USDA Loans in Kentucky. Updated Qualifying Guidelines

What is Kentucky USDA Rural Development Guarantee?

Kentucky USDA Rural Development Guarantee USDA loans offer 100% financing options on home purchases in rural areas of Kentucky. Properties though can be located within city limits and in subdivisions depending on the population density of that particular County of Kentucky. Jefferson and Fayette Counties, the two largest counties of Kentucky are not eligible for Rural Development Loans.

Full Credit Guidelines below ….click on link for USDA Mortgage Credit Guidelines

👇

Some highlights of the KY Rural Housing loan program are:

- 100% financing on purchases with no down payment

- Low 30 year fixed rates. No prepayment penalty.

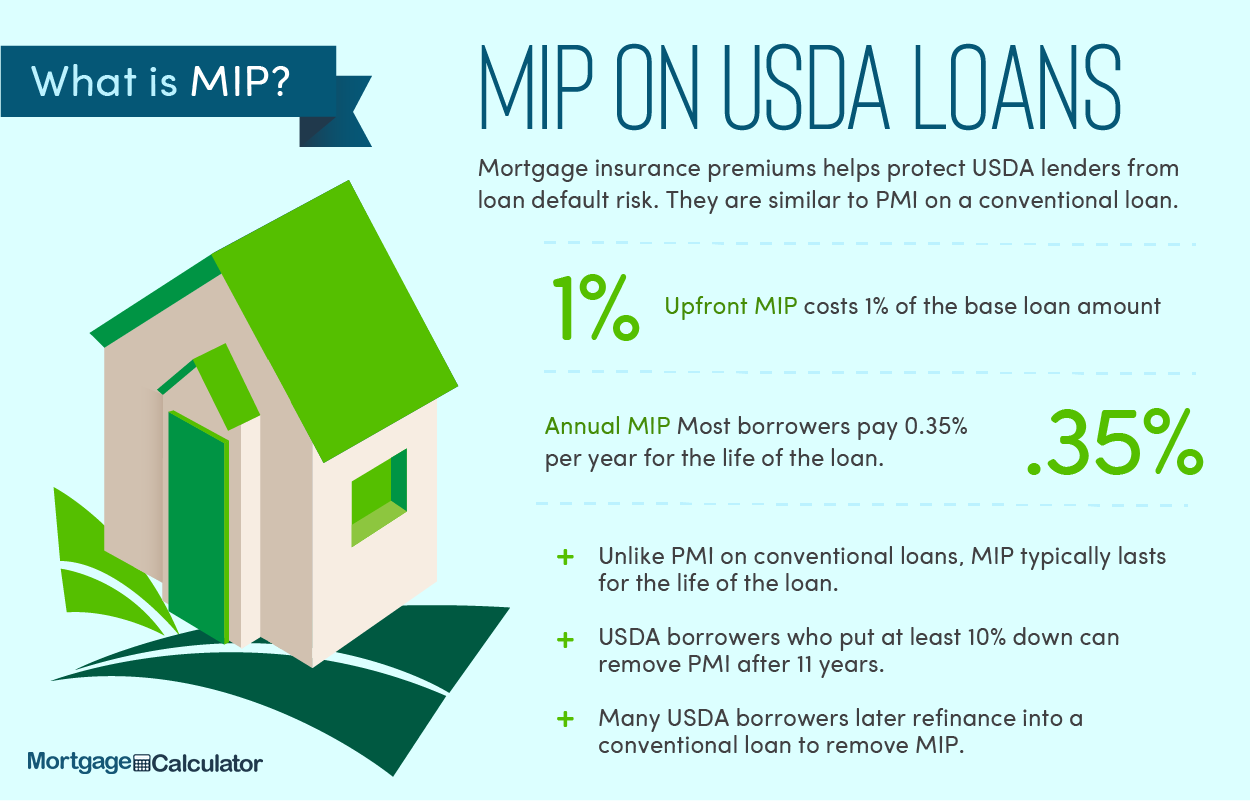

- Rural Housing monthly guarantee fee of .35%

- Upfront Rural Housing funding fee of 1% of the loan amount and is financed into new loan

- No Minimum credit scores but helpful to have 620 or higher with most USDA lenders with a 640 and get an automated underwriting approval thru Rural Housing’s underwriting engine – GUS-GUS Stands for the automated Underwriting system they use online to pre-approve you for a loan.

- Each lender will set their own credit and debt to income criteria

- No rental verification needed with GUS approval

- No foreclosures in the last 36 months,

- A bankruptcy discharged at least 36 months

For a USDA eligible areas in Kentucky, see the property and income eligibility search, please click HERE.

Things to look for in your Rural Housing property search in Kentucky below:

- Avoid homes in flood zones – RD is very restrictive for homes in flood zones. They will do them in flood zones just watch out for the costly premiums.

- Avoid homes with cisterns – they are extremely difficult to get financed

- Be aware that homes with wells and septic systems needed extra tests for contamination

- Avoid homes with any income-producing activities such as working farms, detached buildings with offices or car lifts for auto repairs, or anything else related to income-producing activities.

- Manufactured homes and doublewides are allowed, new or used. Since May 5, 2025, USDA finances existing manufactured homes in Kentucky as long as the unit was built within 20 years of your closing date, sits on a permanent foundation, has never been installed at another homesite, is at least 400 square feet, and still carries both the HUD certification label and the HUD data plate, with no alterations made after it left the factory other than an engineered porch or deck. A lot of lenders still refuse these loans, but that is their own overlay, not a USDA rule. We do originate them at EVO Mortgage.

- Must meet FHA standards on appraisals so watch out for this on older homes with crawl spaces.

- Must have a permanent heat source and no wood stoves as permanent heat sources

- Homes that are in need of major repairs.

Put my experience of originating KY USDA loans to work for you. I have successfully originated over 200 Rural Housing Mortgage Loans in Kentucky. I offer free pre-approvals and will help you from start to finish and I usually attend all my closings in Kentucky.

Get Qualified for a Kentucky USDA Loan Now!

Mortgage Loan Officer

Text or call: 502-905-3708

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916, (www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice.