How Can I Get Rid of Mortgage Insurance for a Rural Housing Loan In Kentucky?

USDA’s Mortgage insurance is for the life of the loan

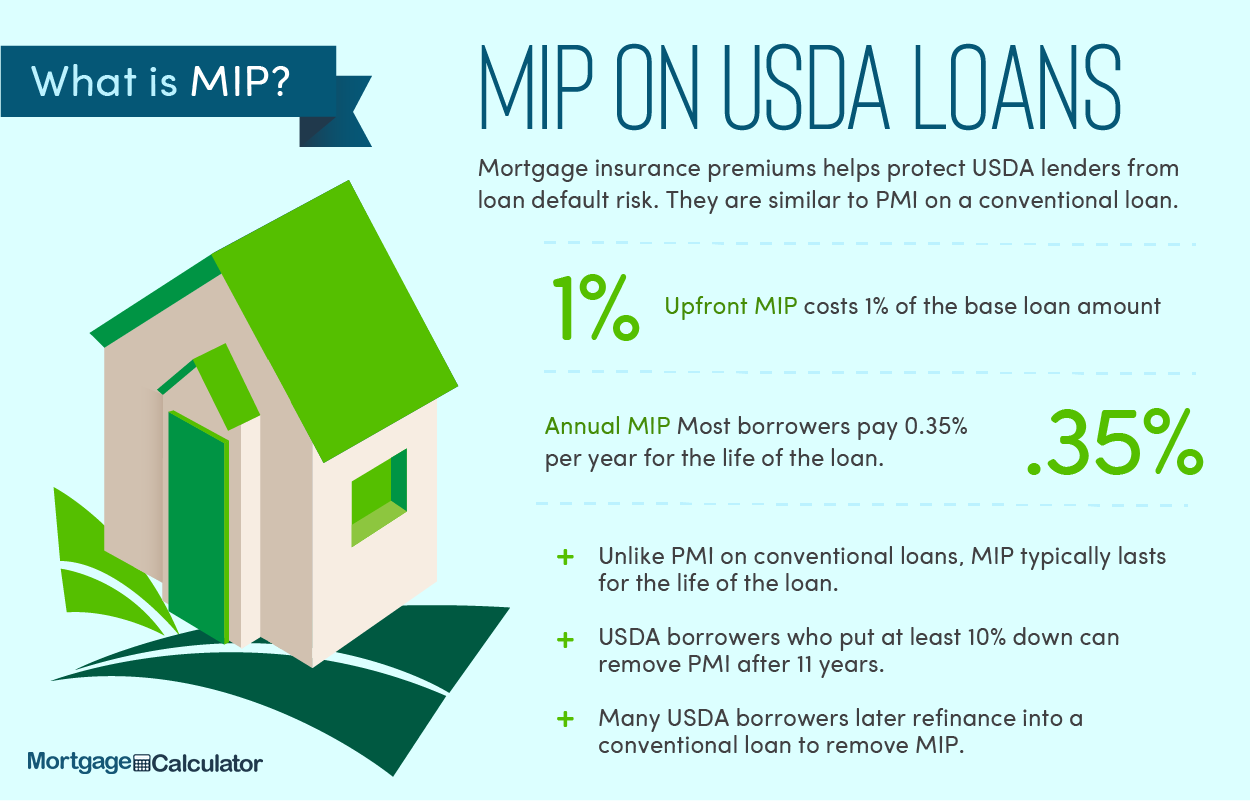

Mortgage insurance advantages & strategies for lower down payment and payment USDA has an annual fee which is similar to private monthly mortgage insurance premiums and an upfront guarantee fee paid to USDA at closing that is currently equal to 1% of the loan amount.

The annual fee is recalculated each year based on the new balance of the mortgage. The annual fee is currently only .35 which began October 1, 2016.

The annual fee percentage on USDA loans stays for the entire 30 year term but because it is based on the annual mortgage balance. Therefore, the dollar amount decreases each year.

How to calculate monthly mortgage insurance for Kentucky USDA loans:

Take Loan amount x 1.0101% (USDA funding fee) x .0035 / 12 = monthly

fee to include in the monthly mortgage payment.

So on a $100,000 sales price, going no money down, this would yield a total loan amount of $101,000 with a monthly mortgage insurance premium of $29.45 a month.

This is very cheap mortgage insurance when compared to an Kentucky FHA loan.

Here are a few reminders about the Kentucky USDA Rural Housing Service (RHS) Section 502 Guaranteed program which provides very-low-, low- and moderate-income rural residents access to affordable housing finance options with little or no down payment or out-of-pocket costs.

• Eligibility Link – Access the USDA Home page, click here.

• Income – To determine eligibility of an applicant/household, click here.

• Property Eligibility – To determine whether the property is located in a designated rural area, click here.s

30 year fixed rate loan terms only, Purchase or refinance, If refinancing must be existing USDA home loan. No cash out allowed.

• Occupancy – Owner occupied only.

• Maximum Loan Amount-No max loan amount

• Max DTI – GUS approved, generally 45% (front end sensitive)/ Manual 29/41.

• Guaranty Fee/Annual Fee – there is a 1.00%/ 0.35% (monthly).

• Down Payment – Down payment not required but if any cash to close, must be borrowers own funds. Gifts are not allowed.

• Interested Third Party Contributions – An amount of 6% of the sales price can be contributed towards closing costs.

.

If you meet income eligibility requirements and are looking to settle in a rural area, you might qualify for the KY USDA Rural Housing program. The program guarantees qualifying loans, reducing lenders’ risk and encouraging them to offer buyers 100% loans. That means Kentucky home buyers don’t have to put any money down, and even the “upfront fee” (a closing cost for this type of loan) can be rolled into the financing.

Fico scores usually wanted for this program center around 620 range, with most lenders wanting a 640 score so they can obtain an automated approval through GUS. GUS stands for the Guaranteed Underwriting system, and it will dictate your max loan pre-approval based on your income, credit scores, debt to income ratio and assets.

CREDIT SCORES UNDERWRITING USDA MORTGAGE FOR RURAL HOUSING

This attachment illustrates the approach to reviewing credit history when a loan is

manually underwritten by an approved lender. Credit score over 680: Perform a basic level of underwriting to confirm the

applicant has an acceptable credit reputation. Perform additional analysis if the

applicant’s credit history has indicators of unacceptable credit as noted in Paragraph 10.7 of this Chapter. Credit score 679 to 640: Perform a comprehensive level of underwriting.

Underwrite all aspects of the applicant’s credit history to establish the applicant has an

acceptable credit reputation. Credit scores in this range indicate the applicant’s

reputation is uncertain and will require a thorough analysis by the underwriter of the

credit to draw a logical conclusion about the applicant’s commitment to making

payments on the new mortgage obligation. The applicant’s credit history should

demonstrate his or her past willingness and ability to meet credit obligations. Credit score less than 640: Perform a cautious level of underwriting. Perform a

detailed review of all aspects of the applicant’s credit history to establish the applicant’s

willingness to repay and ability to manage obligations as agreed. Unless there are

extenuating circumstances documented in accordance with this Chapter, a credit score in this range is generally viewed as a strong indication that the applicant does not have an acceptable credit reputation. Little or no credit history: The lack of credit history on the credit report may be

mitigated if the applicant can document a willingness to pay recurring debts through

other acceptable means such as third party verifications or cancelled checks. Due to

impartiality issues, third party verifications from relatives of household members are not

permissible. Lenders can develop a Non-Traditional Credit Report for applicants who

do not have a credit score in accordance with Paragraph 10.6 of this Chapter.

An applicant with an outstanding judgment obtained by the United States in a

Federal court, other than the United States Tax Court, is not eligible for a guarantee

unless otherwise stated in this Chapter.They also allow for a manual underwrite, which states that the max house payment ratios are set at 29% and 41% respectively of your income.

See link here for more detailed guidelines for credit score, disputed accounts, foreclosures, trade line requirements bankruptcies below:

Indicators of unacceptable credit. The following indicators require documentation

meeting the criteria of Section 10.8 to approve an applicant’s loan request for manually

underwritten loans: Foreclosure and Bankruptcy Guidelines

Foreclosure within 3 years:

Including pre-foreclosure activity, such as a pre-foreclosure sale or short sale

in the previous 3 years (refer to Attachment 10-B for additional guidance);

Bankruptcy within 3 years:

Chapter 7 bankruptcy discharged in the previous 3 years;

An elapsed period of less than 3 years, but not less than 12 months, may

be acceptable if the applicant meets the criteria of Section 10.8 of this

Chapter.

Chapter 13 bankruptcy that has yet to complete repayment (repayment plan in

progress) or has completed payment in the most recent 12 months.

Plans that are completed for 12 months or greater do not require a credit

exception in accordance with Section 10.8;

Late mortgage payments if any mortgage trade line during the most recent 12

months shows 1 or more late payments of greater than 30 days

Collections Accounts

.

In an effort to minimize future risk of open collections left unpaid, the lender will

consider the following during the capacity analysis of the loan request, regardless of the

method utilized to underwrite:

1) Determine if the total outstanding balance of all collections accounts of all

applicants is equal to or greater than $2,000. Unless excluded by state law,

collection accounts of a non-purchasing spouse in a community property state are

included in the cumulative balance of all collections.

2) Remove all medical collections and all types of charge off accounts from the total

balance. Medical collections and charge off accounts must be clearly identifiable

on the credit report.

3) If the remaining outstanding balance of collection accounts are equal to or greater

than $2,000, any of the following actions will apply:

a. Payment in full of all collection accounts at or prior to closing.

b. Payment arrangements are made with each creditor for each collection

account remaining outstanding. A letter from the creditor or evidence on

the credit report is required to validate the payment arrangements. The

agreed upon monthly payment for each outstanding collection account

will be included in the borrower’s debt-to-income ratio.

c. In the absence of a payment arrangement, the lender will utilize in the

debt-to-income ratio a calculated monthly payment. For each collection

utilize 5% of the outstanding balance to represent the monthly payment.

They loan requires no down payment, and the current mortgage insurance is 1% upfront, called a funding fee, and .35% annually for the monthly mi payment. Since they recently reduced their mi requirements, USDA is one of the best options out there for home buyers looking to buy in a rural area.

A rural area typically will be any area outside the major cities of Louisville, Lexington, Paducah, Bowling Green, Richmond, Frankfort, and parts of Northern Kentucky.

There is also a max household income limits with most cutoff starting at $87,000 for a family of four, and up to $115,000 for a family of five or more.

Kentucky FHA, VA, USDA & Rural Housing, KHC and Fannie Mae mortgage loans.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Good News for Kentucky First Time Home Buyers Using the USDA Rural Housing Loan Program!

Kentucky RHS USDA Mortgage Insurance Changes Below and Important Dates to Keep in Mind that could affect your loan closing and approval!

On October 1, 2016, both the upfront guarantee fee and annual fee for purchase and refinance loans will decrease. We are reducing the upfront guarantee fee from 2.75% to 1%, and the annual fee from .5% to .35%. The Guaranteed Underwriting System (GUS) will be updated on August 31, 2016, to allow lenders to select and underwrite using either the FY16 or FY17 fee schedule.

Due to the large volume of loan applications received daily, as well as current turn times, Kentucky will begin accepting applications using the new FY17 fee schedule on September 27, 2016

Applications using the new FY17 fee schedule submitted before September 27, 2016 will not be processed before October 1, 2016.

September 27, 2016 will be the last day Kentucky will accept applications using the existing FY16 fee schedule. This will ensure all of these submissions are reviewed by the Agency prior to October 1.

Most are familiar with USDA Rural Housing Loan Program being a great no money down program available and it is not just for Kentucky first time buyers.

But starting with commitments on October 1, the funding fee that is financed is going from 2.75% to only 1%! On a $100,000 loan, a buyer saves about $1750! In addition, the annual fee (like PMI) reduces from .5% to .35% which lowers the monthly payment by $15 a month on an $100,000 loan amount.

Joel Lobb

Senior Loan Officer

(NMLS#57916 text or call my phone: (502) 905-3708 email me at kentuckyloan@gmail.com

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). USDA Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice. Manufactured and mobile homes are not eligible as collateral.

USDA has just announced that they are planning to lower both the Guarantee Fee and the Annual Fee for RHS loans in Fiscal Year 2017. Effective for loans receiving commitments from RHS on or after October 1, 2016, the following fee changes will be in effect

The Upfront Guarantee Fee will be lowered from 2.75% to 1.00% of the loan amount

The Annual Fee will be lowered from 0.50% to 0.35% of the average scheduled unpaid principal balance for the life of the loan

RHS Increase in Annual Fee for Rural Housing Mortgage Loans in Kentucky

Kentucky USDA Mortgage Lenders must underwrite the loan using an annual fee of .5 percent and resubmit the application to RD in GUS after October 1, 2014

On Wednesday, October 1, 2014, the annual fee for both purchase and refinance loans will increase from .4 percent to .5 percent. The Guaranteed Underwriting System (GUS) has been updated to allow lenders to select and underwrite at either the .4 percent or .5 percent annual fee structure. Lenders should communicate with Rural Development (RD) offices to understand current processing time-frames.

GUS “Final Submissions” with an annual fee of .4 percent, that areissued a conditional commitment by RD prior to the close of business on Tuesday, September 30, 2014, will not be affected by the annual fee change. Those submissions that are not issued a conditional commitment by RD prior to the close of business on Tuesday, September 30, will be affected by the annual fee change.

Lenders must underwrite the loan using an annual fee of .5 percent and resubmit the application to RD in GUS.