I am a Kentucky based USDA Mortgage Lender that has originated over 300 KY Rural Housing Mortgage Loans in Kentucky-CALL OR TEXT 502-905-3708 FOR USDA MORTGAGE LOAN

100% financing · No down payment · Fixed 30-year rate

0%

Down payment required

100%

Financing available

620+

Typical credit score

Key benefits — click to expand

No down payment

Click to learn more ›

Borrowers without savings — or who wish to keep their savings — can qualify. Closing costs may also be financed if the appraised value exceeds the purchase price.

Low mortgage insurance

Click to learn more ›

USDA has the lowest upfront and monthly mortgage insurance of any 100% loan program — keeping your monthly payment as low as possible on a 30-year fixed rate.

Flexible credit guidelines

Click to learn more ›

No minimum credit score is set by USDA, though lenders typically require 620–640. Borrowers with a 640+ score enjoy streamlined processing with no credit explanation letters needed.

Generous income limits

Click to learn more ›

Income limits are based on 115% of the U.S. median. Deductions apply for dependents, child-care expenses, and elderly households — making it easier for Kentucky families to qualify.

Not just first-time buyers

Click to learn more ›

Any qualified buyer may use a USDA loan — not only first-time homebuyers. Sellers are also permitted to pay the buyer’s closing costs, further reducing out-of-pocket expenses.

Rural areas across Kentucky

Click to learn more ›

Eligible areas include open country and towns with a population of 10,000 or less. Many Kentucky communities outside major metros qualify — check eligibility at the USDA website.

Debt-to-income ratio guidelines

Housing (PITI)

≤ 29%

Total debt

≤ 41%

Buyers with satisfactory credit may qualify with higher ratios in high-cost areas.

Joel Lobb · Mortgage Loan Officer · NMLS #57916 · Company NMLS #1738461

Equal Housing Lender · Kentucky mortgage loans only

This page is not endorsed by USDA, FHA, VA, or any government agency.

Get Expert Help With Your Kentucky USDA Rural Housing Loan that is a foreclosure or fixer-upper with fixed income

Are you considering a USDA rural housing loan in Kentucky to purchase a foreclosed property or fixer-upper home? This comprehensive guide walks Kentucky homebuyers through everything you need to know about USDA 502 Direct and Guaranteed loans. It is especially useful if you are living on fixed income. It’s also helpful for those on Social Security benefits, disability payments, or lower wages.

Can Kentucky Residents Use USDA Rural Housing Loans for Foreclosures or Fixer-Uppers?

Yes, with important conditions. While USDA loans offer an excellent path to affordable homeownership in rural Kentucky communities, these properties must meet specific standards:

The home must be structurally sound

The property must be move-in ready (safe and sanitary)

All essential systems must be functional

The property must be located in a USDA-eligible rural area in Kentucky

Many Kentucky foreclosures can qualify for USDA financing if they’re in good condition or if repairs are completed before closing.

Kentucky USDA Loan Programs: Which Works Best for Your Situation?

Kentucky homebuyers have two primary USDA rural housing loan options:

USDA 502 Direct Loan Program (Kentucky Low-Income Buyers)

Income Requirements: 50-80% of Kentucky area median income

Funding Source: Direct from USDA (government-funded)

Perfect For: Very low to low-income Kentucky residents

Credit Flexibility: Higher flexibility with manual underwriting

Down Payment: $0 down payment required

Mortgage Insurance: Lower annual fee (0.35%)

DTI Ratios: May permit higher DTI with strong residual income

Asset Restrictions: Stricter requirements (cannot have excessive assets)

Best For: Kentucky families with lower, stable incomes including fixed income and disability benefits

USDA 502 Guaranteed Loan Program (Kentucky Moderate-Income Buyers)

Income Requirements: Up to 115% of Kentucky area median income

Funding Source: Private Kentucky lenders with USDA guarantee

Get Pre-Qualified: Work with a Kentucky lender experienced in USDA rural housing loans

Property Inspection: Have any potential foreclosure or fixer-upper thoroughly inspected early

Select Appropriate Program: Determine whether Direct or Guaranteed better suits your circumstances

Prepare Documentation: Gather income verification, tax returns, benefit award letters, and other required paperwork

Frequently Asked Questions About Kentucky USDA Rural Housing Loans

Can I use a Kentucky USDA loan to purchase a foreclosed property?

Yes, if the foreclosed home meets all USDA livability and safety standards.

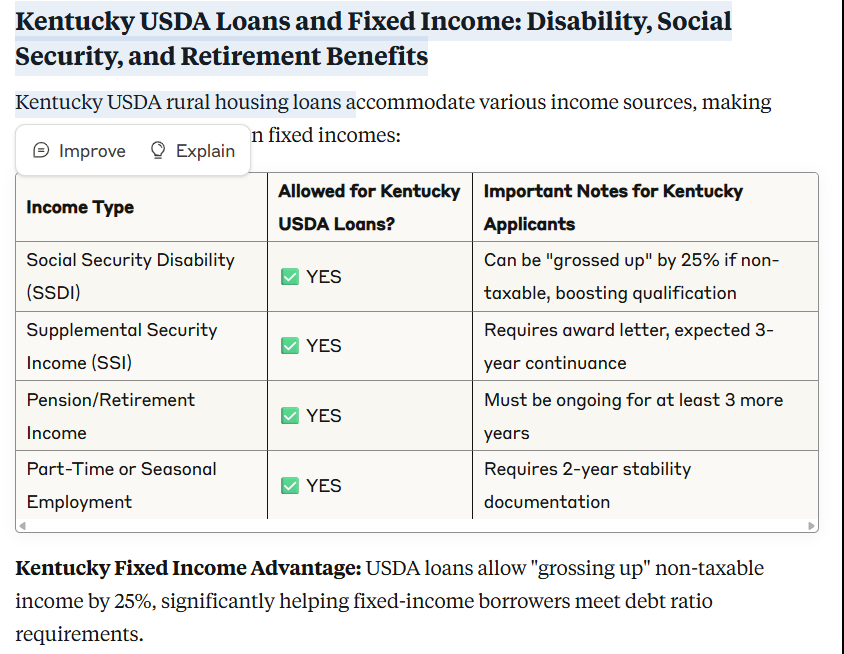

Do Kentucky USDA loans accept disability income for qualification?

Absolutely. Both SSI and SSDI are eligible income sources and can often be “grossed up” by 25% if non-taxable.

What if my desired Kentucky property needs repairs?

USDA Guaranteed loans may allow an escrow holdback for minor repairs (typically up to $10,000). Major issues will disqualify the property.

How do Kentucky’s 502 Direct loans differ from Guaranteed loans?

Direct loans are specifically for very low-income borrowers with tighter restrictions; Guaranteed loans accommodate moderate-income buyers and utilize private lenders. View Kentucky income limits here.

Are manufactured homes eligible for Kentucky USDA loans?

Yes, provided they meet HUD standards and are permanently attached to a foundation.

Can I combine Kentucky Housing Corporation down payment assistance with USDA?

Yes, KHC programs can often be paired with USDA loans for additional assistance.

Get Expert Help With Your Kentucky USDA Rural Housing Loan

Need assistance navigating Kentucky’s USDA rural housing loan options? Our experienced mortgage professionals specialize in helping Kentucky homebuyers with fixed income, disability benefits, and unique financing needs.

Chapter 13 Bankruptcy and Mortgage Loans: Buying a Home in Kentucky

Are you currently in or have recently completed a Chapter 13 bankruptcy and want to buy a home in Kentucky? Navigating the mortgage process after bankruptcy can feel overwhelming, but it’s entirely possible to qualify for a home loan with the right knowledge and preparation. Here’s what you need to know about how Chapter 13 bankruptcy impacts your ability to qualify for popular mortgage loan programs like FHA, VA, USDA, and Fannie Mae.

Chapter 13 bankruptcy can impact your ability to qualify for various mortgage loan programs like FHA, VA, USDA, and Fannie Mae. Here are the details for each program regarding waiting times, credit score requirements, down payment, and qualification criteria after a Chapter 13 bankruptcy:

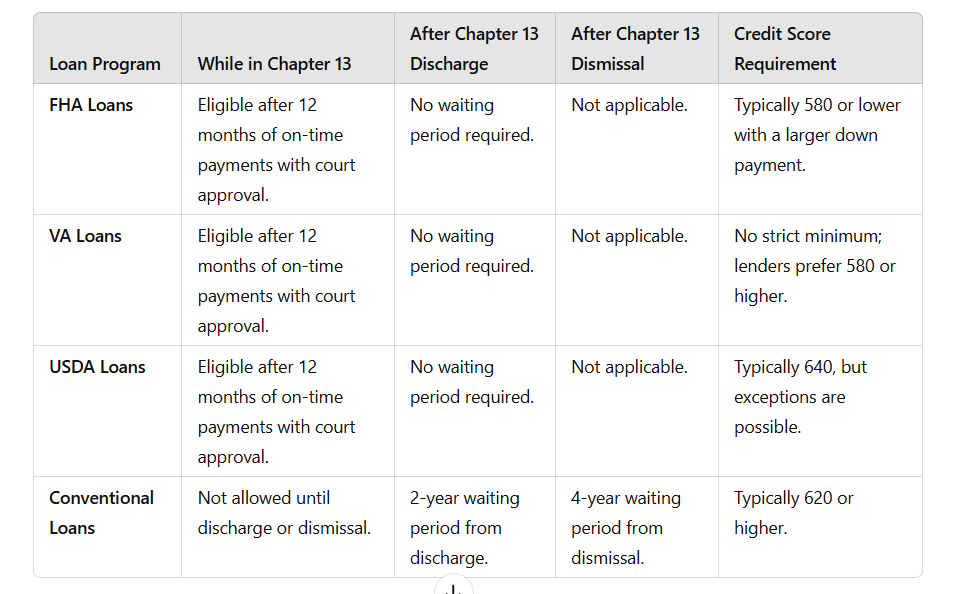

Waiting Time: Typically, you’ll need to wait at least two years after the discharge date of your Chapter 13 bankruptcy before applying for an FHA loan.

Credit Score: FHA loans are known for their flexibility with credit scores. While there’s no specific minimum score, a higher score (usually around 580 or above) can help you qualify for better terms.

Down Payment: The down payment requirement for an FHA loan after Chapter 13 bankruptcy is relatively low, usually starting at 3.5% of the purchase price.

Qualification with Chapter 13 Bankruptcy: To qualify, you must demonstrate that you’ve made all Chapter 13 payments on time for at least one year and receive approval from the bankruptcy court to take on new debt.

Waiting Time: The waiting time for a VA loan after Chapter 13 bankruptcy is generally two years from the discharge date.

Credit Score: VA loans also have flexible credit score requirements, with many lenders looking for scores around 620 or higher.

Down Payment: VA loans are known for offering zero-down financing, but eligibility depends on your military service record and whether you’ve used your VA loan benefits before.

Qualification with Chapter 13 Bankruptcy: Similar to FHA, you’ll need to demonstrate a consistent payment history under your Chapter 13 plan and receive approval from the bankruptcy court.

Waiting Time: USDA loans typically require a waiting period of three years from the discharge date of your Chapter 13 bankruptcy.

Credit Score: While there’s no official minimum credit score, most lenders look for scores of 640 or higher for USDA loans.

Down Payment: USDA loans offer low to no down payment options, making them attractive for eligible borrowers in rural areas.

Qualification with Chapter 13 Bankruptcy: You’ll need to show that you’ve been making timely payments under your Chapter 13 plan for at least one year and obtain approval from the bankruptcy court.

Waiting Time: Fannie Mae typically requires a waiting period of two years from the discharge date of your Chapter 13 bankruptcy.

Credit Score: Fannie Mae loans often have stricter credit score requirements compared to FHA, VA, and USDA loans. A score of around 620 or higher is generally needed.

Down Payment: Down payment requirements vary based on the type of Fannie Mae loan you apply for, but they can range from 3% to 20%.

Qualification with Chapter 13 Bankruptcy: You’ll need to demonstrate responsible financial management after bankruptcy, including rebuilding your credit and showing a stable income.

In all cases, it’s essential to work with a knowledgeable mortgage broker like Joel Lobb, who can guide you through the specific requirements and help you navigate the loan application process after a Chapter 13 bankruptcy.

2026 Guide to USDA Rural Housing Loans for Manufactured Homes in Kentucky: No-Money-Down Options, Even with Bad Credit

100% financing available for qualified Kentucky borrower

Table of Contents

Understanding USDA Mobile Home Loans in Kentucky

2026 Game-Changing Updates

Kentucky USDA Rural Housing Loan Requirements

Bad Credit Mobile Home Loans in Kentucky

No Money Down Mobile Home Financing Options

Kentucky Counties Eligible for USDA Mobile Home Loans

Foundation and Installation Requirements

How to Apply for USDA Mobile Home Loans in Kentucky

Alternative Financing Options

Frequently Asked Questions

Understanding USDA Mobile Home Loans in Kentucky

The United States Department of Agriculture (USDA) Rural Development program has been quietly revolutionizing homeownership opportunities across Kentucky for decades. Many potential homebuyers don’t realize this. The USDA’s Single Family Housing Guaranteed Loan Program (SFHGLP) extends far beyond traditional stick-built homes. It also includes manufactured and mobile homes. This opens doors for thousands of Kentucky families who previously thought homeownership was out of reach.

Kentucky, with its vast rural landscapes and small-town communities, is well-suited to USDA rural housing programs. Conventional mortgages often demand large down payments and excellent credit. USDA loans, however, are designed for low- to moderate-income families in rural areas. They are an excellent option for mobile home buyers across the Commonwealth.

What Makes USDA Mobile Home Loans Different

•100% Financing: No money down is required, making it perfect for buyers with limited savings

•Affordable Terms: Competitive interest rates make monthly payments manageable

•Rural Housing Opportunities: Ideal for Kentucky homebuyers in small towns and rural areas

•Flexible Credit Requirements: Holistic approach to creditworthiness evaluation

On March 4, 2025, the USDA officially expanded its Single Family Housing Guaranteed Loan Program. This expansion provides 100% financing for manufactured homes. Industry experts are calling this change the most significant development in rural housing finance in decades.

Key Program Changes

Expanded Eligibility

Manufactured homes now receive the same favorable treatment as traditional homes

Age Restrictions Relaxed

Existing manufactured homes up to 20 years old can now qualify

Streamlined Process

Processing times reduced by 30-40% with new guidelines

Better Credit Pathways

Clearer guidelines for borrowers with credit challenges

Kentucky USDA Rural Housing Loan Requirements

Borrower Requirements

✓Income cannot exceed 115% of area median income

✓Must occupy home as primary residence

✓U.S. citizen, non-citizen national, or qualified alien

✓Credit score typically 580+ (manual underwriting available)

Property Requirements

✓Built to HUD Code standards (post-1976)

✓Permanent foundation required

✓Minimum 12 feet wide, 400 sq ft living space

✓Located in USDA-eligible rural area

Bad Credit Mobile Home Loans in Kentucky

One of the most significant advantages of USDA mobile home loans is their accessibility to borrowers with less-than-perfect credit. Unlike conventional mortgages, which often have rigid credit score requirements, USDA loans offer flexibility. This flexibility recognizes the unique challenges faced by rural borrowers.

Credit Score Guidelines

640+ Credit Score Streamlined Processing

580 and above Credit Score Manual Underwriting

Note: USDA takes a holistic approach to credit evaluation, considering factors beyond just credit scores.

Often Asked Questions

What credit score do I need for a USDA mobile home loan in Kentucky?

While USDA doesn’t set a minimum credit score, most lenders prefer scores of 580 or higher. Borrowers with lower scores may still qualify through manual underwriting, and the program takes a holistic approach to credit evaluation.

Can I buy a used mobile home with a USDA loan?

Yes, existing manufactured homes can qualify if they’re less than 20 years old. They must meet HUD standards. The homes should be properly installed on permanent foundations. Additionally, they need to meet all other USDA requirements.

Do I need to own the land to get a USDA loan for a mobile home?

USDA loans can finance both the manufactured home and land together. They can also finance just the home if you already own suitable land. However, the home must be permanently installed and classified as real property.

What areas of Kentucky are eligible for USDA loans?

Approximately 97% of Kentucky qualifies as rural for USDA purposes. Most areas outside of Louisville, Lexington, and a few other metropolitan centers are eligible. Use the USDA’s online eligibility tool to check specific addresses.

This comprehensive guide provides general information about USDA mobile home loans in Kentucky. It should not be considered as financial or legal advice. Potential borrowers should consult with qualified lenders, real estate professionals, and legal advisors for guidance specific to their situations.

Contact a Kentucky Mobile Home Loan Expert

For personalized guidance on Kentucky USDA mobile home loans, contact a local mortgage specialist. They can help with options for borrowers with bad credit and no down payment. The specialist will understand the unique requirements of manufactured home financing.

Disclaimer: This website is not endorsed by the FHA, VA, USDA, or any government agency. It is an independent platform created to educate and assist Kentucky homebuyers with expert advice and accessible tools.

Can I buy land and a mobile home together with a USDA loan?

USDA loans can finance both the manufactured home and the land in a single transaction. This is possible if both meet USDA eligibility requirements. The combined purchase must not exceed USDA loan limits for your area.

What if my credit score is below 580?

While challenging, approvals are possible with strong compensating factors such as stable employment, low debt-to-income ratios, and cash reserves. Working with an experienced USDA lender who understands manual underwriting is essential. Honestly, best to get score to 620 or 640 range for better changes of loan approval. USDA does not have minimum credit score requirements.

How long does the USDA loan process take?

Typical processing time is 45-60 days from application to closing. Processing is taking longer due to USDA cutbacks. This delay can vary based on property complexity. It also depends on documentation completeness and current USDA processing volumes.

Can I use gift funds for closing costs?

Yes, gift funds from family members are allowed for closing costs and prepaid items. Proper gift documentation and seasoning requirements must be met.

What happens if the home doesn’t appraise for the purchase price?

If the appraisal comes in low, you have several options. You can negotiate with the seller to reduce the price. Another option is to pay the difference in cash. Alternatively, you can cancel the contract if you have an appraisal contingency.

Are there income limits for USDA mobile home loans?

Yes, household income cannot exceed 115% of the Area Median Income for your county. These limits are updated annually and vary significantly across Kentucky.

Can I refinance my existing mobile home with a USDA loan?

USDA offers refinancing options for existing USDA loans, but cannot refinance non-USDA loans. However, if your current mobile home meets USDA requirements, you might qualify for a new purchase loan.

What areas of Kentucky qualify for USDA loans?

Most of Kentucky qualifies as rural under USDA guidelines. Use the USDA eligibility map to verify specific addresses, as eligibility can vary even within the same county.

Ready to explore USDA mobile home loan options in Kentucky? Don’t wait, as these programs have annual funding limits. Working with an experienced local lender who understands manufactured home financing is crucial for success.

For personalized guidance on Kentucky USDA mobile home loans:

.jpg)