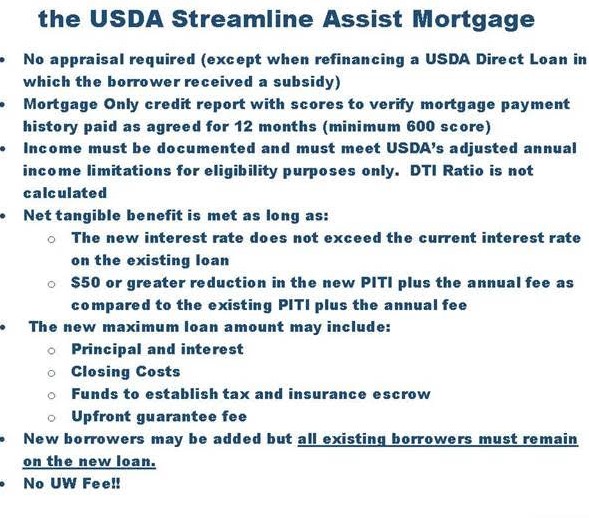

You can refinance your existing USDA Rural Housing Loan. See details below:

KENTUCKY USDA LOAN GUARANTEED RURAL HOUSING REFINANCE FEATURES

- Loan must be secured by the same property as the original loan. The original loan must be Guaranteed Rural Housing (GRH) or USDA Section 502 Direct only. The Program may not be used to refinance FHA, VA, or other government or conventional mortgages.

- Term of the new loan will be 30 years.

- Interest rate of the new loan cannot exceed the interest rate of the loan being refinanced. However, the interest rate of the new loan does not have to meet the interest rate requirements established in RD Instruction 1980-D, §1980.320 Interest rate.

- Property must be owned and occupied by the borrowers as their principal residence.

- The guarantee fee is 1.00% of the total principal obligation of the new loan.

- The 1.00% guarantee fee may be always financed into any GRH refinancing transaction. As usual, borrowers may finance other closing costs and fees up to 100% of the current appraised value. However, it is possible for the loan-to-value (LTV) of the new loan to reach 101% if the 1% guarantee fee is financed. Loans may exceed 100% LTV only to the extent that the excess represents a financed guarantee fee of no more than 1.00%.

- Total household income cannot exceed the moderate level for the area as established in RD Instruction 1980-D, Exhibit C.

- GRH refinance loans are permitted for properties in areas that have been determined to be non-rural since the existing loan was made.

- Applicants are not eligible to receive “cash out” from the refinancing transaction. However, applicants may receive reimbursement from loan proceeds at settlement for their personal funds advanced for eligible loan purposes that are part of the refinance transaction, such as an appraisal fee or credit report fee. At loan closing, a nominal amount of “cash out” to the applicants (beyond reimbursement of these “prepaid” items) may occasionally result due to final escrow and interest calculations. This amount, if any, must be applied to a principal reduction of the new loan.

- Subordinate financing such as home equity seconds and down payment assistance “silent” seconds cannot be included in the new loan amount. Any existing secondary financing must be subordinate to the new first lien.

- Maximum loan amount cannot exceed the balance of the loan being refinanced, plus the guarantee fee, and reasonable and customary closing costs, including funds necessary to establish a new escrow account.

- Unpaid fees, such as late fees due the current servicer, are not eligible to be included in the new loan amount.

- eligible areas on USDA Rural Development’s web-site at:

- http://eligibility.sc.egov.usda.govhttp://eligibility.sc.egov.usda.gov

EVO Mortgage

911 Barret Ave, Louisville, KY 40204

Text or call: 502-905-3708

email: kentuckyloan@gmail.com

NMLS #57916 | Company NMLS #1738461

Equal Housing Lender

| For commitments issues on or after October 1, 2016:

USDA charges the lender, who can pass the charge to the borrower, a one-time up-front cost, which is known as a Guarantee Fee. The Guarantee Fee can be financed in addition to the maximum base loan amount. The Guarantee Fee is calculated as follows as of October 1, 2016:

CALCULATION FOR REFINANCE TRANSACTIONS:

ANNUAL FEE:

|

||||||

| REPAYMENT RATIOS REFINANCE | FOR BOTH GUARANTEED LOAN TO GUARANTEED LOAN AND DIRECT LOAN TO GUARANTEED LOAN: USDA – GUS Approved USDA – Manual Underwrite – Must meet USDA guideline maximum debt ratios of 29 & 41%–No Exceptions Allowed. |

|||||

| TERM OF NEW LOAN | FOR BOTH GUARANTEED LOAN TO GUARANTEED LOAN AND DIRECT LOAN TO GUARANTEED LOAN: TERM OF THE NEW LOAN WILL BE A 30 YEAR FULLY AMORTIZED FIXED RATE MORTGAGE ONLY. |

|||||

| INTEREST RATE |

|

|||||

| HOUSEHOLD INCOME | Total adjusted income for the household cannot exceed the moderate level for the area as established in HB-1-3555. | |||||

| LOAN SECURITY |

|

|||||

| RURAL / NONRURAL AREAS | SFHGLP refinance loans are permissible for properties in areas that have been determined to be non-rural since the existing loan was made. | |||||

| PROPERTY VALUATION |

|

|||||

| INSPECTIONS |

|

|||||

| NET TANGIBLE BENEFIT | Every refinance | |||||

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the views of my employer. Not all products or services mentioned on this site may fit all people

Reblogged this on and commented:

For commitments issues on or after October 1, 2016:

USDA charges the lender, who can pass the charge to the borrower, a one-time up-front cost, which is known as a Guarantee Fee. The Guarantee Fee can be financed in addition to the maximum base loan amount. The Guarantee Fee is calculated as follows as of October 1, 2016:

PURCHASE TRANSACTION CALCULATION:

1.00% of the TOTAL loan amount for commitments issued on or after 10/1/16.

Calculation: Base loan amount divided by .99 = Total loan amount (round down to nearest dollar). Total loan is then multiplied by 1.00% to get the amount of the guarantee fee.

A Guarantee Fee & Annual Fee (monthly) Calculator can be found on the USDA training resource website.

CALCULATION FOR REFINANCE TRANSACTIONS:

1.00% of the TOTAL loan amount for commitments issued on or after 10/1/16.

Calculation: Base loan amount divided by .99 = Total loan amount (round down to nearest dollar). Total loan is then multiplied by 1.00% to get the amount of the guarantee fee.

A Guarantee Fee & Annual Fee (monthly) Calculator can be found on the USDA training resource website.

ANNUAL FEE:

All loan transactions will include an annual fee of .35%

REPAYMENT RATIOS REFINANCE

FOR BOTH GUARANTEED LOAN TO GUARANTEED LOAN AND DIRECT LOAN TO GUARANTEED LOAN:

USDA – GUS Approved

USDA – Manual Underwrite – Must meet USDA guideline maximum debt ratios of 29 & 41%–No Exceptions Allowed.

TERM OF NEW LOAN

FOR BOTH GUARANTEED LOAN TO GUARANTEED LOAN AND DIRECT LOAN TO GUARANTEED LOAN:

TERM OF THE NEW LOAN WILL BE A 30 YEAR FULLY AMORTIZED FIXED RATE MORTGAGE ONLY.

INTEREST RATE

Interest rate of the new loan must be a fixed rate.

The interest rate must be lower than the existing loan to be refinanced.

Funded buy down accounts are not permitted.

HOUSEHOLD INCOME

Total adjusted income for the household cannot exceed the moderate level for the area as established in HB-1-3555.

LOAN SECURITY

Loan security must include the same property as the original loan.

The security property must be owned and occupied by the applicants as their principal residence.

RURAL / NONRURAL AREAS

SFHGLP refinance loans are permissible for properties in areas that have been determined to be non-rural since the existing loan was made.

PROPERTY VALUATION

The value of the new mortgage loan request must be supported by a new appraisal. The loan amount cannot exceed the present market value plus the one-time 2 percent guarantee fee. The new loan amount can include closing costs or lender fees if supported by market value.

INSPECTIONS

The lender must confirm the property meets or continues to meet the current requirements of HUD Handbook 4150.2 and 4905.1.

No further inspections or repairs required by Rural Development.

Lender may require inspections or repairs. Expenses related to inspections or repairs may not be financed.

NET TANGIBLE BENEFIT

Every refinance