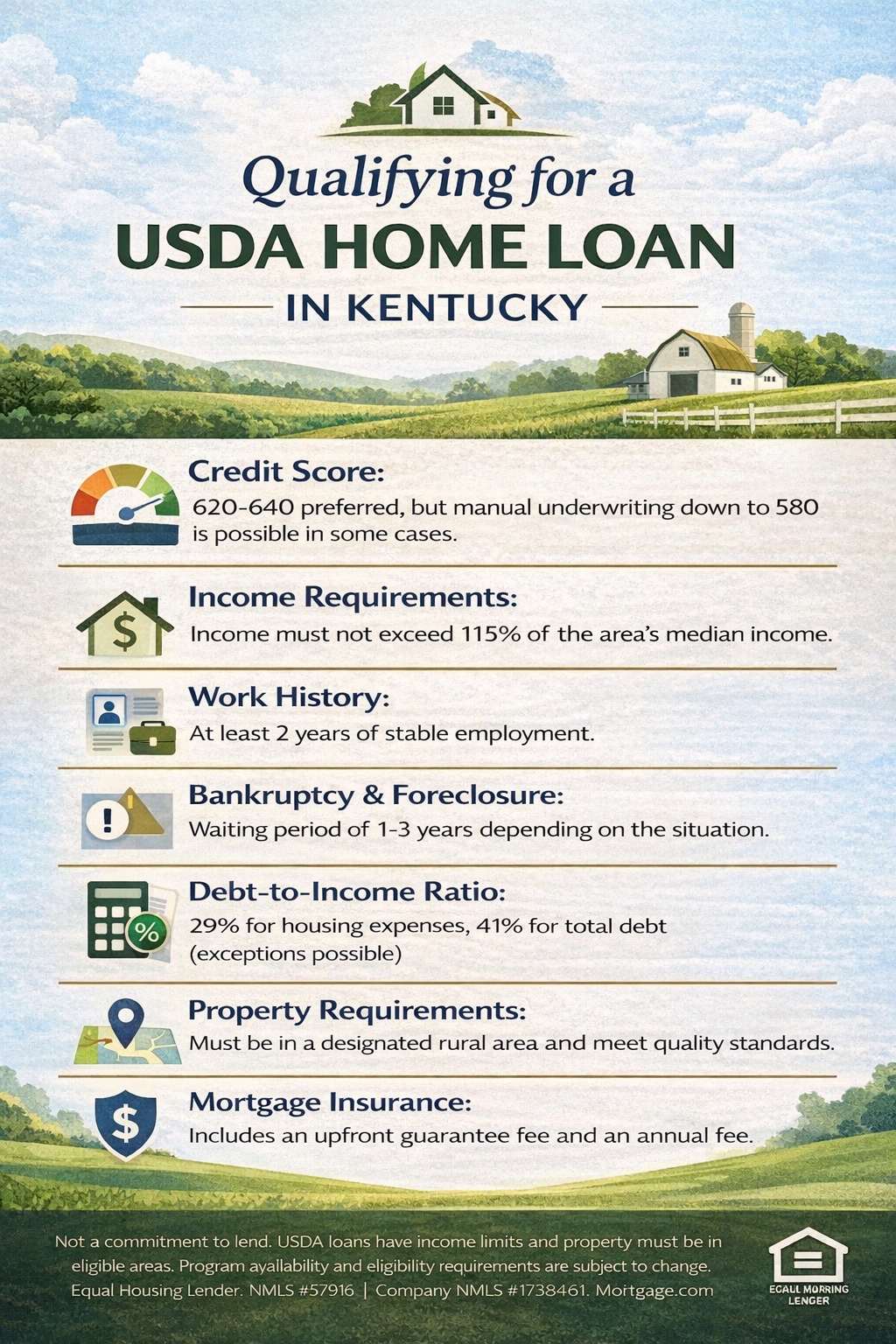

Kentucky USDA Loan Guide

Kentucky USDA Appraisals: What to Expect (and What Can Trigger Repairs)

USDA appraisals follow FHA minimum property standards to confirm value and ensure the home is safe, sound, and move-in ready.

Key point

The USDA appraisal is completed by an FHA-approved appraiser and must follow FHA property requirements. The report typically includes language substantially similar to:

“The subject meets minimum standards as set under guidelines established by the U.S. Department of Housing and Urban Development and indicated in Handbook 4000.1.”

How the USDA appraisal works

- Appraiser inspects the property and determines market value.

- If the home has property deficiencies, the appraisal is issued “subject to” repairs.

- Repairs are completed and the appraiser performs a re-inspection.

- Appraiser signs off once repairs meet minimum standards.

Common property deficiencies that can delay closing

- Chipped or peeling paint

- Missing handrails on stairs or guardrails on decks

- Non-working lights, exposed wiring, or uncovered junction boxes

- Inoperable HVAC, plumbing leaks, or non-working water heater

- Utilities not turned on at time of appraisal (water/electric/heat)

Bottom line: USDA is designed for homes in move-in condition, not fixer-uppers.

What FHA/USDA appraisers typically review

General health and safety

- Foundation or structural defects

- Working utilities: water, sewer/septic, heat, electricity

- Paint hazards (especially pre-1978 peeling paint)

- Incomplete renovations

- Water damage or moisture concerns

- Access for vehicles/emergency access

- External hazards and excessive noise

- Missing handrails/guardrails

Exterior

- Roof condition and leaks

- Damaged siding or holes

- Doors that don’t open/close properly

- Gutters, chimney, porches, stairs, railings

- Fencing issues that create safety concerns

- Swimming pool safety/code (if applicable)

Interior and systems

- Each room has working electricity

- Bedroom egress (window or exterior door)

- Kitchen: typical conveyed appliances and working sink

- Bathrooms: working fixtures and ventilation

- Crawlspace/basement: moisture or standing water

- Heating and plumbing: operable with no major leaks

Repair escrow note (important)

A limited repair escrow option may be available through select USDA lenders. If you think repairs may be required, tell me before you write the offer so we can align the lender strategy up front and avoid avoidable delays.

Appraisal vs home inspection

An FHA/USDA appraisal is not a full home inspection. Buyers should still obtain an independent home inspection to evaluate overall condition, components, and long-term maintenance risks.

As with all loan programs, the USDA Loan requires that an independent appraiser inspect the subject property in order to determine the property value. Specific to a USDA Loan, the appraisal report will be conducted by an FHA approved appraiser. The appraisal report must include verbiage or similar verbiage:

“The subject meets minimum standards as set under guidelines established by the U.S. Department of Housing and Urban Development and indicated in Handbooks 4000.1”

No different from a FHA or VA appraisal inspection, the appraiser is required to document all property deficiencies that preclude the appraiser from signing off on their report. A property deficiency is any defect to the house that the appraiser deems necessary to have repaired to ensure compliance to the loan program guidelines. Typical examples of property deficiencies include:

- Chipped and peeling paint

- Missing handrails on stairs and railing on decks

- Lights not working properly and wires hanging out of the electrical box

- Non-working heating and cooling systems and plumbing

- Houses that do not have utilities turned on

If a property has deficiencies, the appraiser will determine the value of the property, but state that their report is subject to the property defects listed being corrected. After the property defects are repaired, the appraiser will re-inspect the property, and signoff if the required repairs have been completed.

Bottom line, the USDA Loan program is designed to finance homes that are in move-in condition, not fixer-uppers. However, on a subsequent email I will review an option to establish a repair escrow account to address certain property deficiencies. The repair escrow account is only available through one of my many USDA lenders, so it is imperative to inform me when making an offer a house if this option will be required.

Kentucky USDA appraisals

Kentucky USDA appraisals can take home buyers by surprise. That’s why we’ve put together some good-to-know info about the process. Feel free to use this to help educate your clients.

The property must pass an FHA appraisal, so USDA and FHA have the same appraisal requirements, which determines the current market value and makes sure the house meets certain safety standards. Here is a list of items an FHA appraiser may look for:

General Health and Safety

- Foundation or structural defects

- Whether the utilities (water, sewage, heat, and electricity) all work

- Chipped or peeling paint in homes built before 1978

- Incomplete renovations

- Water damage

- If the property is accessible to vehicles, especially emergency vehicles

- Exposed wiring and uncovered junction boxes

- Whether the house is too close to outside hazards, such as a leaking oil tank or a waste dump

- Excessive noise, such as being close to an airport

- Missing handrails

Exterior

- Leaky or defective roof and holes in the siding

- Leaning or broken fencing

- Doors that don’t properly open or close

- Condition of gutters, chimney, stairs, railings, and porches

- If swimming pools are up to code

Every Room

- Whether each room has electricity

- Whether each room has a window or door to the exterior to be used as a fire escape

Kitchen

- Missing or broken appliances usually sold with a home, including stove and refrigerator

- Broken or leaking sink

Bathrooms

- Broken or leaking toilet, sink, or tub/shower

- No ventilation (either an exhaust fan or window)

Crawl space or basement

- Basement moisture

- Evidence of past or present standing water

Heating and Plumbing

- Inoperable HVAC

- Major plumbing issues and leaks

These are some common items an FHA appraiser looks for, but other issues that might make a house unsafe could keep it from passing. An FHA appraisal is not the same as an independent home inspection. It’s still a good idea to get a separate home inspection to make sure you’re making a wise investment!

.jpg "USDA APPRAISAL REQUIREMENTS FOR KENTUCKY MORTGAGE LOANS")

Call/Text:

Call/Text:  Email:

Email:  Website:

Website:

Address: 911 Barret Ave, Louisville, KY 40204

Address: 911 Barret Ave, Louisville, KY 40204