I am a Kentucky based USDA Mortgage Lender that has originated over 300 KY Rural Housing Mortgage Loans in Kentucky-CALL OR TEXT 502-905-3708 FOR USDA MORTGAGE LOAN

If you have a credit score below 640 you will probably get referred for a manual underwrite which means the income and credit requirements are much tougher for scores below 640. We can do scores down to 620 but usually it is best to try and raise your score to 640 so we can get an automated approval thru GUS.

If GUS returns an refer/eligible, then we can consider doing a manul underwrite on your loan approval. This usually entails a verifiable rent history over the last 12 months with no lates, and the debt to income ratios are usually tied to the industry old standard of 29% and 41% respectively.

If GUS returns an ineligible status, then your loan is automatically denied and there is no chance of getting approved when this result shows.

Collections:

If you have any delinquent back taxes, student loans they would need to be paid or brought current so you don’t have any liens to the government.

Delinquent Government Debt (back taxes, student loans

Medical bills are usually okay if they are not showing as a garnishment against you or on the title search.

Large unpaid utility bills, credit card charge offs, and car repos will usually have to be paid before closing. You will have to show you have funds to pay these off before closing.

Foreclosure:

You have to be 3 years removed from a foreclosure to qualify for a Kentucky RHS loan.

Bankruptcy:

Chapter 7 Bankruptices require a 3 year wait after the bankruptcy was discharged.

Chapter 13 bankruptices only require 1 year wait after discharge.

Get Expert Help With Your Kentucky USDA Rural Housing Loan that is a foreclosure or fixer-upper with fixed income

Are you considering a USDA rural housing loan in Kentucky to purchase a foreclosed property or fixer-upper home? This comprehensive guide walks Kentucky homebuyers through everything you need to know about USDA 502 Direct and Guaranteed loans. It is especially useful if you are living on fixed income. It’s also helpful for those on Social Security benefits, disability payments, or lower wages.

Can Kentucky Residents Use USDA Rural Housing Loans for Foreclosures or Fixer-Uppers?

Yes, with important conditions. While USDA loans offer an excellent path to affordable homeownership in rural Kentucky communities, these properties must meet specific standards:

The home must be structurally sound

The property must be move-in ready (safe and sanitary)

All essential systems must be functional

The property must be located in a USDA-eligible rural area in Kentucky

Many Kentucky foreclosures can qualify for USDA financing if they’re in good condition or if repairs are completed before closing.

Kentucky USDA Loan Programs: Which Works Best for Your Situation?

Kentucky homebuyers have two primary USDA rural housing loan options:

USDA 502 Direct Loan Program (Kentucky Low-Income Buyers)

Income Requirements: 50-80% of Kentucky area median income

Funding Source: Direct from USDA (government-funded)

Perfect For: Very low to low-income Kentucky residents

Credit Flexibility: Higher flexibility with manual underwriting

Down Payment: $0 down payment required

Mortgage Insurance: Lower annual fee (0.35%)

DTI Ratios: May permit higher DTI with strong residual income

Asset Restrictions: Stricter requirements (cannot have excessive assets)

Best For: Kentucky families with lower, stable incomes including fixed income and disability benefits

USDA 502 Guaranteed Loan Program (Kentucky Moderate-Income Buyers)

Income Requirements: Up to 115% of Kentucky area median income

Funding Source: Private Kentucky lenders with USDA guarantee

Get Pre-Qualified: Work with a Kentucky lender experienced in USDA rural housing loans

Property Inspection: Have any potential foreclosure or fixer-upper thoroughly inspected early

Select Appropriate Program: Determine whether Direct or Guaranteed better suits your circumstances

Prepare Documentation: Gather income verification, tax returns, benefit award letters, and other required paperwork

Frequently Asked Questions About Kentucky USDA Rural Housing Loans

Can I use a Kentucky USDA loan to purchase a foreclosed property?

Yes, if the foreclosed home meets all USDA livability and safety standards.

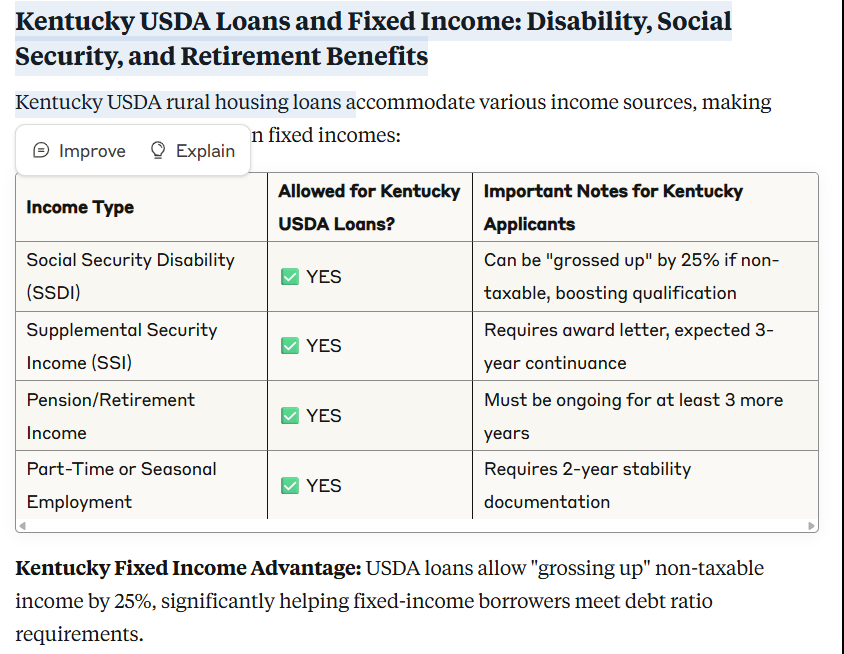

Do Kentucky USDA loans accept disability income for qualification?

Absolutely. Both SSI and SSDI are eligible income sources and can often be “grossed up” by 25% if non-taxable.

What if my desired Kentucky property needs repairs?

USDA Guaranteed loans may allow an escrow holdback for minor repairs (typically up to $10,000). Major issues will disqualify the property.

How do Kentucky’s 502 Direct loans differ from Guaranteed loans?

Direct loans are specifically for very low-income borrowers with tighter restrictions; Guaranteed loans accommodate moderate-income buyers and utilize private lenders. View Kentucky income limits here.

Are manufactured homes eligible for Kentucky USDA loans?

Yes, provided they meet HUD standards and are permanently attached to a foundation.

Can I combine Kentucky Housing Corporation down payment assistance with USDA?

Yes, KHC programs can often be paired with USDA loans for additional assistance.

Get Expert Help With Your Kentucky USDA Rural Housing Loan

Need assistance navigating Kentucky’s USDA rural housing loan options? Our experienced mortgage professionals specialize in helping Kentucky homebuyers with fixed income, disability benefits, and unique financing needs.

Annual Qualifying Income – The requirement for calculations to be included on the Income Calculation worksheet have been removed and should now be included on Attachment 9-B, the underwriter transmittal summary, FNMA form 1008/Freddie form 1077, or equivalent

4506-T – The requirement for asset statements to be reviewed to ensure borrowers have no additional income sources has been removed.

Repayment Income – MCC income must now be included in repayment income.

Boarder Income – USDA now considers a boarder as a household member and a boarder’s income must now be included in annual income calculation. Rent paid by boarders that is reported on tax returns must also be included in annual income.

Capital Gains – USDA removed requirement from Repayment Income to provide evidence showing borrowers own additional property or assets that may be sold if additional income is needed to support the mortgage obligation

Commission – The borrower must now show one year history in same or similar line of work to include commission in repayment income.

Fellowship, Stipend, Scholarship – Scholarship award letters must now provide date of termination and USDA will no longer presume benefits with no expiration date will continue. USDA also added guidelines for GI Bill income and stated it cannot be included in annual or repayment income.

MCC – This income must now be included in repayment income, but no history is required. A copy of the W-4 from employer is required to verify borrower is taking tax credit on monthly basis. Note: MCC’s are ineligible with FWL as qualifying income.

Unreimbursed Business Income – only taxable income is allowed to be included in repayment income

Section 8 – USDA removed requirement for section 8 income to be deducted from the monthly PITI to determine DTI if it is paid directly to the loan servicer when included in the repayment income.

Self Employed Income – Federal tax returns must now be reviewed to determine gross income for annual calculations. Removed requirement to deduct business loss before entering as repayment income into GUS or on loan application. Clarified documentation requirements as most recent 2 years of federal tax returns / transcripts & YTD P&L may be audited or unaudited

Social Security Income – clarified documentation options and will allow social security benefit statement or form SSA-1099/1042S to source

Temporary Leave – The history requirements for repayment income has been changed and now income must be received by loan closing.

Cash on Hand – The underwriter must review the reasonableness of accumulation based upon income stream, spending habits, etc. and cash on hand can no longer be included in reserves

Gift Funds – Clarification provided on how gift funds must be sourced when gift funds have been deposited into borrower’s account, not deposited into borrower’s account, or if funds are being wired directly to the settlement agent.

Large Deposits – USDA no longer addresses lump sum additions.

KENTUCKY RURAL HOUSING CHANGES TO ANNUAL USDA GUARANTEE FEE STRUCTURE

ANNUAL GUARANTEE FEE

THROUGH 9/30/2014

EFFECTIVE 10/1/14

Purchase Transactions

.40%

.50%

Refinance Transactions

.40%

.50%

The new fee structure is applicable to all Conditional Commitments issued by Kentucky Rural Development Loans on or after October 1, 2014.

Loan guarantee requests submitted to Rural Development (RD) on which a conditional commitment has not been issued by September 30, 2014, will be subject to the 2014 annual guarantee fee structure.

There is no exception to the new annual guarantee fee structure regardless of the date the file was submitted/received by RD . Inc. If the Conditional Commitment has not been issued before October 1, 2014, the file will need to be revised to reflect the correct fees and this will require re-disclosure, re-underwriting and resubmission to RD.

The Guarantee Fee change will take effect 10/1/2014.

Income from all occupants of the household must be included as qualifying income regardless of whether or not they are obligated on the note. Income eligibility can be determined from the following USDA web site. Final eligibility must still be determined by USDA

When a borrower has a rental property it must also be included in the eligibility calculation.

Positive net rental income is included in the eligibility income for the household

Negative net rental income is counted as zero for eligibility income

Qualifying Income:

The underwriter is responsible for calculating income and approving the loan. Applicants with commission only position’s, or varying amounts of overtime and bonus income may not exhibit enough stable monthly income to qualify. Typically, income of less than 24 months duration should not be included in qualifying income.

Salaried Borrowers

Pay-stubs covering most recent 30 day period, W-2’s for the previous two years and telephone verification of employment performed by Freedom Mortgage (paystub must show at least 30 days of year-to-date earnings).

If overtime, commission, or bonus income is used for qualifying purposes the file must be documented with a two year history of receipt and be expected to continue.

Standard VOE, sent directly to the employer, along with the borrower’s most recent paystub.

Self-Employed Borrowers

Copies of the borrower’s signed individual Federal tax returns that were filed with the IRS for the most recent two years. As an alternative, the Freedom may obtain IRS-issued transcripts of the borrower’s tax returns, as long as the transcripts include the information from all of the applicable schedules. The tax return documentation should be complete and include all appropriate schedules.

The self-employed applicant also should submit current documentation of the business’s income and expenses, including any applicable Federal tax returns that were filed with the IRS for the most recent two years as well as year-to-date profit and loss and balance statements.

Rental Income

Rental income may only be counted for repayment income if the lease has been in place for at least two years. For leases older than two years, count positive net rental income in repayment income and negative net rental income as debt. If rental income is not received for a full two year period then the full PITIA must be used in the debt to income calculation.

Rental income calculation – reduce monthly gross income by a 25% vacancy rate, and then the monthly PITI, HOA dues, etc. are subtracted. If positive then include in income if negative include in DTI.

All other income sources refer to USDA guidelines for all income guidelines and documentation requirements

Assets:

Assets are not required; however, any assets disclosed must be supported with appropriate documentation

Satisfactory explanation and documentation should be provided for large deposits or increases in liquid assets

Cash on hand is not acceptable

Bank accounts require Verification of Deposit with average 2 month balance, or 2 consecutive months statements dated within 45 days of loan application

Earnest money deposit may be considered an asset if deposit is not already reflected in liquid assets

Asset amount of retirement accounts is 60% of the vested account balance

Gifts must be documented through gift donor letter and establish that gift does not have to be repaid

For sale proceeds of real property, provide HUD-1 or equivalent closing statement to indicate the actual amount of cash proceeds realized by the borrower

Stocks and bonds must be documented by a statement provide by stockbroker or financial institution managing the portfolio

Households with net family assets of greater than $5,000 require that the actual income derived from all net family assets or a percentage of the value of such assets based on the current passbook savings rate be considered when calculating income.