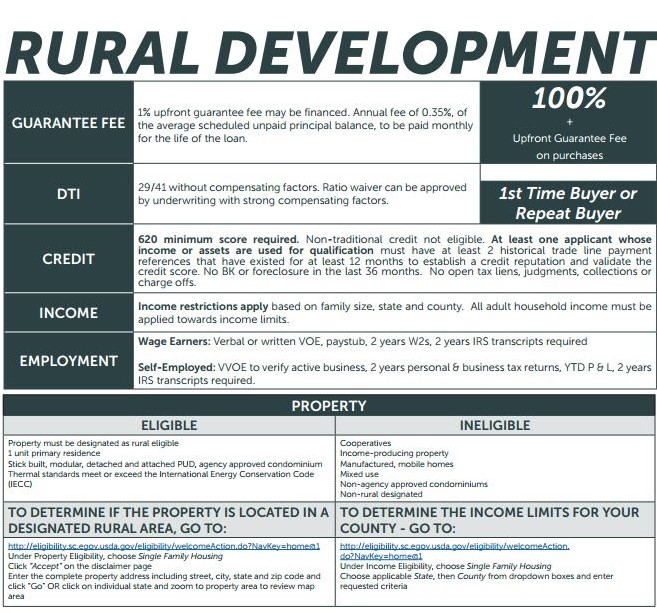

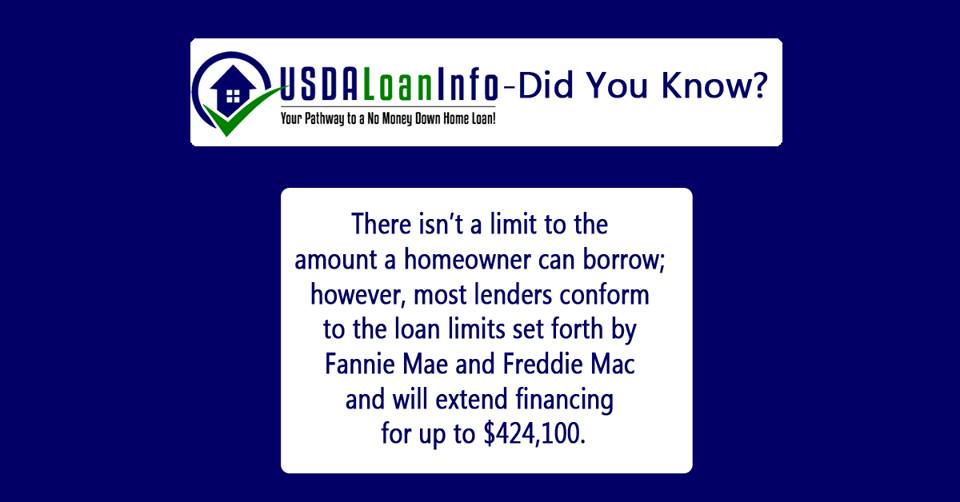

RHS Funding Now Available for Kentucky Rural Housing Mortgage Loans for 2022

Funding has now been authorized for RHS loans.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the views of my employer. Not all products or services mentioned on this site may fit all people