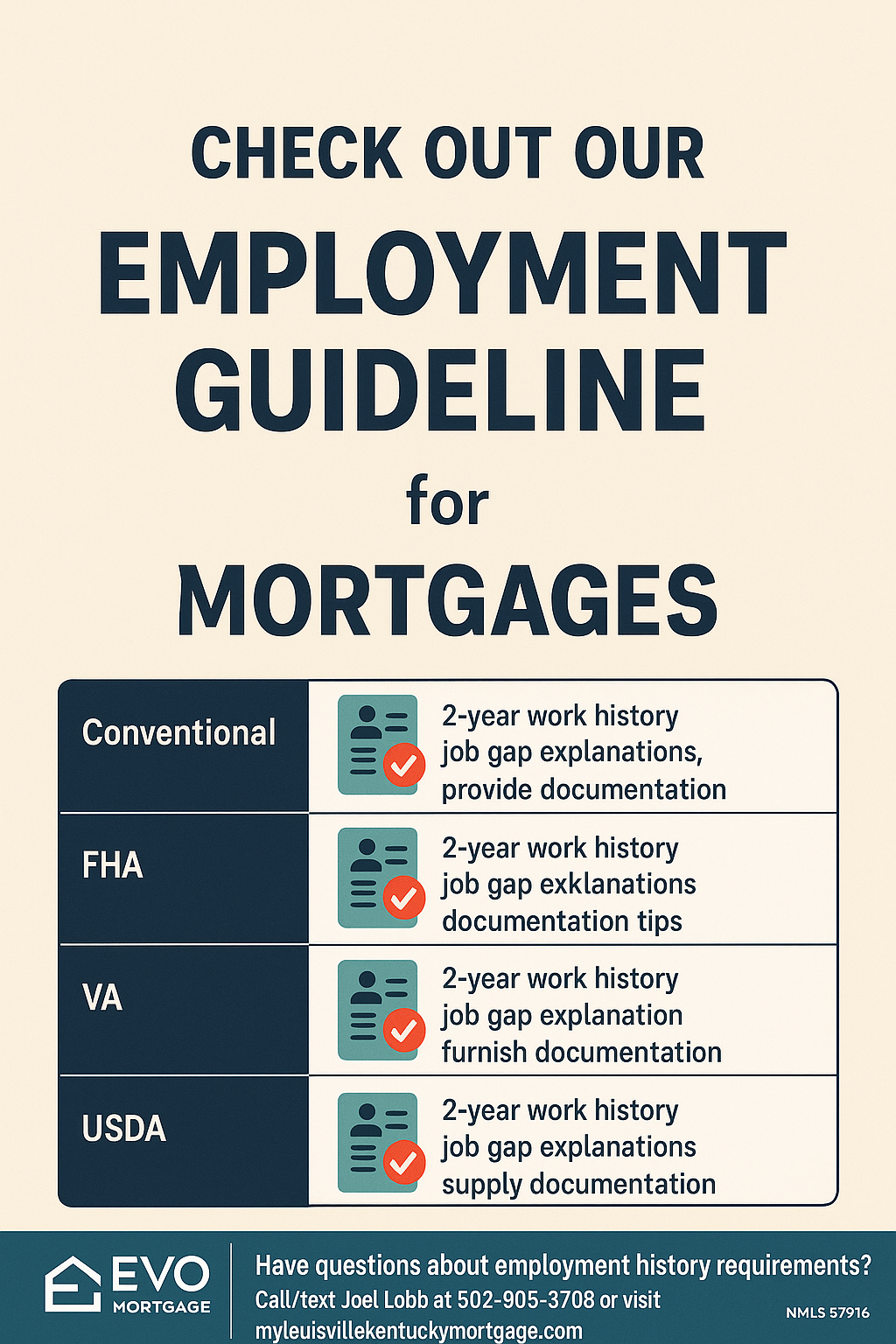

Employment History Requirements for FHA, VA, and USDA Loans in Kentuckyhttps://embed.reddit.com/widgets.js

byu/Any-Discount-5989 inMortgageQuestionsKY

I am a Kentucky based USDA Mortgage Lender that has originated over 300 KY Rural Housing Mortgage Loans in Kentucky-CALL OR TEXT 502-905-3708 FOR USDA MORTGAGE LOAN

Tag: Debt-to-income ratio

For potential home buyers with student loans that are either in a deferred payment status or being paid back through an income based or graduated repayment program, the treatment of this liability needs to be considered.

When student loan debts are not currently being paid upon, due to the loan applicant still being in school or recently graduating from school, the monthly liability will be calculated based on the lower of 1/2 of 1% of the outstanding loan balance or the monthly payment listed on the credit report.

Example if you owe $100,000 in student loan debt the monthly payment will be $500. Also, if the student loan is being paid upon, but at a lesser amount than originally agreed, such as the payment being determined based on repayment ability (i.e. Income Based Repayment Plan), the monthly payment will be calculated the same as above (monthly liability = 1/2 of 1% of the outstanding loan balance).

This offers a significant improvement compared to the FHA Loan guidelines, in which student loans that are in deferment or under an income based repayment plan will have the monthly payment calculated at 1% of the outstanding loan balance.

If the student loan is being paid upon as originally agreed upon when the loan was first obtained, the monthly liability will be the amount specified on the credit report.

Or if the student loans have been consolidated into a new loan, so long as the monthly payment is based on a fixed repayment schedule, that payment will be used when calculating the borrower’s debt to income ratio.

If you have yet to apply for your Kentucky USDA Loan pre-qualification request, you can do so online

Text/call: 502-905-3708

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

One of the most frequent questions that come from perspectives Kentucky home buyers is

Answering this question is determined based on calculating what are known as the borrower’s Debt-to-Income or DTI ratios. The established standard DTI ratio used for a USDA Loan is based on two sets of ratios, which are as follows:

A monthly mortgage payment includes the principal and interest payment on the mortgage note, as well as the monthly pro-rated portion of the annual fee, property tax and homeowner insurance premium.

Specific to the USDA Rural Loan program is the pro-rate portion of the USDA Annual Fee, which is often referred to as a monthly mortgage insurance payment. If there are any Condominium or Homeowner Association (HOA) fees, these fees must be included in the monthly mortgage payment as well.

Total debts include the anticipated monthly mortgage payment and all monthly re-occurring credit obligations.

Examples of reoccurring credit obligations include monthly car payments, minimum payment on credit cards, and student loan payments. If the borrower is obligated to make any alimony or child support payments, these payments will be included within the total debt calculations as well.

If the total debts exceed 41% of the gross monthly income, the maximum monthly mortgage payment must be reduced in order to bring total DTI back down to 41%. For example, assume a monthly income of $5,000.

Based on the 29%/41% ratio requirements, the maximum housing expense will be $1,450 and total debts will be $2,050. If the non-housing expense exceeds $600 ($2,050 – $1,450), the housing expense will need to be reduced by an equal amount to keep the total ratio at 41%.

While the 29%/41% ratio is considered to be the Underwriting standard guideline, the USDA Loan Program will allow for DTI ratios as high as 33.99%/45.99%.

What determines the ability to qualify at a higher ratio is a combination of factors, such as an approval through Guaranteed Underwriting System, which is USDA’s automated approval, and other compensating factors such as:

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com