How to Get a Free Credit Score for Mortgage Loan Approval

Before applying for a Kentucky mortgage loan, make sure you understand the difference between a free consumer credit score and the mortgage credit scores lenders actually use.

Key Takeaway

The credit score you see on Credit Karma, a credit card app, or a consumer credit monitoring site may not be the same score used for a mortgage approval. Most mortgage lenders review mortgage-specific credit scores when determining eligibility for FHA, VA, USDA, KHC, and conventional home loans.

3 Ways to Check Your Credit Before Applying for a Mortgage

1. Pull Your Free Credit Reports

Start by reviewing your free credit reports at AnnualCreditReport.com. Look for late payments, collections, incorrect balances, duplicate accounts, old addresses, and accounts that do not belong to you.

Remember: your free credit report usually does not include your actual mortgage credit score.

2. Use myFICO for Mortgage FICO Scores

myFICO offers access to multiple FICO score versions, including mortgage-related score models. This is usually not free, but it can help consumers see scores closer to what a mortgage lender may review.

3. Contact a Mortgage Lender or Broker

A mortgage lender or mortgage broker can pull a mortgage credit report as part of the pre-approval process.

At my office, there is no upfront out-of-pocket cost for the credit report. If your loan closes with us, the credit report fee may be collected at closing and shown on your settlement statement.

Important: Not All Credit Scores Are the Same

Free credit score apps may show VantageScore or newer consumer FICO models. Those scores can be helpful for general credit monitoring, but they may not match the mortgage middle score used for loan approval.

Example: you may see a 680 score on a free credit app, but your actual mortgage middle score could be different.

Common Mortgage Credit Score Guidelines

Loan Program

Common Minimum Score Guideline

FHA Loan

580+ for 3.5% down

VA Loan

No official VA minimum, but many lenders require 580–620+

USDA Loan

Often 620–640+ depending on lender and automated approval

Conventional Loan

Often 620+

KHC Down Payment Assistance

Usually tied to the first mortgage program and lender approval

Want to Know Your Real Mortgage Credit Score?

If you are buying a home in Kentucky, I can help review your mortgage credit profile and explain your options for FHA, VA, USDA, KHC, and conventional mortgage programs.

Joel Lobb

Mortgage Loan Officer

NMLS #57916

EVO Mortgage | Company NMLS #1738461

911 Barret Ave., Louisville, KY 40204

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval, income verification, property approval, and program guidelines. Not affiliated with FHA, VA, USDA, KHC, Fannie Mae, Freddie Mac, or any government agency.

Big News for Kentucky Mobile Home Buyers: USDA Loan Changes Coming in

Are you looking for affordable home financing options for manufactured or mobile homes in Kentucky? Big news is here! Starting March 4, 2025, the USDA will officially offer 100% financing for manufactured homes. This exciting change will make homeownership more accessible and affordable for families in Kentucky.

You can now take advantage of FHA loans with Kentucky Housing Corporation’s down payment assistance. This assistance is available on used mobile homes or new mobile homes. This assistance offers a path to 100% financing. This option is ideal for those purchasing manufactured homes in urban and rural areas alike

What Does This Mean for Kentucky Homebuyers?

For years, many buyers in Kentucky seeking affordable housing options, like mobile homes, faced limited financing choices. With the USDA’s policy changes, more Kentucky homebuyers will qualify for 100% financing on manufactured homes. This program is transformative. It is especially beneficial for those in rural areas. Many are looking to take advantage of USDA’s Rural Housing Loan Program.

Benefits of the USDA Manufactured Home Loan Program

100% Financing – No money down is required, making it perfect for buyers with limited savings.

Affordable Terms – Competitive interest rates make monthly payments manageable.

Rural Housing Opportunities – Ideal for Kentucky homebuyers in small towns and rural areas.

Expanded Eligibility – These changes will allow more manufactured homes to qualify, opening up affordable housing options.

How to Qualify for a USDA Loan for Mobile Homes in Kentucky

To take advantage of this incredible opportunity, you’ll need to meet a few requirements:

Credit Score: Typically, a score of 581 or higher is needed.

With rising home prices, these changes make it easier for families in Kentucky to purchase affordable housing. Manufactured homes are an excellent option for those seeking modern, energy-efficient, and affordable living solutions. This program ensures that homeownership is possible for more families across Kentucky, particularly in rural communities.

Get Pre-Approved for Your USDA Mobile Home Loan in Kentucky

Don’t wait until March 2025! Start planning now to take advantage of these USDA loan changes. Are you considering purchasing a mobile home in Kentucky? I can help you secure the best financing option for your needs.

I specialize in USDA and rural housing loans for mobile and manufactured homes across Kentucky. I have decades of experience and local expertise. I’m here to guide you through the process. I will help you achieve your dream of owning a home with no money down.

100% financing · No down payment · Fixed 30-year rate

0%

Down payment required

100%

Financing available

620+

Typical credit score

Key benefits — click to expand

No down payment

Click to learn more ›

Borrowers without savings — or who wish to keep their savings — can qualify. Closing costs may also be financed if the appraised value exceeds the purchase price.

Low mortgage insurance

Click to learn more ›

USDA has the lowest upfront and monthly mortgage insurance of any 100% loan program — keeping your monthly payment as low as possible on a 30-year fixed rate.

Flexible credit guidelines

Click to learn more ›

No minimum credit score is set by USDA, though lenders typically require 620–640. Borrowers with a 640+ score enjoy streamlined processing with no credit explanation letters needed.

Generous income limits

Click to learn more ›

Income limits are based on 115% of the U.S. median. Deductions apply for dependents, child-care expenses, and elderly households — making it easier for Kentucky families to qualify.

Not just first-time buyers

Click to learn more ›

Any qualified buyer may use a USDA loan — not only first-time homebuyers. Sellers are also permitted to pay the buyer’s closing costs, further reducing out-of-pocket expenses.

Rural areas across Kentucky

Click to learn more ›

Eligible areas include open country and towns with a population of 10,000 or less. Many Kentucky communities outside major metros qualify — check eligibility at the USDA website.

Debt-to-income ratio guidelines

Housing (PITI)

≤ 29%

Total debt

≤ 41%

Buyers with satisfactory credit may qualify with higher ratios in high-cost areas.

Joel Lobb · Mortgage Loan Officer · NMLS #57916 · Company NMLS #1738461

Equal Housing Lender · Kentucky mortgage loans only

This page is not endorsed by USDA, FHA, VA, or any government agency.

Get Expert Help With Your Kentucky USDA Rural Housing Loan that is a foreclosure or fixer-upper with fixed income

Are you considering a USDA rural housing loan in Kentucky to purchase a foreclosed property or fixer-upper home? This comprehensive guide walks Kentucky homebuyers through everything you need to know about USDA 502 Direct and Guaranteed loans. It is especially useful if you are living on fixed income. It’s also helpful for those on Social Security benefits, disability payments, or lower wages.

Can Kentucky Residents Use USDA Rural Housing Loans for Foreclosures or Fixer-Uppers?

Yes, with important conditions. While USDA loans offer an excellent path to affordable homeownership in rural Kentucky communities, these properties must meet specific standards:

The home must be structurally sound

The property must be move-in ready (safe and sanitary)

All essential systems must be functional

The property must be located in a USDA-eligible rural area in Kentucky

Many Kentucky foreclosures can qualify for USDA financing if they’re in good condition or if repairs are completed before closing.

Kentucky USDA Loan Programs: Which Works Best for Your Situation?

Kentucky homebuyers have two primary USDA rural housing loan options:

USDA 502 Direct Loan Program (Kentucky Low-Income Buyers)

Income Requirements: 50-80% of Kentucky area median income

Funding Source: Direct from USDA (government-funded)

Perfect For: Very low to low-income Kentucky residents

Credit Flexibility: Higher flexibility with manual underwriting

Down Payment: $0 down payment required

Mortgage Insurance: Lower annual fee (0.35%)

DTI Ratios: May permit higher DTI with strong residual income

Asset Restrictions: Stricter requirements (cannot have excessive assets)

Best For: Kentucky families with lower, stable incomes including fixed income and disability benefits

USDA 502 Guaranteed Loan Program (Kentucky Moderate-Income Buyers)

Income Requirements: Up to 115% of Kentucky area median income

Funding Source: Private Kentucky lenders with USDA guarantee

Get Pre-Qualified: Work with a Kentucky lender experienced in USDA rural housing loans

Property Inspection: Have any potential foreclosure or fixer-upper thoroughly inspected early

Select Appropriate Program: Determine whether Direct or Guaranteed better suits your circumstances

Prepare Documentation: Gather income verification, tax returns, benefit award letters, and other required paperwork

Frequently Asked Questions About Kentucky USDA Rural Housing Loans

Can I use a Kentucky USDA loan to purchase a foreclosed property?

Yes, if the foreclosed home meets all USDA livability and safety standards.

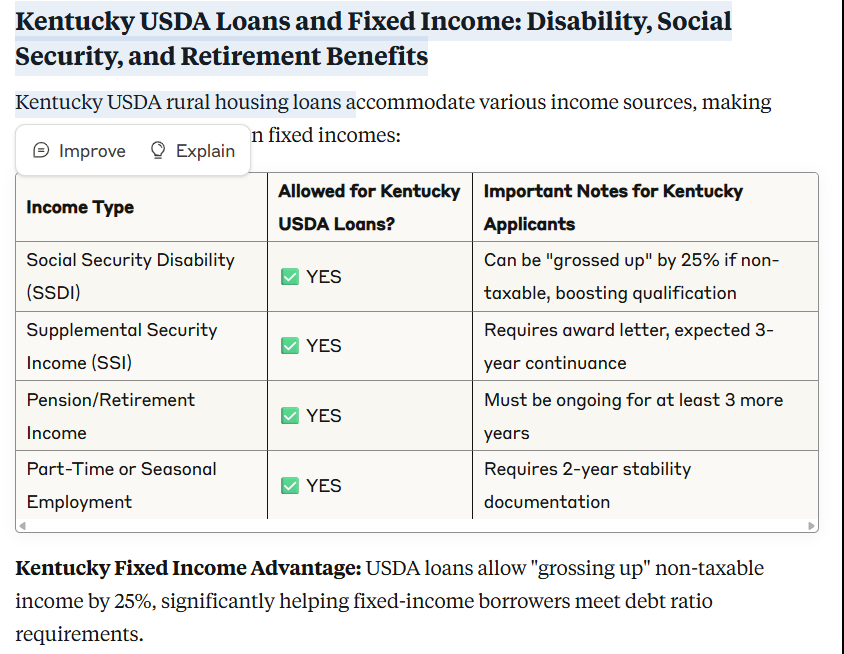

Do Kentucky USDA loans accept disability income for qualification?

Absolutely. Both SSI and SSDI are eligible income sources and can often be “grossed up” by 25% if non-taxable.

What if my desired Kentucky property needs repairs?

USDA Guaranteed loans may allow an escrow holdback for minor repairs (typically up to $10,000). Major issues will disqualify the property.

How do Kentucky’s 502 Direct loans differ from Guaranteed loans?

Direct loans are specifically for very low-income borrowers with tighter restrictions; Guaranteed loans accommodate moderate-income buyers and utilize private lenders. View Kentucky income limits here.

Are manufactured homes eligible for Kentucky USDA loans?

Yes, provided they meet HUD standards and are permanently attached to a foundation.

Can I combine Kentucky Housing Corporation down payment assistance with USDA?

Yes, KHC programs can often be paired with USDA loans for additional assistance.

Get Expert Help With Your Kentucky USDA Rural Housing Loan

Need assistance navigating Kentucky’s USDA rural housing loan options? Our experienced mortgage professionals specialize in helping Kentucky homebuyers with fixed income, disability benefits, and unique financing needs.

Chapter 13 Bankruptcy and Mortgage Loans: Buying a Home in Kentucky

Are you currently in or have recently completed a Chapter 13 bankruptcy and want to buy a home in Kentucky? Navigating the mortgage process after bankruptcy can feel overwhelming, but it’s entirely possible to qualify for a home loan with the right knowledge and preparation. Here’s what you need to know about how Chapter 13 bankruptcy impacts your ability to qualify for popular mortgage loan programs like FHA, VA, USDA, and Fannie Mae.

Chapter 13 bankruptcy can impact your ability to qualify for various mortgage loan programs like FHA, VA, USDA, and Fannie Mae. Here are the details for each program regarding waiting times, credit score requirements, down payment, and qualification criteria after a Chapter 13 bankruptcy:

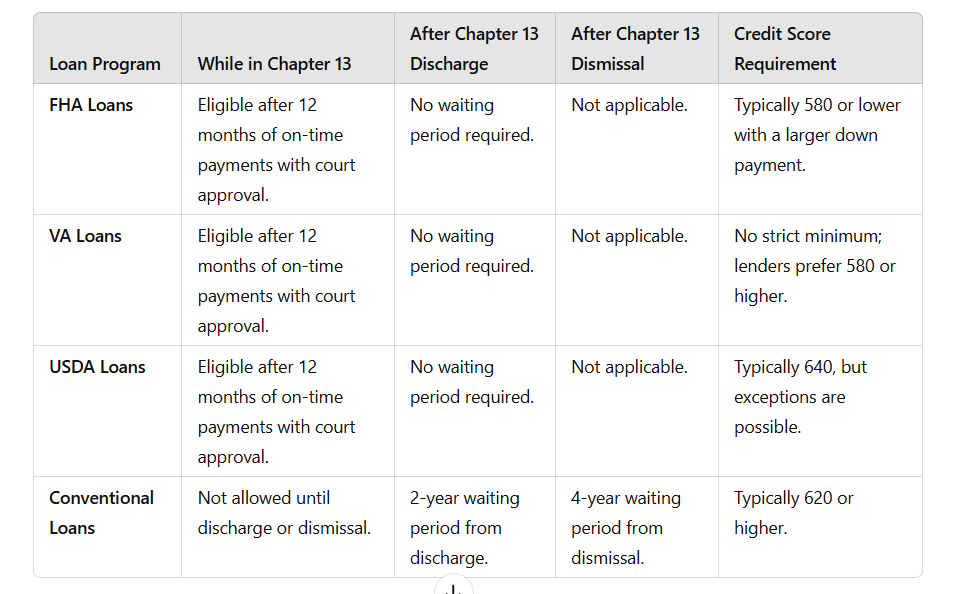

Waiting Time: Typically, you’ll need to wait at least two years after the discharge date of your Chapter 13 bankruptcy before applying for an FHA loan.

Credit Score: FHA loans are known for their flexibility with credit scores. While there’s no specific minimum score, a higher score (usually around 580 or above) can help you qualify for better terms.

Down Payment: The down payment requirement for an FHA loan after Chapter 13 bankruptcy is relatively low, usually starting at 3.5% of the purchase price.

Qualification with Chapter 13 Bankruptcy: To qualify, you must demonstrate that you’ve made all Chapter 13 payments on time for at least one year and receive approval from the bankruptcy court to take on new debt.

Waiting Time: The waiting time for a VA loan after Chapter 13 bankruptcy is generally two years from the discharge date.

Credit Score: VA loans also have flexible credit score requirements, with many lenders looking for scores around 620 or higher.

Down Payment: VA loans are known for offering zero-down financing, but eligibility depends on your military service record and whether you’ve used your VA loan benefits before.

Qualification with Chapter 13 Bankruptcy: Similar to FHA, you’ll need to demonstrate a consistent payment history under your Chapter 13 plan and receive approval from the bankruptcy court.

Waiting Time: USDA loans typically require a waiting period of three years from the discharge date of your Chapter 13 bankruptcy.

Credit Score: While there’s no official minimum credit score, most lenders look for scores of 640 or higher for USDA loans.

Down Payment: USDA loans offer low to no down payment options, making them attractive for eligible borrowers in rural areas.

Qualification with Chapter 13 Bankruptcy: You’ll need to show that you’ve been making timely payments under your Chapter 13 plan for at least one year and obtain approval from the bankruptcy court.

Waiting Time: Fannie Mae typically requires a waiting period of two years from the discharge date of your Chapter 13 bankruptcy.

Credit Score: Fannie Mae loans often have stricter credit score requirements compared to FHA, VA, and USDA loans. A score of around 620 or higher is generally needed.

Down Payment: Down payment requirements vary based on the type of Fannie Mae loan you apply for, but they can range from 3% to 20%.

Qualification with Chapter 13 Bankruptcy: You’ll need to demonstrate responsible financial management after bankruptcy, including rebuilding your credit and showing a stable income.

In all cases, it’s essential to work with a knowledgeable mortgage broker like Joel Lobb, who can guide you through the specific requirements and help you navigate the loan application process after a Chapter 13 bankruptcy.

Website:

Website:  Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204

.jpg)