I am a Kentucky based USDA Mortgage Lender that has originated over 300 KY Rural Housing Mortgage Loans in Kentucky-CALL OR TEXT 502-905-3708 FOR USDA MORTGAGE LOAN

Kentucky Housing Corporation (KHC) recognizes that down payments, closing costs, and prepaids are stumbling blocks for many potential homebuyers. We offer several loan programs to help you achieve your dream of buying a home. Your KHC-approved lender can help you apply for the program that meets your needs.

<

Kentucky Down Payment Assistance

Your path to homeownership in Kentucky for 2026–2026

Limited time: KHC assistance up to $12,500

KHC Down Payment Assistance

Maximum Assistance

$12,500

15-year repayable second mortgage

Kentucky Housing Corporation

VA Home Loans

$0 Down

No monthly mortgage insurance

Eligible Veterans

USDA Rural Housing

100% Financing

Rural and eligible suburban areas

Income Limits Apply

FHA + KHC

3.5% Down Covered

Flexible credit guidelines

Stackable Assistance

Louisville Metro DPA

$20,000

0% interest, partial forgiveness

Location Specific

Welcome Home Grant

Expected 2026

Non-repayable grant program

Seasonal Funding

Get Started

Mortgage Loan Officer

20+ years experience

1,300+ Kentucky families helped

$2500 Grant from Fannie Mae and Freddie Mac To Buy a home in Kentucky

Kentucky Homeownership just got more affordable for low-to-moderate income Kentucky residents! If you’re planning to buy a home in 2025, you could qualify for a $2,500 grant.

This grant is available through Freddie Mac’s Home Possible® and Fannie Mae’s HomeReady® programs. This limited-time offer can help cover your down payment. It also assists with closing costs. This makes the dream of homeownership more accessible. Let’s break it down!

What Are HomeReady® and Home Possible® Programs?

HomeReady®:

Offered by Fannie Mae, this program provides:

Low down payments as little as 3%.

Flexible mortgage options for borrowers with household incomes below the area median income.

Reduced mortgage insurance requirements, making homeownership more affordable.

620 credit scores or higher

lower mortgage insurance

3 percent down payment

4 years removed from bankruptcy

Home Possible®:

Freddie Mac’s Home Possible® program offers:

3% down payment options for eligible buyers.

Flexible credit terms and lower mortgage insurance premiums.

Special features to assist low-income buyers achieve their homeownership goals.

620 credit scores or higher

lower mortgage insurance

3 percent down payment

4 years removed from bankruptcy

The $2,500 Grant: What You Need to Know

This $2,500 credit can be used toward:

Down payment costs and prepaids for taxes, home insurance and prepaid interest

Closing costs, helping to reduce the financial burden of purchasing a home.

Eligibility Criteria

Property Types: The grant applies to purchases of 1-4 unit properties.

Income Limits: Borrower’s income must not exceed 50% of the Area Median Income (AMI).

Loan Programs: The credit is available exclusively through Fannie Mae’s HomeReady® and Freddie Mac’s Home Possible® loan programs.

Program Duration

Loans must achieve “purchase-ready” status by February 28, 2026.

For loans delivered into mortgage-backed securities (MBS), the deadline is February 1, 2026.

Why Take Advantage of This Program?

This grant is a game-changer for first-time and low-income homebuyers in Kentucky. The financial relief offered helps bridge the gap for individuals and families working toward their goal of owning a home.

Get Started Today!

If you’re ready to make your move, contact an experienced loan officer who specializes in HomeReady® and Home Possible® programs. They can guide you through the eligibility process. They will help you take the next step toward achieving your dream of homeownership with this incredible grant opportunity.

If you’re in Kentucky, don’t miss this chance to access $2,500 in grant assistance. Make your homeownership dream a reality in 2025. For more information, get in touch with a local expert today!

Programs: Available through HomeReady® and Home Possible® loan programs.

Deadlines: Loans must achieve “purchase-ready” status by February 28, 2026.

Don’t miss this opportunity to reduce your upfront homebuying costs. Find out if you qualify and connect with a local loan officer today. These grants are limited and offered for a short time—act before the deadlines pass!

Eligibility Requirements for the $2,500 Grant

This $2,500 credit is available exclusively through Fannie Mae’s HomeReady® mortgage. Here’s what you need to qualify:

1. Mortgage Insurance

If you put less than 20% down, you’ll need mortgage insurance. However:

The insurance is canceled when you reach 80% equity. Unlike FHA loans, they often require mortgage insurance for the loan’s life.

2. Kentucky First-Time or Repeat Homebuyers

You don’t need to be a first-time Kentucky homebuyer to qualify for HomeReady®.

If all borrowers on the loan are first-time buyers, at least one must complete a homeownership education course. This course can be Fannie Mae HomeLier.

Income limits below for Major Cities in Kentucky

Why Choose HomeReady® Over Other Loan Options?

Lower Down Payment: Only 3% is required, compared to 3.5% for FHA loans.

Reduced Mortgage Insurance Costs: Save money over the life of the loan.

Flexible Eligibility: The program is open to both first-time and repeat buyers. The flexibility in household income allows multi-generational income to help you qualify.

How to Get Started

Check Your Eligibility: Use the AMI Lookup Tool to determine if your income qualifies for the grant.

Contact a Lender: Work with a lender who offers HomeReady® mortgages. They can guide you through the application process and help determine your grant eligibility.

Complete a Homebuyer Education Course: If you’re a first-time homebuyer, complete the required course to meet eligibility.

Take the First Step Toward Homeownership in Kentucky

The $2,500 credit from Fannie Mae’s HomeReady® mortgage offers a fantastic way to reduce your upfront costs. It helps make homeownership more affordable. Whether you’re a first-time buyer or looking to upgrade, this grant is here to help.

Don’t miss out on this limited-time opportunity to take advantage of a program designed to help Kentucky homebuyers like you. Start your journey today and make your dream home a reality!

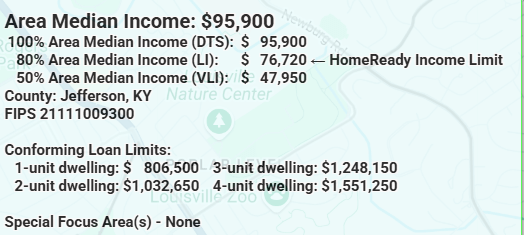

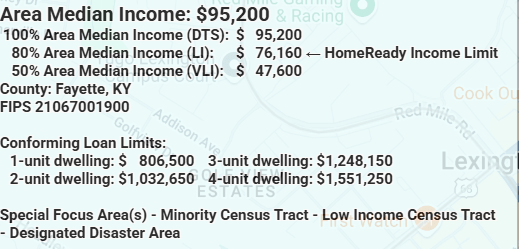

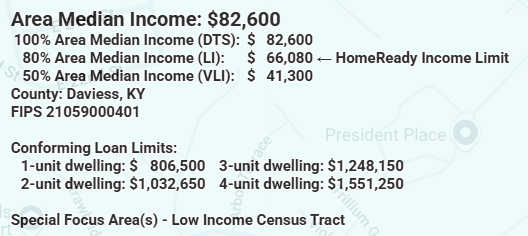

Below is a snapshot of current income limits for Homeready and Home Possible. These are the income limits for Jefferson, Fayette, Warren, and Daviess County. This is for 2025 household income limits.

ADVERTISEMENT |EVO Mortgage is an Equal Housing Opportunity Lender NMLS # 1738461 (Nationwide Multistate Licensing System –

www.nmlsconsumeraccess.org) Terms, conditions, and restrictions may apply. All information contained herein is for informational purposes only and, while every effort is made to ensure accuracy, no guarantee is expressed or implied. Not a commitment to extend credit.

Borrower must meet all loan program and eligibility requirements. Information is subject to change without any notice. This is not an offer for an extension of credit or a commitment to lend. Restrictions may apply.

TERMS AND CONDITIONS: Eligibility for the $2,500 credit is based on qualifying income at or below 50% of the Area Median Income (AMI). This is determined via Fannie Mae’s and Freddie Mac’s respective tools. The credit must be applied toward down payment and/or closing costs for eligible 1-unit properties. It is also applicable for 2-4 unit properties with LTV ≤ 80%. The program applies to FNMA HomeReady® loans with closing dates between March 1, 2024, and February 28, 2025. It also applies to FHLMC Home Possible® loans within the same dates. All loans must be approved via DU or LPA

Annual Qualifying Income – The requirement for calculations to be included on the Income Calculation worksheet have been removed and should now be included on Attachment 9-B, the underwriter transmittal summary, FNMA form 1008/Freddie form 1077, or equivalent

4506-T – The requirement for asset statements to be reviewed to ensure borrowers have no additional income sources has been removed.

Repayment Income – MCC income must now be included in repayment income.

Boarder Income – USDA now considers a boarder as a household member and a boarder’s income must now be included in annual income calculation. Rent paid by boarders that is reported on tax returns must also be included in annual income.

Capital Gains – USDA removed requirement from Repayment Income to provide evidence showing borrowers own additional property or assets that may be sold if additional income is needed to support the mortgage obligation

Commission – The borrower must now show one year history in same or similar line of work to include commission in repayment income.

Fellowship, Stipend, Scholarship – Scholarship award letters must now provide date of termination and USDA will no longer presume benefits with no expiration date will continue. USDA also added guidelines for GI Bill income and stated it cannot be included in annual or repayment income.

MCC – This income must now be included in repayment income, but no history is required. A copy of the W-4 from employer is required to verify borrower is taking tax credit on monthly basis. Note: MCC’s are ineligible with FWL as qualifying income.

Unreimbursed Business Income – only taxable income is allowed to be included in repayment income

Section 8 – USDA removed requirement for section 8 income to be deducted from the monthly PITI to determine DTI if it is paid directly to the loan servicer when included in the repayment income.

Self Employed Income – Federal tax returns must now be reviewed to determine gross income for annual calculations. Removed requirement to deduct business loss before entering as repayment income into GUS or on loan application. Clarified documentation requirements as most recent 2 years of federal tax returns / transcripts & YTD P&L may be audited or unaudited

Social Security Income – clarified documentation options and will allow social security benefit statement or form SSA-1099/1042S to source

Temporary Leave – The history requirements for repayment income has been changed and now income must be received by loan closing.

Cash on Hand – The underwriter must review the reasonableness of accumulation based upon income stream, spending habits, etc. and cash on hand can no longer be included in reserves

Gift Funds – Clarification provided on how gift funds must be sourced when gift funds have been deposited into borrower’s account, not deposited into borrower’s account, or if funds are being wired directly to the settlement agent.

Large Deposits – USDA no longer addresses lump sum additions.

Section 504 Repair Loan and Grant Program for Kentucky USDA RHS Loans

If you missed the live webinar to learn about recent changes to the Section 504 Single-Family Housing Repair Loan and Grant Program, the presentation slides from the webinar are available on the U.S. Department of Agriculture (USDA) Rural Development’s website. This information is for individuals and organizations, including nonprofits and public agencies, who work with affordable housing products such as weatherization, home repairs, and Section 504 application packaging.

The slides will provide information on the following:

An overview of recent changes to the Section 504 Single-Family Housing Repair Loan and Grant Program.

For a brief overview of the 504 program, please watch the USDA Helps You Make Home Repairs

Program Guidelines & Terms –Section 504 Loans

• Maximum outstanding 504 loan amount is $20,000

• Interest rate is fixed at 1%

• Maximum term of 20 years (term and payment is based upon the

family budget)

• Appraisal and escrow account is required for loans over $15,000

• Flood insurance is required for properties located in a flood zone

• Mortgage, title work and closing agent required for loans of

$7,500 or more

• Mortgage is filed for loans of $7,500 and over

• Assets above $15,000 ($20,000 for elderly/disabled households)

must be applied toward repairs.

• Residential Mortgage Credit Reports are ordered by Agency for

loans of $7,500 and over (RMCR fee paid by Rural Development

General Eligibility Criteria – Section 504 Loans

• Household income must not exceed “very low” income

limits; < 50% HUD median income

• Applicant must own home (to include site when

considering manufactured housing) and occupy house on a

permanent basis

• Demonstrate repayment ability based upon a family budget

• Stable and dependable source of income

• Acceptable credit – reasonable ability and willingness to

meet debt obligations

• Meet asset limitations (15K non-elderly and $20K elderly*)

Program Guidelines & Terms –Section 504 Grant

• Maximum cumulative lifetime grant assistance is $7,500

• Grantee must sign Grant Agreement requiring occupancy

of home for 3 years

• No lien on property

• Repairs to remove health and safety hazards or to make the

home accessible and useable for household members with

disabilities.

General Eligibility Criteria – Section 504 Grants

• At least one applicant must be 62 years of age or older.

• Household income must not exceed “very low” income limits;

< 50% HUD median income

• Applicant must own home (to include site when considering

manufactured housing) and occupy house on a permanent basis

• Repairs must be necessary to remove health and safety hazards or

to make the home accessible and useable for household members

with disabilities.

• Must demonstrate a lack of repayment ability based upon a

household budget.

• Meet asset limitations (15K non-elderly and $20K elderly*)

• No outstanding federal judgments

SECTION 504 PROPERTY REQUIREMENTS

• Must be modest for the area; market value cannot be in

excess of USDA established area loan limit

• Property must be located in a designated rural area

• Must not have an in-ground swimming pool

• If the property has income producing land or structures, we

may use loan/grant funds as long as repairs are used for the

residential portion of the home.

• Mobile or manufactured homes must be on a permanent

foundation or be placed on a permanent foundation with

loan or grant funds.

For additional program Information, please visit the following USDA webpages:

COMPANY NMLS# 1738461

COMPANY NMLS# 1738461