RHS Increase in Annual Fee for Rural Housing Mortgage Loans in Kentucky

Kentucky USDA Mortgage Lenders must underwrite the loan using an annual fee of .5 percent and resubmit the application to RD in GUS after October 1, 2014

On Wednesday, October 1, 2014, the annual fee for both purchase and refinance loans will increase from .4 percent to .5 percent. The Guaranteed Underwriting System (GUS) has been updated to allow lenders to select and underwrite at either the .4 percent or .5 percent annual fee structure. Lenders should communicate with Rural Development (RD) offices to understand current processing time-frames.

GUS “Final Submissions” with an annual fee of .4 percent, that areissued a conditional commitment by RD prior to the close of business on Tuesday, September 30, 2014, will not be affected by the annual fee change. Those submissions that are not issued a conditional commitment by RD prior to the close of business on Tuesday, September 30, will be affected by the annual fee change.

Lenders must underwrite the loan using an annual fee of .5 percent and resubmit the application to RD in GUS.

Looking for a home loan when you are self-employed can be a bit challenging but a USDA loan may be a great option. Many banks and lenders shy away from this type of loan due to the complex nature and experience that it requires. These scenarios can be complicated but with proper analysis and documentation the outcome can be successful. This short video will explain how to qualify for a USDA home loan if you are self-employed.

Who are considered self-employed when applying for a USDA loan?

• 1099 Contractors are considered self-employed

• W2 Employees who are 100% commissioned

• Converting from a self-employed to a W2 employee can be acceptable

What are the USDA guidelines for the self-employed?

Minimum guidelines require that a self-employed borrower must have 2 years of self-employment history. Common documents that will be needed for verification purposes include articles of incorporation when applicable and at least 2 years of both business and personal tax returns. Also, keep in mind your tax returns should include all pages and schedules. If you filed an extension, make sure to have the signed extension available for underwriting.

Tax return documentation includes but not limited to:

• Business tax returns for corporations

• Schedule C for sole proprietors

• Partnership details if applicable

• Signed extensions when necessary

• Year to Date Profit & Loss Statement

• Year to Date Balance Sheet

What are the USDA home loan income limits for the self-employed?

As with all USDA home loans, income limits will apply and qualifying income for a USDA home loan for the self-employed is based on your adjusted income. The adjusted income is calculated after expenses are deducted. Your qualifying income is not based on gross commissions or your total sales. When following USDA guidelines for self-employment, alternative income documentation such as bank statements showing deposits are not acceptable. Read more about the USDA eligibility requirements for the self-employed.

We realize that qualifying when you are self-employed may seem overwhelming, but we offer the unique experience and expertise to help with each step of the process.

What are the Kentucky USDA Mortgage Loan Requirements?

To decide if you qualify for an USDA Mortgage Loan, we will look at:

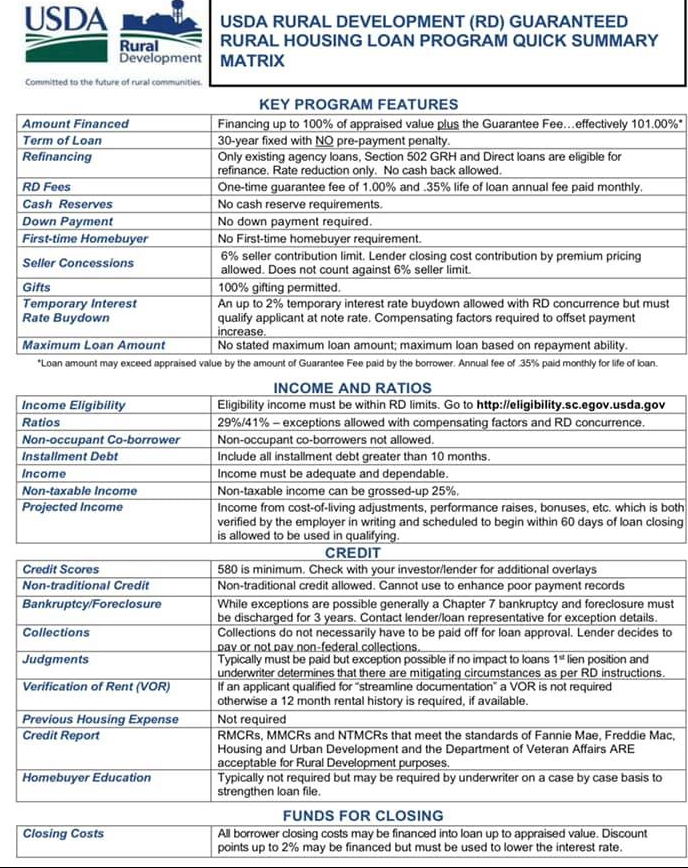

Your income and your monthly expenses. Standarddebt-to-income ratios are 29/41 for USDA Loans on a manual underwrite. Those ratios can be waived up to 32/44 when every applicant on the loan has a 680 or higher credit score and the file has a compensating factor.

Your credit history (this is important, but USDA’s credit standards are flexible). USDA does not publish a minimum credit score anywhere in Handbook HB-1-3555. What drives your file is the underwriting recommendation you get back from GUS, USDA’s automated system. A 640 middle score will usually get a GUS Accept. Below 640 the file has to be manually underwritten, which is still possible. Most lenders hold you to a 640 floor, but that is the lender’s own overlay, not a USDA rule.

Your overall pattern rather than to individual problems you may have had.

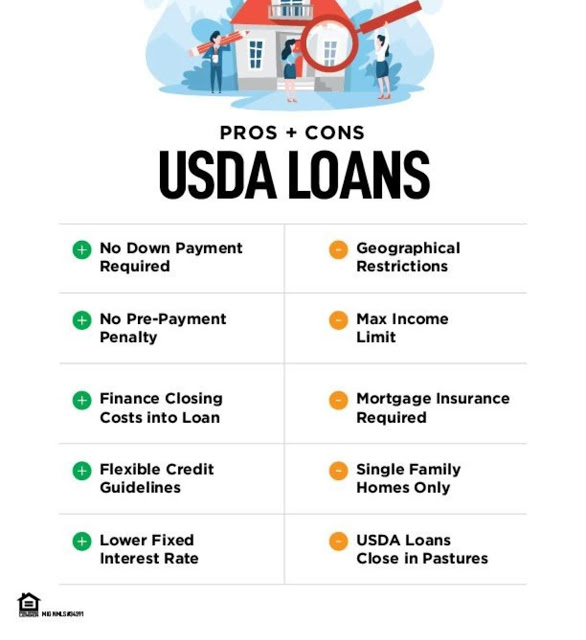

To be eligible for an Kentucky USDA Mortgage, your monthly housing costs (mortgage principal and interest, property taxes and insurance) must meet a specified percentage of your gross monthly income (29% ratio). Your credit background will be fairly considered. There is no USDA minimum FICO credit score — the GUS underwriting recommendation is what drives the approval, and a 640 middle score typically returns a GUS Accept. You must also have enough income to pay your housing costs plus all additional monthly debt (41% ratio). These percentages may be exceeded with compensating factors. Applicants for loans may have an income of up to 115% of the median income for the area. Effective July 13, 2026, the income limits in most Kentucky counties are $122,800 for a 1-4 person household and $162,100 for a 5-8 person household. In Boone, Bracken, Campbell, Gallatin, Kenton and Pendleton counties the limits are $128,600 and $169,800. Families must be without adequate housing, but be able to afford the mortgage payments, including taxes and insurance.

Can I get an USDA Mortgage Loan after bankruptcy?

Criteria for USDA loan approvals state that if you have been discharged from a Chapter 7 bankruptcy for 36 months or more, you are eligible to apply for an USDA mortgage. If you are in a Chapter 13 bankruptcy, have made all court approved payments on time and as agreed for at least 12 months, and your trustee gives permission, you are also eligible to make an Kentuck USDA Loan application. A foreclosure, deed-in-lieu, or short sale carries a 36 month waiting period.

What are the USDA Down Payment Requirements? USDA Mortgages have no down payment requirement. Other loan programs don’t allow this.

What types of property are eligible?

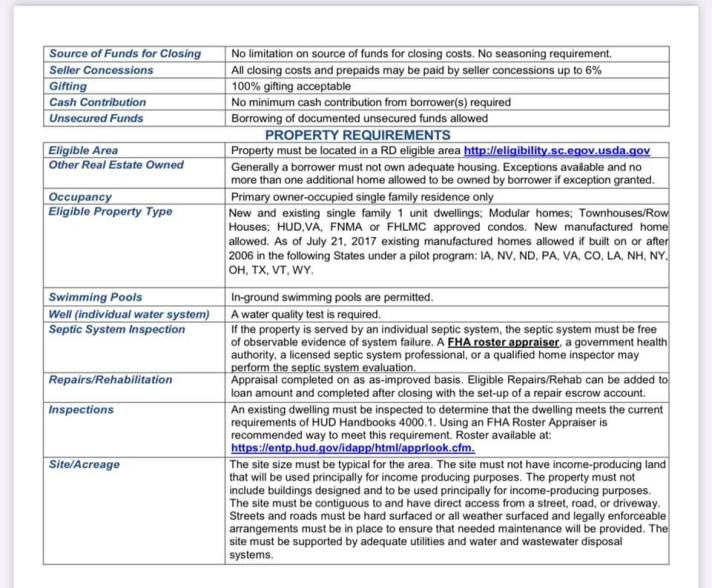

While USDA Mortgage Guidelines do require that the property be Owner Occupied (OO), they do allow you to purchase condos, planned unit developments, manufactured homes, and single family residences.

What is the maximum amount that I can borrow?

The maximum amount for an Kentucky USDA Mortgage Loans are determined by:

Maximum loan amount: The is no set maximum loan amount allowed for an USDA Mortgage. Instead, your debt-to-income ratios will dictate how much home your can afford (29/41 ratios). Additionally, your total household monthly income must be within USDA allowed maximum income limits for your area. Maximum USDA Loan income limits for your area can be found at here.

Maximum financing: The maximum USDA Mortgage amount will be 100% of the appraised value of the home.

What kinds of loans does USDA offer?

Fixed rate loans – All Rural Housing and USDA loans are fixed-rate mortgages. In a fixed rate mortgage, your interest rate stays the same during the whole loan period, normally 30 years. The advantage of a fixed-rate mortgage is that you always know exactly how much your monthly payment will be, and you can plan for it.

What is Considered a Rural Area by the USDA?

Rural areas include open country and places with population of 10,000 or less and—under certain conditions—towns and cities. There is an automated rural area eligibility calculator at:http://eligibility.sc.egov.usda.gov.

Kentucky USDA Loans

What are USDA Home Loans?

USDA stands for United States Department of Agriculture. A USDA Mortgage provides a low-cost insured home mortgage loan that suits a variety of options. A USDA mortgage is likely the best home loan option if you want to purchase a home with no down payment. If you’re unsure about your credit rating, or have concerns about a down payment when you’re doing a home loan comparison,

What Types of Loans does USDA offer in Kentucky?

Currently, there are two kinds of USDA Homeo Loans available in Kentucky for single family households:

USDA Guaranteed Rural Housing Loans

USDA Guaranteed Kentucky USDA Mortgage are the most common type of USDA loanin Kentucky and allow for higher income limits and 100% financing for home purchases. USDA Guaranteed Loan applicants may have an income of up to 115% of the median household income for the area. Area income limits for this program can be viewed here. All USDA Guaranteed Loans carry 30 year terms and are set at a fixed rate.

USDA Direct Rural Housing Loans

USDA Direct Housing Loans are less common than USDA Guaranteed Loans and are only available for low and very low income households to obtain homeownership, as defined by the USDA. Very low income is defined as below 50 percent of the area median income (AMI); low income is between 50 and 80 percent of AMI; moderate income is 80 to 100 percent of AMI. Click here to see area income limits for this program.

What factors determine if I am eligible for a USDA Loan in Kentucky?

To be eligible for A USDA Kentucky USDA Mortgage Loans | Rural Housing Ky Loans in Kentucky, your monthly housing costs (mortgage principal and interest, property taxes, and insurance) must meet a specified percentage of your gross monthly income (29% ratio). Your credit background will be fairly considered. USDA itself sets no minimum FICO credit score for a Kentucky USDA Mortgage Loans | Rural Housing Ky Loans approval. The GUS underwriting recommendation drives the file, and most lenders apply their own 640 overlay on top of it. You must also have enough income to pay your housing costs plus all additional monthly debt (41% ratio). These ratios can be exceeded somewhat with compensating factors. Applicants for loans may have an income of up to 115% of the median income for the area. Maximum USDA Guaranteed Loan income limits for your area can be found at here. Maximum USDA Direct Loan income limits for your area can be found at here. Families must be without adequate housing, but be able to afford the mortgage payments, including taxes and insurance.

What is the maximum amount that I can borrow?

The maximum amount for an USDA home loan is determined by:

Maximum Loan Amount: The is no set maximum loan amount allowed for USDA Kentucky USDA Mortgage Loans | Rural Housing Ky Loans. Instead, your debt-to-income ratios will dictate how much home your can afford (29/41 ratios). Additionally, your total household monthly income must be within USDA allowed maximum income limits for your area. Maximum USDA Guaranteed Loan income limits for your area can be found at here.

Maximum financing: The maximum USDA Kentucky USDA Mortgageamount is 101% of the appraised value of the home (100% plus the 1.00% USDA Kentucky USDA Mortgage RD Loan upfront guarantee fee).

How much money will I need for the down payment and closing costs?

USDA Kentucky USDA Mortgage Loans require no down payment and they allow for the closing costs to be included in the loan amount (appraisal permitting).

What property types are allowed for USDA Rural Loan Mortgages?

While USDA mortgage guidelines do require that the property be Owner Occupied (OO), they do allow you to purchase condos, planned unit developments, manufactured homes, and single family residences.

Additional offers from other lenders.

This website is not an Government Agency, and does not officially represent the HUD, VA, USDA or FHA

Kentucky USDA Loan Adjusted Maximum Income Limits by County\\\\\\\\\

Kentucky USDA Mortgage Loans | Rural Housing Ky Loans

Why choose a USDA Mortgage?

The loans require no down payment.

There are no prepayment penalties for USDA Kentucky USDA Mortgage Rural Home Loans

A USDA Kentucky USDA Mortgage Rural Housing loan has no monthly mortgage insurance the way FHA and conventional loans do. What you pay instead is a 0.35% annual fee on the loan balance, spread out monthly, plus a 1.00% upfront guarantee fee you can roll into the loan.

A USDA Kentucky USDA Mortgage Rural Housing is available all rural areas of the country, provided a market exists for the property and the home meets HUD’s minimum property standards.

A USDA Kentucky USDA Mortgage Rural Housing Loan can be used to purchase a new or existing one family home in rural areas.

USDA RD LOANS are offered at terms of 30 years with a fixed interest rate.

USDA Loan FAQ’s

Kentucky USDA Mortgage Loans | Rural Housing Ky Loans

What is the Maximum LTV for a USDA Loan?

The maximum USDA rural loan LTV can be up to 100% LTV plus the Agency guarantee fee.

Can Closing Costs be Financed into the Loan?

Yes, any difference between the contract price and the appraisal value can be used to finance normal closing costs for a Kentucky USDA Mortgage

What is a USDA Loan Guarantee?

USDA Rural Development Single Family Housing Program serves as a safety net for mortgage lenders. The USDA provides the full faith and assurance of the U.S. government that any financial loss resulting from servicing the loan will be reimbursed in full up to an amount not exceeding 90% of the original loan amount. All loss up to an amount not exceeding 35% of the original loan is fully reimbursed. Any loss amount exceeding the 35% is 85% reimbursed. This leaves the lender only 15% exposed on the loss amount above the 35% of original loan. In the majority of cases, the total loss does not exceed 35% of the original loan and the lenders are fully reimbursed. This guarantee provides lenders an expanded level of protection against losses. The quality of this guarantee allows lenders to easily sell the loans on the secondary market.

Kentucky USDA Mortgage Loans | Rural Housing Ky Loans