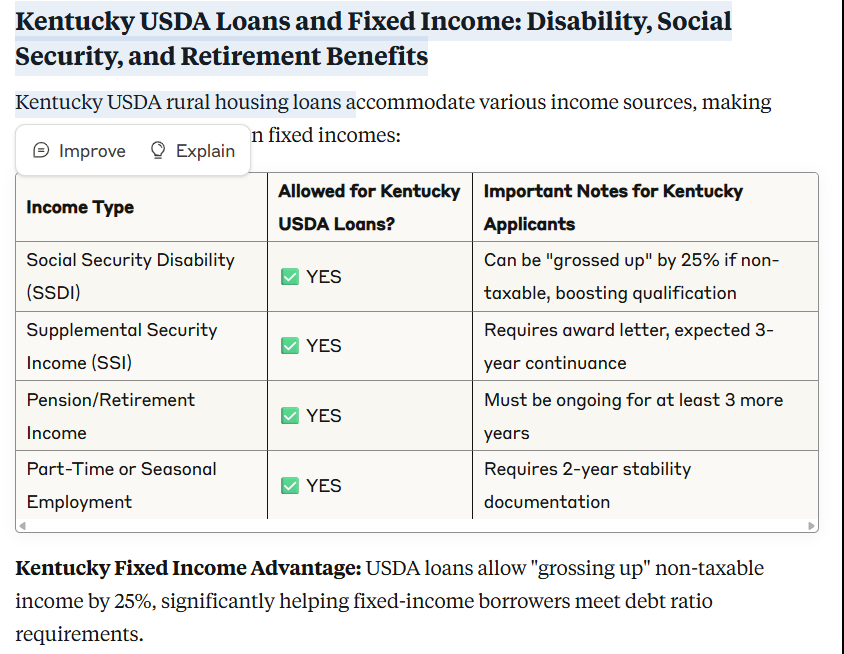

<

Kentucky USDA Loans: 502 Direct vs. Guaranteed — Which One Is Right for You?

If you’re looking to buy a home in rural Kentucky with no down payment, a USDA Rural Housing loan could be your best option. But there are two very different programs under the USDA umbrella — and choosing the wrong one could slow down your home purchase or leave money on the table.

In this guide, I’ll break down the USDA 502 Direct loan and the USDA Guaranteed loan side by side so you know exactly which program fits your situation — and how to get started today.

What Are USDA Rural Housing Loans?

USDA Rural Housing loans are backed by the U.S. Department of Agriculture and are designed to help low- to moderate-income buyers purchase homes in eligible rural areas of Kentucky. Both programs offer 100% financing — meaning no down payment is required — and both are available to first-time and repeat homebuyers alike.

The key difference is who lends you the money and how much you can earn and still qualify.

USDA 502 Direct Loan vs. Guaranteed Loan: Side-by-Side Comparison

| Feature | 502 Direct Loan | Guaranteed Loan |

|---|---|---|

| Who funds the loan | USDA directly | Private lender (e.g., mortgage company) |

| Income limit | Very low / low income | Moderate income (up to 115% AMI) |

| Interest rate | Subsidized — as low as 1% effective rate | Current market rate |

| Loan term | 33 years (38 years for very low income) | 30-year fixed |

| Down payment | None required | None required |

| Minimum credit score | 640+ | 640+ (typically) |

| Where to apply | Local USDA Rural Development office | Approved mortgage lender |

| Approval speed | Slower — depends on USDA funding | Faster — same-day pre-approval available |

| Payment subsidy | Yes — income-based assistance | No |

| Subsidy recapture at payoff | Yes — may apply | No |

| Annual fee | None | 0.35% of loan balance/year |

The USDA 502 Direct Loan — A Closer Look

The Section 502 Direct Loan is funded by the USDA itself. You apply directly through one of approximately 13 USDA Rural Development offices in Kentucky, not through a private lender.

Who qualifies?

This program is specifically for very low- and low-income buyers who cannot qualify for financing elsewhere on reasonable terms. To be eligible, you must:

- Currently be without decent, safe, and sanitary housing

- Be unable to obtain a conventional loan on terms you can reasonably meet

- Agree to occupy the property as your primary residence

- Meet USDA citizenship or eligible noncitizen requirements

- Have a credit score of 640 or higher with at least 2 active or closed trade lines over 12 months

What’s the interest rate?

The Direct loan carries a fixed rate based on current market rates at approval or closing — whichever is lower. USDA then provides payment assistance (subsidy) based on your adjusted family income, which can reduce your effective interest rate to as low as 1%. This is one of the most affordable mortgage programs available anywhere.

Important note: When the property is sold or you no longer occupy it, you may be required to repay some or all of the subsidy you received. This is called subsidy recapture.

Property requirements for the Direct loan

- Must be modest in size for the area

- Cannot have a market value exceeding the applicable area loan limit

- Cannot have an in-ground swimming pool

- Cannot be designed for income-producing activities

- For manufactured housing: only new construction is eligible

Homebuyer education required

All Direct loan borrowers must complete a homebuyer education course prior to closing.

The USDA Guaranteed Loan — A Closer Look

The USDA Guaranteed loan (also called the Section 502 Guaranteed loan) is the program most Kentucky homebuyers use. You apply through an approved private lender — like me — and USDA guarantees the loan against default. This protects the lender and allows them to offer favorable terms with no down payment.

Who qualifies?

This program serves moderate-income buyers — generally households earning up to 115% of the area median income (AMI). For most Kentucky counties in 2024, that’s roughly $103,000–$110,000 for a household of four. Exact limits vary by county and household size.

You must also:

- Purchase a home in a USDA-eligible rural area (most Kentucky areas outside Louisville, Lexington, and Bowling Green qualify)

- Occupy the home as your primary residence

- Have a qualifying credit profile (640+ score typically)

- Meet debt-to-income guidelines

Fees for the Guaranteed loan

Unlike the Direct loan, the Guaranteed program includes two fees:

- 1% upfront guarantee fee — typically financed into the loan at closing

- 0.35% annual fee — paid monthly as part of your mortgage payment

These fees are significantly lower than FHA mortgage insurance premiums, making USDA one of the most cost-effective zero-down loan options available.

Can I combine this with Kentucky down payment assistance?

Yes. The USDA Guaranteed loan can be paired with KHC (Kentucky Housing Corporation) down payment assistance programs. Since USDA already covers 100% of the purchase price, KHC funds can be applied toward closing costs — reducing your out-of-pocket expenses at the closing table to near zero.

Which USDA Loan Is Right for You?

Here’s a simple rule of thumb:

- Very low or low income? The 502 Direct loan offers the deepest subsidy and the lowest effective payment — but you’ll apply through USDA directly and the process takes longer.

- Moderate income? The Guaranteed loan is faster, processed through a private lender, and can be combined with KHC assistance. It’s the most common USDA loan in Kentucky for a reason.

- Not sure which applies to you? Call or text me at 502-905-3708. I’ll pull your county’s income limits, check the property address, and tell you exactly which program you qualify for — usually in the same conversation.

Frequently Asked Questions — USDA Loans in Kentucky

Do I have to be a first-time homebuyer to use a USDA loan?

No. Both USDA programs are open to repeat buyers. The requirement is that you cannot own another adequate, decent home at the time of closing, and the new property must be your primary residence.

How do I check if a Kentucky property is in a USDA-eligible area?

You can check any address at the USDA’s eligibility website at eligibility.sc.egov.usda.gov. Generally, rural areas with populations under 35,000 qualify. Or simply text me the address and I’ll check it immediately.

What credit score do I need for a USDA loan in Kentucky?

Both programs typically require a minimum 640 credit score. Lenders will also look at the number and age of your trade lines. If your score is below 640, I can walk you through steps to improve it before applying. Learn more on my FHA loan page for alternative options.

How long does it take to close on a USDA loan in Kentucky?

The Guaranteed loan typically closes in 30–45 days once you’re under contract — similar to FHA. The Direct loan can take considerably longer, as processing times depend on USDA’s funding availability and regional demand.

Is there a USDA guarantee fee like FHA mortgage insurance?

Yes, but it’s lower. The Guaranteed loan has a 1% upfront fee (financeable) and a 0.35% annual fee. Compare that to FHA’s 1.75% upfront and 0.55%+ annual MIP. For many Kentucky buyers, USDA is the better deal when the property and income qualify.

Can I combine a USDA Guaranteed loan with KHC down payment assistance?

Yes — and it’s one of the most powerful combinations available to Kentucky first-time buyers. KHC assistance covers closing costs, making it possible to buy a home with little to no cash out of pocket. See my full guide on Kentucky Housing Corporation programs.

Ready to See If You Qualify for a USDA Loan in Kentucky?

I’ve helped 1,300+ Kentucky families close on homes using USDA, FHA, VA, and KHC programs. With over 20 years of experience in Kentucky mortgage lending, I know these programs inside and out — and I’ll match you to the right one, fast.

- ✅ Free mortgage application

- ✅ Same-day pre-approval

- ✅ Expert guidance on USDA, FHA, VA & KHC programs

- ✅ Down payment assistance still available for qualifying buyers

📞 Call or text: 502-905-3708

📧 Email: kentuckyloan@gmail.com

🌐 Apply online: www.kentuckymortgageblog.com

Joel Lobb | Mortgage Loan Officer | NMLS #57916 | Company NMLS #1738461 |

www.nmlsconsumeraccess.org

Equal Housing Lender. All loans subject to credit approval and program guidelines. Income and property eligibility requirements apply.

USDA loan programs are subject to change. This website is not endorsed by or affiliated with the USDA, FHA, VA, or any government agency.

Information is provided for educational purposes only and does not constitute a commitment to lend.

Loan terms and availability vary by location and borrower qualification.

Website:

Website:  Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204