On March 15th, 2024, the National Association of Realtors (NAR) agreed to pay $418 million in damages to settle some of their real estate commission lawsuits. The settlement prohibits NAR from requiring a seller’s agent to engage in cooperative compensation with a buyer’s agent.

The key details are:

Date: March 15th, 2024

Payment: NAR agreed to pay $418 million in damages

Settlement terms: NAR prohibited from requiring seller’s agent to cooperate with buyer’s agent on commissions

This settlement is significant because the new terms will likely have ripple effects that both consumers and industry stakeholders will experience:

Consumers:

Potentially lower real estate commission fees as a result of increased competition between agents

More flexibility and control for sellers in how they compensate buyer’s agents

Possibility of buyers having to pay their agent’s fees directly rather than them being bundled into the home price

Industry Stakeholders:

Real estate brokerages and agents may need to adjust their business models and commission structures

Reduced influence of NAR in setting industry standards and practices around commissions

Potential for new business models and pricing approaches to emerge in the real estate market

Overall, this settlement represents a shift in the power dynamics of the real estate industry that could lead to more competition and consumer-friendly changes in the way real estate transactions are conducted. Let me know if you have any other questions!

Real Estate Commissions and Loan Types in Kentucky

The National Association of Realtors (NAR) recently reached a settlement that impacted real estate commissions for different mortgage loan types in Kentucky and across the United States. Here’s a breakdown of how commissions can vary:

Conventional Loans

For conventional mortgage loans, the typical real estate commission is 3-6% of the home’s sale price.

This commission is usually split evenly between the buyer’s agent and the seller’s agent.

Buyer may pay their Agent’s reasonable commissions or have the seller or agent contribute to the commission of the buyer agents’ commission. Typical fees paid by the seller are not subject to the IPC limits. (interested party contribution)

FHA Loans

For FHA (Federal Housing Administration) loans, the real estate commission is typically slightly lower, around 3-6% of the sale price.

This lower commission is due to the additional requirements and paperwork involved with FHA loans.

FHA Loans-FHA allows buyer to pay commissions of their agents, or negotiate the seller’s or agent contribution to commission to the buyer’s agent. – If the State and Local law or custom permits this, and if the commissions and fees are reasonable in amount, the existing policy would not treat it as an IPC. (interested party contribution)

VA Loans

For VA (Veterans Affairs) loans, the real estate commission is usually the lowest, around 3-6% of the sale price.

VA loans have strict guidelines, and the lower commission helps offset some of the additional costs associated with these loans.

VA Loans-Buyer may pay their agent’s commission or negotiate the seller or agents contribution to commission to the buyer’s agent. (interested party contribution) IPC is not mentioned. A temporary variance is permitted for the Veteran buyer to pay Buyer Broker Fees.

USDA Loans

USDA (United States Department of Agriculture) loans, which are designed for low-income homebuyers in rural areas, also typically have a real estate commission of 3-6%.

The lower commission helps make these loans more affordable for the homebuyers.

USDA loans-Buyer may pay their agents commission or negotiate the seller’s or agent’s contribute to the commission of the buyer’s agent. Real Estate Commission Fees are excluded from the 6% cap for IPC concessions

—

s.

Reach out to me anytime on my cell — Always happy to help!

Joel Lobb Mortgage Loan Officer NMLS 57916

EVO Mortgage

911 Barret Ave, Louisville, KY 40204

Company NMLS ID # 173846

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

NMLS ID# 57916, (www.nmlsconsumeraccess.org).

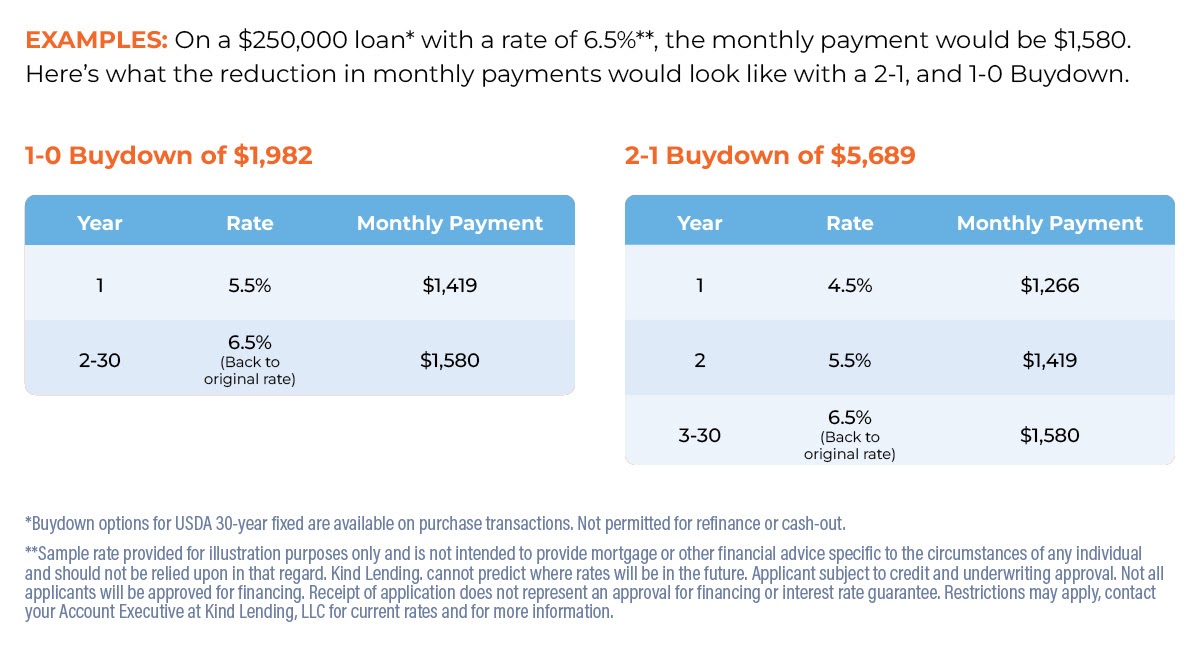

2-1 and 1-0 buydowns for Kentucky Rural Housing USDA RD loans Interest Rates.

What are Buydowns for Kentucky USDA RD Loans?

The Kentucky Rural Housing USDA Buydown Program provides simple financing options that lowers the interest rate on a mortgage for either 1 year (1-0) or 2 years (2-1), before it rises to the regular permanent rate. Specifics2-1, and 1-0 temporary interest rate buydowns are allowed on 30 year fixed-rate mortgages for principal residences, purchase only. Not permitted on refinance transactions.The seller or agent may provide funds for the temporary interest rate buydown, subject to standard interested party contribution limits.Lender paid buydowns are not offered.The borrower is qualified at the note rate fully amortized (not the buydown rate)Minimum credit score for loans with buydown is 620

Have Questions or Need Expert Advice? Text, email, or call me below:

Joel Lobb Mortgage Loan Officer Individual NMLS ID #57916

American Mortgage Solutions, Inc. 10602 Timberwood Circle Louisville, KY 40223 Company NMLS ID #1364

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org).

Kentucky USDA loans are mortgages made by lenders and guaranteed by the U.S. Department of Agriculture. They are available to moderate- and low-income borrowers to build, rehabilitate, improve or relocate a primary residence in eligible rural and suburban areas. The income limit is 115 percent of the median income in your area. You can check the income limits for your area here.

It can be closed with zero down. USDA loans do have a monthly insurance requirement, but the upfront fee is significantly lower than on the VA loan and the mortgage premiums are lower than on the FHA loan.

The problem is that the number of buyers who qualify for a USDA loan is much smaller. Unlike on other loans where more income is better, a USDA loan has strict income maximums.

Credit Score Required for Kentucky Rural Housing Loans

There is no minimum credit score for a USDA loan, but you are automatically ineligible if you are presently delinquent on a nontax federal debt.

Automated approval is available if you have two tradelines reported on your credit history and acredit score of 640 or higher.

If you do not have sufficient credit data, the underwriter can assess your creditworthiness other ways, such as by examining your history with rent payments. Applicants with a credit score lower than 640 will undergo additional underwriting steps.

Why Would a Seller Agree to a Seller Credit?

Seller Benefits:

~ Seller credits help a home sell faster in buyer markets.

Price Reductions are costlier to a seller than credits.

~ Innovative “Good Will” to support a new homeowner adjusting to homeownership.

When the housing market turns into a buyer’s market, selling a home can be quite competitive.

The seller is no longer expecting to receive 100% or more of their asking price and instead expects to take less than their asking price to sell their property.

Therefore, they may offer a credit to attract more people to buy their home. After all, the seller is only concerned about selling their home at a reasonable price and selling it as quickly as possible. Seller credits and concessions are a very popular tactic to give the perception that buying their home is better. Seller credits work because many first-time buyers struggle to come up with the down payment and closing costs, and seller credits ease that burden.

Buyer Benefits:

~ Allows the buyer to ease into homeownership by paying below fixed-rate payments.

~ Does not increase the loan amount. The loan amount amortizes as a standard fixed-rate loan.

~ Safe way to take advantage of a lower payment in a rising rate environment.

A Seller Credit Can:

= Offset closing costs

= Permanentlv Reduce an interest rate

= Temporarily Reduce an interest rate

In all three scenarios, this helps your buyers. Each buyer has different needs, so it is up to you to help them In all three scenarios, this helps your buyers.

Each buyer has different needs, so it is up to you to help them figure out how to best apply a seller credit.

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

If you are looking to buy a home in Northern Kentucky, to either own a home on acreage in the country with 100% financing on your home loan with zero down, then you need to look at the Kentucky USDA Rural Housing Loan Program.

How Does the USDA Home Loan Work in Northern Kentucky?

Here are some of the Key Financial Elements of the USDA Home Loan in Northern Kentucky:

Low to Middle-Income Households are generally eligible – If the Household Income is too high, you may be ineligible.

30 Year Fixed Term Loans at Today’s Low Interest Rates compared to FHA, USDA and other government mortgage loans

Qualifying rations are 29% for Housing and 41% for total debt. or possibly higher with a credit score over 640.

Rural Development Loan Guarantee Fee applies, currently 1% USDA funding fee and .35% monthly mi premium

Zero Cash required for the Down Payment. If access to 20% down payment, then you cannot use this program.

Flexible Credit Guidelines, where non-traditional histories may be accepted. USDA will do a no score loan, but it is very difficult to qualify for so your best bet is to get your credit scores to 620 to 640 range and go from there. You will need two trade lines on the credit report for last 12 months, so no limited credit history is allowed on this program.

Eligible properties include: Existing Homes, New Construction, New Manufactured Homes, Modular Homes, and eligible Condos!—No used mobile homes.

Eligible Repairs may be included in the loan as well! If home appraises for more than sales price, sometimes you can finance these repairs into the loan.

They’re are two income tests. Compliance income and repayment income. See pic below for answers about Northern Kentucky Counties with max income limits for household

Home must be in an eligible area. See map below of Northern Kentucky Eligibility for USDA Rural Housing Loans

What Parts of Northern Kentucky Are Eligible for the USDA Home Loan?

With Northern Kentucky being part of the metro area of Cincinnati, the USDA has provided a map of the Ineligible Northern part of the Counties of Boone, Kenton, Campbell counties which means, the remaining southern part of the counties of Boone, Kenton, Campbell being eligible. Here is the Northern Kentucky rural housing map courtesy of the USDA:

What Parts of Northern Kentucky Are Eligible for the USDA Home Loan?

What are the income limits for a Rural Housing Loan in Northern Kentucky?

Households with 1-4 members have different limits as households with 5-8. Similarly, applicants living in high-cost counties will have a higher income limit than those living in counties with a more average cost of living.

Here are a few more items to check off before looking into this loan or at a particular property:

Must be Owner Occupied as the Primary Residence;

Home must not be used to produce Income, nor can there be Income Producing Buildings or other Accessories that produce Income on the property; i.e. no working farms or cows, livestock, crops etc. Can be a small hobby farm.

No foreclosed homes that that need a lot of work.

Home must be structurally sound and in reasonably good repair and pass FHA standards on an appraisal.

Home cannot be used for a Rental Property or, be a major fixer

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223

Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Here are a few reminders about the Kentucky USDA Rural Housing Service (RHS) Section 502 Guaranteed program which provides very-low-, low- and moderate-income rural residents access to affordable housing finance options with little or no down payment or out-of-pocket costs.

• Eligibility Link – Access the USDA Home page, click here.

• Income – To determine eligibility of an applicant/household, click here.

• Property Eligibility – To determine whether the property is located in a designated rural area, click here.s

30 year fixed rate loan terms only, Purchase or refinance, If refinancing must be existing USDA home loan. No cash out allowed.

• Occupancy – Owner occupied only.

• Maximum Loan Amount-No max loan amount

• Max DTI – GUS approved, generally 45% (front end sensitive)/ Manual 29/41.

• Guaranty Fee/Annual Fee – there is a 1.00%/ 0.35% (monthly).

• Down Payment – Down payment not required but if any cash to close, must be borrowers own funds. Gifts are not allowed.

• Interested Third Party Contributions – An amount of 6% of the sales price can be contributed towards closing costs.

.

If you meet income eligibility requirements and are looking to settle in a rural area, you might qualify for the KY USDA Rural Housing program. The program guarantees qualifying loans, reducing lenders’ risk and encouraging them to offer buyers 100% loans. That means Kentucky home buyers don’t have to put any money down, and even the “upfront fee” (a closing cost for this type of loan) can be rolled into the financing.

Fico scores usually wanted for this program center around 620 range, with most lenders wanting a 640 score so they can obtain an automated approval through GUS. GUS stands for the Guaranteed Underwriting system, and it will dictate your max loan pre-approval based on your income, credit scores, debt to income ratio and assets.

CREDIT SCORES UNDERWRITING USDA MORTGAGE FOR RURAL HOUSING

This attachment illustrates the approach to reviewing credit history when a loan is

manually underwritten by an approved lender. Credit score over 680: Perform a basic level of underwriting to confirm the

applicant has an acceptable credit reputation. Perform additional analysis if the

applicant’s credit history has indicators of unacceptable credit as noted in Paragraph 10.7 of this Chapter. Credit score 679 to 640: Perform a comprehensive level of underwriting.

Underwrite all aspects of the applicant’s credit history to establish the applicant has an

acceptable credit reputation. Credit scores in this range indicate the applicant’s

reputation is uncertain and will require a thorough analysis by the underwriter of the

credit to draw a logical conclusion about the applicant’s commitment to making

payments on the new mortgage obligation. The applicant’s credit history should

demonstrate his or her past willingness and ability to meet credit obligations. Credit score less than 640: Perform a cautious level of underwriting. Perform a

detailed review of all aspects of the applicant’s credit history to establish the applicant’s

willingness to repay and ability to manage obligations as agreed. Unless there are

extenuating circumstances documented in accordance with this Chapter, a credit score in this range is generally viewed as a strong indication that the applicant does not have an acceptable credit reputation. Little or no credit history: The lack of credit history on the credit report may be

mitigated if the applicant can document a willingness to pay recurring debts through

other acceptable means such as third party verifications or cancelled checks. Due to

impartiality issues, third party verifications from relatives of household members are not

permissible. Lenders can develop a Non-Traditional Credit Report for applicants who

do not have a credit score in accordance with Paragraph 10.6 of this Chapter.

An applicant with an outstanding judgment obtained by the United States in a

Federal court, other than the United States Tax Court, is not eligible for a guarantee

unless otherwise stated in this Chapter.They also allow for a manual underwrite, which states that the max house payment ratios are set at 29% and 41% respectively of your income.

See link here for more detailed guidelines for credit score, disputed accounts, foreclosures, trade line requirements bankruptcies below:

Indicators of unacceptable credit. The following indicators require documentation

meeting the criteria of Section 10.8 to approve an applicant’s loan request for manually

underwritten loans: Foreclosure and Bankruptcy Guidelines

Foreclosure within 3 years:

Including pre-foreclosure activity, such as a pre-foreclosure sale or short sale

in the previous 3 years (refer to Attachment 10-B for additional guidance);

Bankruptcy within 3 years:

Chapter 7 bankruptcy discharged in the previous 3 years;

An elapsed period of less than 3 years, but not less than 12 months, may

be acceptable if the applicant meets the criteria of Section 10.8 of this

Chapter.

Chapter 13 bankruptcy that has yet to complete repayment (repayment plan in

progress) or has completed payment in the most recent 12 months.

Plans that are completed for 12 months or greater do not require a credit

exception in accordance with Section 10.8;

Late mortgage payments if any mortgage trade line during the most recent 12

months shows 1 or more late payments of greater than 30 days

Collections Accounts

.

In an effort to minimize future risk of open collections left unpaid, the lender will

consider the following during the capacity analysis of the loan request, regardless of the

method utilized to underwrite:

1) Determine if the total outstanding balance of all collections accounts of all

applicants is equal to or greater than $2,000. Unless excluded by state law,

collection accounts of a non-purchasing spouse in a community property state are

included in the cumulative balance of all collections.

2) Remove all medical collections and all types of charge off accounts from the total

balance. Medical collections and charge off accounts must be clearly identifiable

on the credit report.

3) If the remaining outstanding balance of collection accounts are equal to or greater

than $2,000, any of the following actions will apply:

a. Payment in full of all collection accounts at or prior to closing.

b. Payment arrangements are made with each creditor for each collection

account remaining outstanding. A letter from the creditor or evidence on

the credit report is required to validate the payment arrangements. The

agreed upon monthly payment for each outstanding collection account

will be included in the borrower’s debt-to-income ratio.

c. In the absence of a payment arrangement, the lender will utilize in the

debt-to-income ratio a calculated monthly payment. For each collection

utilize 5% of the outstanding balance to represent the monthly payment.

They loan requires no down payment, and the current mortgage insurance is 1% upfront, called a funding fee, and .35% annually for the monthly mi payment. Since they recently reduced their mi requirements, USDA is one of the best options out there for home buyers looking to buy in a rural area.

A rural area typically will be any area outside the major cities of Louisville, Lexington, Paducah, Bowling Green, Richmond, Frankfort, and parts of Northern Kentucky.

There is also a max household income limits with most cutoff starting at $87,000 for a family of four, and up to $115,000 for a family of five or more.

Kentucky FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.