The post Shutdown Stalling Rural Mortgages appeared first on Zillow Research.

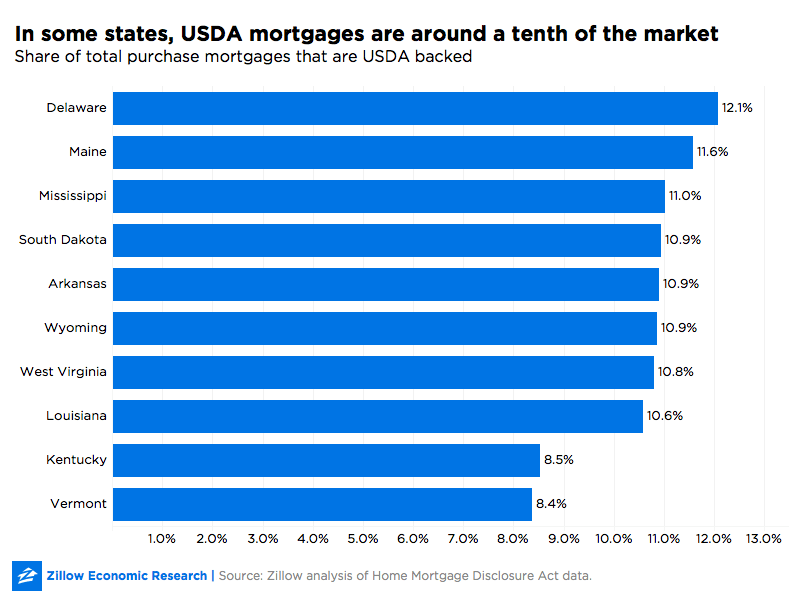

- The USDA backs about 120,000 mortgages a year, or about 3.5 percent of purchase mortgage originations nationally.

- Almost half of USDA mortgages were in southern states from 2012 to 2017.[1]

Borrowers who rely on mortgages from the U.S. Department of Agriculture (USDA) have been in a holding pattern that runs alongside the federal government shutdown. These loans from the USDA’s Farm Service Agency and the Rural Housing Service are made mostly in rural areas and often to low- and middle-income borrowers.

The USDA backs about 120,000 mortgages a year, or about 3.5 percent of all mortgage purchase originations,[2] according to data from the Home Mortgage Disclosure Act. The USDA offices that administer these loans have been closed since late December, rendering a major source of funding inaccessible.