- Annual Qualifying Income – The requirement for calculations to be included on the Income Calculation worksheet have been removed and should now be included on Attachment 9-B, the underwriter transmittal summary, FNMA form 1008/Freddie form 1077, or equivalent

- 4506-T – The requirement for asset statements to be reviewed to ensure borrowers have no additional income sources has been removed.

- Repayment Income – MCC income must now be included in repayment income.

- Boarder Income – USDA now considers a boarder as a household member and a boarder’s income must now be included in annual income calculation. Rent paid by boarders that is reported on tax returns must also be included in annual income.

- Capital Gains – USDA removed requirement from Repayment Income to provide evidence showing borrowers own additional property or assets that may be sold if additional income is needed to support the mortgage obligation

- Commission – The borrower must now show one year history in same or similar line of work to include commission in repayment income.

- Fellowship, Stipend, Scholarship – Scholarship award letters must now provide date of termination and USDA will no longer presume benefits with no expiration date will continue. USDA also added guidelines for GI Bill income and stated it cannot be included in annual or repayment income.

- MCC – This income must now be included in repayment income, but no history is required. A copy of the W-4 from employer is required to verify borrower is taking tax credit on monthly basis. Note: MCC’s are ineligible with FWL as qualifying income.

- Unreimbursed Business Income – only taxable income is allowed to be included in repayment income

- Section 8 – USDA removed requirement for section 8 income to be deducted from the monthly PITI to determine DTI if it is paid directly to the loan servicer when included in the repayment income.

- Self Employed Income – Federal tax returns must now be reviewed to determine gross income for annual calculations. Removed requirement to deduct business loss before entering as repayment income into GUS or on loan application. Clarified documentation requirements as most recent 2 years of federal tax returns / transcripts & YTD P&L may be audited or unaudited

- Social Security Income – clarified documentation options and will allow social security benefit statement or form SSA-1099/1042S to source

- Temporary Leave – The history requirements for repayment income has been changed and now income must be received by loan closing.

- Cash on Hand – The underwriter must review the reasonableness of accumulation based upon income stream, spending habits, etc. and cash on hand can no longer be included in reserves

- Gift Funds – Clarification provided on how gift funds must be sourced when gift funds have been deposited into borrower’s account, not deposited into borrower’s account, or if funds are being wired directly to the settlement agent.

- Large Deposits – USDA no longer addresses lump sum additions.

USDA Loans in Kentucky: The Ultimate Guide to 100% Financing

KENTUCKY USDA RURAL DEVELOPMENT HOME LOAN

HOME LOAN BASICS

- NO DOWN PAYMENT REQUIRED

- Closing costs can be financed into the loan

- Minimal credit score requirements – NO minimum score

- Low monthly mortgage insurance

- Home must be located in an eligible area

- Home must meet property eligibility requirements

- Fill out worksheet to get additional information about qualifying

- Must be a regular stick-built home

- Single Close Construction Program available

- USDA to USDA Streamline Refinances available

SFH Direct Loan and Grant Programs

February 7, 2022

Fee Increases for Origination Appraisals and Conditional Commitments

An Unnumbered Letter (UL) dated February 4, 2022, has been issued which increases the appraisal fee to $750 and the conditional commitment fee to $825 under the direct programs. The fee increases are effective March 6, 2022. The increased fees reflect market price increases for origination appraisals in rural areas and the average cost of appraisals under the programs’ nationwide contract with the Appraisal Management Companies.

Rural Development staff will follow the implementation responsibilities outlined in the UL, which has been posted to https://www.rd.usda.gov/resources/directives/unnumbered-letters under Housing Programs (or click here for a direct link).

How to qualify for a Kentucky FHA loan

FHA loans vs. conventional mortgages

CONVENTIONAL LOAN FHA LOAN

Credit score minimum 620 500

Down payment 3% to 20% 3.5% for credit scores of 580+; 10% for credit scores of 500-579

Loan terms 8- to 30-year terms 15- or 30-year terms

Mortgage insurance premiums PMI (if less than 20% down): 0.58% to 1.86% of loan amount Upfront premium: 1.75% of loan amount; annual premium: 0.45% to 1.05%

Interest type Fixed-rate or adjustable-rate Fixed-rate

Pros and cons of FHA loans

Pros

You can have a lower credit score: If you haven’t established much of a credit history or you’ve encountered some issues in the past with making on-time payments, a 620 credit score — the typical magic number for consideration of a conventional mortgage — might seem out of reach. If your credit score is 580, you’re in good standing with most FHA-approved lenders.

You can make a lower down payment: FHA loans also give the option for a smaller down payment. With a credit score of at least 580, you can make a down payment of as little as 3.5 percent. If your credit score is between 500 and 579, you may still be able to qualify for an FHA-backed loan, but you will need to make a 10 percent down payment.

You can stop renting earlier: Since FHA loans make buying a home easier, you can start building equity sooner. Instead of continuing to rent while trying to save more money or improve your credit score, FHA loans make the dream of being a homeowner possible sooner.

Cons

You won’t be able to avoid mortgage insurance: Since your credit score is lower, you’re a bigger risk of default. To protect the lender, you have to pay mortgage insurance. You can roll the upfront insurance premium into your closing costs, but your annual premiums will be divided into 12 installments and show up on every mortgage bill. If you put down less than 10 percent, you have to pay those annual premiums for the entire life of the loan. There’s no escaping them. That’s a big difference from conventional loans: Once you build up 20 percent equity, you no longer have to pay for private mortgage insurance.

You’ll have to meet property requirements: If you’re applying for an FHA loan, the property has to meet some eligibility requirements. The most important is the price: FHA-backed mortgages are not allowed to exceed certain amounts, which vary based on location. You have to live in the property, too. FHA loans for new purchases are not designed for second homes or investment properties.

You could pay more: When you compare mortgage rates between FHA and conventional loans, you might notice the interest rates on FHA loans are lower. The APR, though, is the better comparison point because it represents the total cost of borrowing. On FHA loans, the APR can sometimes be higher than conventional loans.

Some sellers might shy away: In the ultra-competitive pandemic housing market, sellers weighing multiple offers often viewed FHA borrowers less favorably.

Louisville Kentucky Mortgage Loans

—

| CONVENTIONAL LOAN | FHA LOAN | |

|---|---|---|

| Credit score minimum | 620 | 500 |

| Down payment | 3% to 20% | 3.5% for credit scores of 580+; 10% for credit scores of 500-579 |

| Loan terms | 8- to 30-year terms | 15- or 30-year terms |

| Mortgage insurance premiums | PMI (if less than 20% down): 0.58% to 1.86% of loan amount | Upfront premium: 1.75% of loan amount; annual premium: 0.45% to 1.05% |

| Interest type | Fixed-rate or adjustable-rate | Fixed-rate |

Pros and cons of FHA loans

Pros

- You can have a lower credit score: If you haven’t established much of a credit history or you’ve encountered some issues in the past with making on-time payments, a 620 credit score — the typical magic number for consideration of a conventional mortgage — might seem out of reach. If your credit score is 580, you’re in good standing with most FHA-approved lenders.

- You can make a lower down…

View original post 410 more words

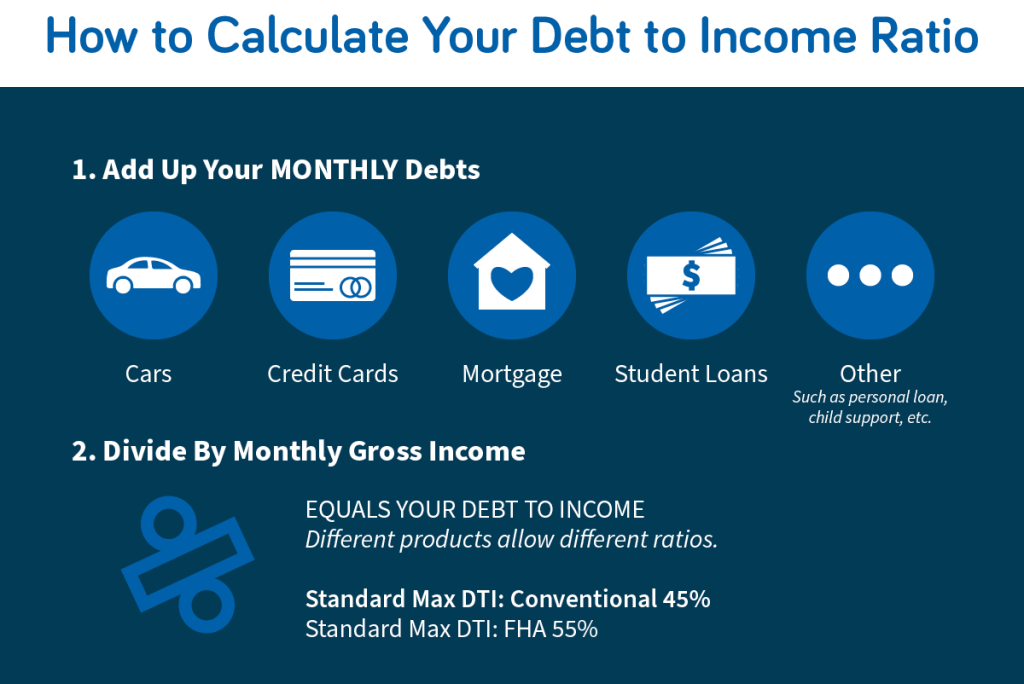

Debt-to-Income Ratio for Kentucky Mortgage Loans

Debt-to-Income Ratio for Kentucky Mortgage Loans

No Money Down Kentucky USDA Rural Loan Program

How USDA Government Underwriters calculate your Debt-to-Income or DTI ratio.

One of the most frequent questions that come from perspectives Kentucky home buyers is

“How Much House Can I Afford?”

Answering this question is determined based on calculating what are known as the borrower’s Debt-to-Income or DTI ratios. The established standard DTI ratio used for a USDA Loan is based on two sets of ratios, which are as follows:

- Front-end or housing ratio – the monthly mortgage payment cannot exceed 29% of the gross monthly income.

- Back-end or total debt ratio – the total debts, including the new monthly mortgage payment, cannot exceed 41% of the gross monthly income.

A monthly mortgage payment includes the principal and interest payment on the mortgage note, as well as the monthly pro-rated portion of the annual fee, property tax and homeowner insurance premium.

Specific to the USDA Rural Loan program is the pro-rate portion of the USDA Annual Fee, which is often referred to as a monthly mortgage insurance payment. If there are any Condominium or Homeowner Association (HOA) fees, these fees must be included in the monthly mortgage payment as well.

Total debts include the anticipated monthly mortgage payment and all monthly re-occurring credit obligations.

Examples of reoccurring credit obligations include monthly car payments, minimum payment on credit cards, and student loan payments. If the borrower is obligated to make any alimony or child support payments, these payments will be included within the total debt calculations as well.

If the total debts exceed 41% of the gross monthly income, the maximum monthly mortgage payment must be reduced in order to bring total DTI back down to 41%. For example, assume a monthly income of $5,000.

Based on the 29%/41% ratio requirements, the maximum housing expense will be $1,450 and total debts will be $2,050. If the non-housing expense exceeds $600 ($2,050 – $1,450), the housing expense will need to be reduced by an equal amount to keep the total ratio at 41%.

While the 29%/41% ratio is considered to be the Underwriting standard guideline, the USDA Loan Program will allow for DTI ratios as high as 33.99%/45.99%.

What determines the ability to qualify at a higher ratio is a combination of factors, such as an approval through Guaranteed Underwriting System, which is USDA’s automated approval, and other compensating factors such as:

- 680 or higher credit score

- No or low “payment shock” – less than a 100% increase in proposed mortgage payment vs. current rental housing expenses

- Fiscally sound use of credit

- Ability to accumulate savings

- Stable employment history with 2 or more years in current position or continuous employment history with no job gaps

- Cash reserves available for use after settlement

- Career advancement as indicated by job training or additional education in the applicant’s profession

- Trailing spouse income – as a result of a job transfer, in which the house is being purchased, prior to the secondary wage-earner obtaining employment. This assumes that the secondary wage-earner has an established history of employment and has a reasonable chance to obtain new employment in the area upon relocating to the area

- Low total debt load

Joel Lobb (NMLS#57916)

Senior Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle Suite 3

Louisville, KY 40223Company ID #1364 | MB73346

Text/call 502-905-3708

kentuckyloan@gmail.com