How to Get a Free Credit Score for Mortgage Loan Approval

Before applying for a Kentucky mortgage loan, make sure you understand the difference between a free consumer credit score and the mortgage credit scores lenders actually use.

Key Takeaway

The credit score you see on Credit Karma, a credit card app, or a consumer credit monitoring site may not be the same score used for a mortgage approval. Most mortgage lenders review mortgage-specific credit scores when determining eligibility for FHA, VA, USDA, KHC, and conventional home loans.

3 Ways to Check Your Credit Before Applying for a Mortgage

1. Pull Your Free Credit Reports

Start by reviewing your free credit reports at AnnualCreditReport.com. Look for late payments, collections, incorrect balances, duplicate accounts, old addresses, and accounts that do not belong to you.

Remember: your free credit report usually does not include your actual mortgage credit score.

2. Use myFICO for Mortgage FICO Scores

myFICO offers access to multiple FICO score versions, including mortgage-related score models. This is usually not free, but it can help consumers see scores closer to what a mortgage lender may review.

3. Contact a Mortgage Lender or Broker

A mortgage lender or mortgage broker can pull a mortgage credit report as part of the pre-approval process.

At my office, there is no upfront out-of-pocket cost for the credit report. If your loan closes with us, the credit report fee may be collected at closing and shown on your settlement statement.

Important: Not All Credit Scores Are the Same

Free credit score apps may show VantageScore or newer consumer FICO models. Those scores can be helpful for general credit monitoring, but they may not match the mortgage middle score used for loan approval.

Example: you may see a 680 score on a free credit app, but your actual mortgage middle score could be different.

Common Mortgage Credit Score Guidelines

Loan Program

Common Minimum Score Guideline

FHA Loan

580+ for 3.5% down

VA Loan

No official VA minimum, but many lenders require 580–620+

USDA Loan

Often 620–640+ depending on lender and automated approval

Conventional Loan

Often 620+

KHC Down Payment Assistance

Usually tied to the first mortgage program and lender approval

Want to Know Your Real Mortgage Credit Score?

If you are buying a home in Kentucky, I can help review your mortgage credit profile and explain your options for FHA, VA, USDA, KHC, and conventional mortgage programs.

Joel Lobb

Mortgage Loan Officer

NMLS #57916

EVO Mortgage | Company NMLS #1738461

911 Barret Ave., Louisville, KY 40204

Equal Housing Lender. This is not a commitment to lend. All loans are subject to credit approval, income verification, property approval, and program guidelines. Not affiliated with FHA, VA, USDA, KHC, Fannie Mae, Freddie Mac, or any government agency.

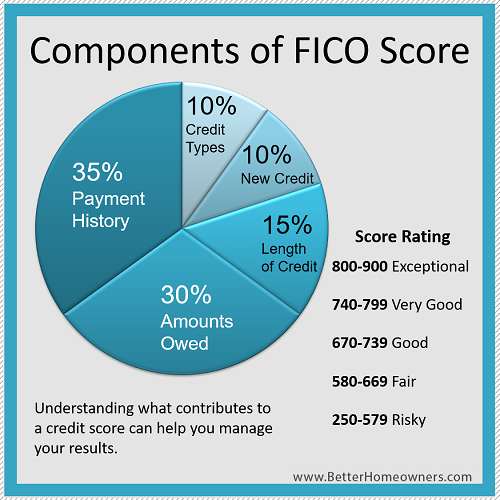

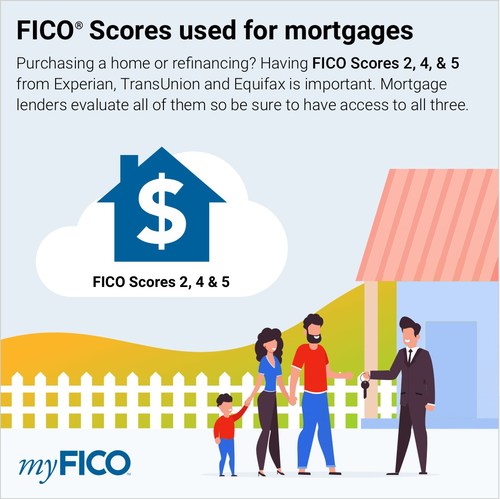

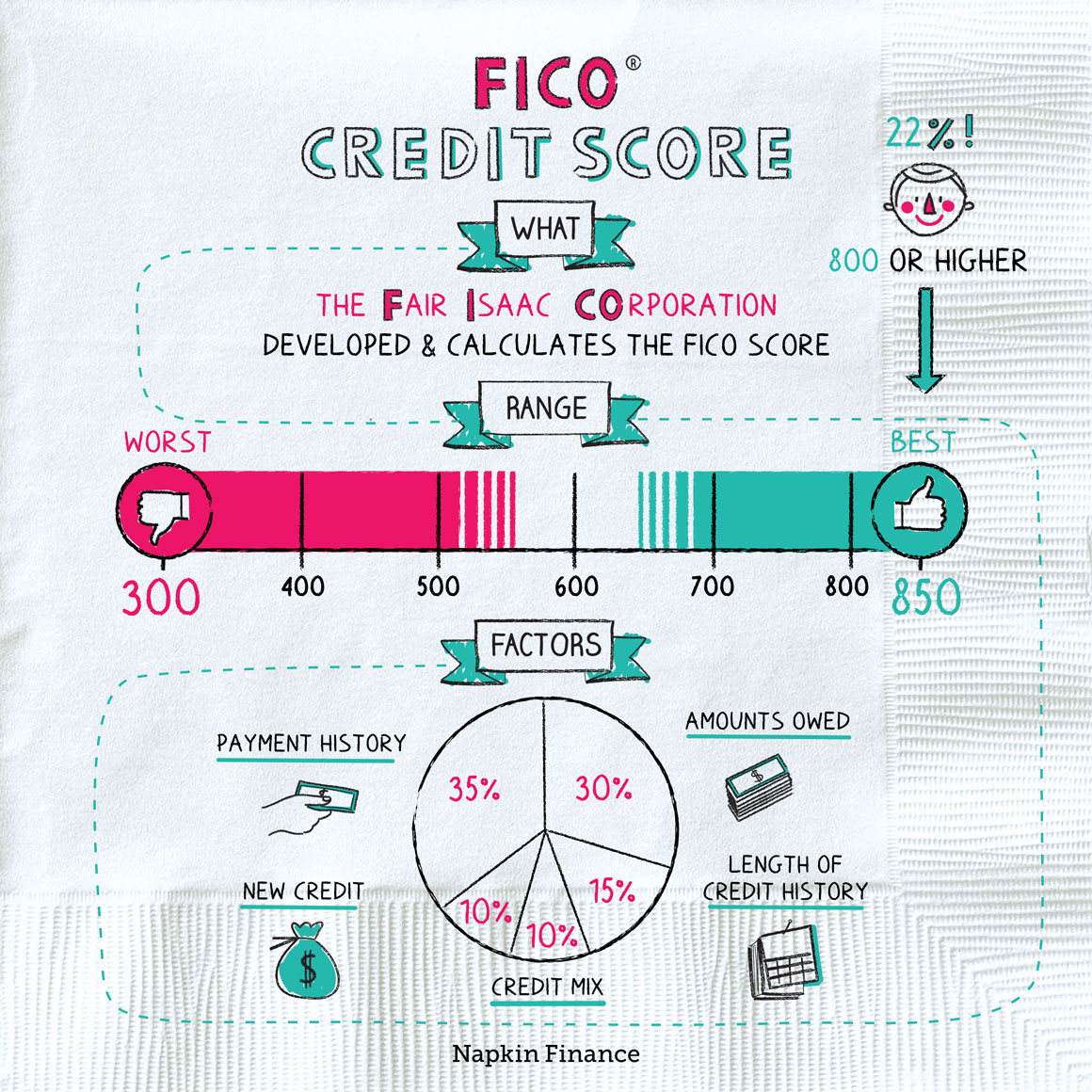

When you are ready to apply for a Kentucky mortgage loan approval to buy a house in the state of Kentucky, you will need a more accurate picture of how a mortgage lender may view your Transunion, Experian, Equifax credit reports and their scores. Scores go from 344 to 850 on each three credit bureaus and they take the middle score of the three, throwing out the highest and lowest score. Kentucky Mortgage lenders look at your credit on Equifax as well as TransUnion and Experian — all 3 bureaus.

Although FICO Score version 8 is one of the latest and most predictive versions of the FICO Score, the mortgage industry generally uses the “classic” versions 5, 4 and 2 from Transunion, Equifax and Experian

If you are planning to buy a home in Kentucky, one of the first questions you should be asking is: what credit score do I need to qualify? The second question is: what credit score do I need to get the best interest rate? These are not the same question. Qualifying is one thing. Securing optimal pricing is another.

Kentucky minimum credit score requirements by loan type

Credit score alone does not determine approval. Underwriting also evaluates income stability, debt-to-income ratio, assets, employment history, and the appraisal. That said, credit score is still a critical approval gate for most programs.

FHA loan (Federal Housing Administration)

Minimum allowed by HUD: 580 for 3.5% down; 500–579 typically requires 10% down

Real-world lender requirement in Kentucky: most lenders will not go below 580; many prefer 600–620

VA loan (Veterans Affairs)

VA does not publish a minimum credit score

Real-world lender overlays: most lenders require 580–620; stronger pricing typically starts at 640+

USDA Rural Development (guaranteed)

Technically, 580 may be accepted in some cases

In practice, 640+ is commonly needed for smoother automated approval; under 640 may trigger manual underwriting

Conventional (Fannie Mae)

620 minimum

Best pricing is typically 740–760+

KHC (Kentucky Housing Corporation) with down payment assistance

620 minimum

No exceptions for most KHC DPA options

Bottom line: most realistic Kentucky approval scenarios begin at 580 for FHA/VA and 620 for Conventional/KHC. USDA is often most efficient at 640+.

Government guidelines vs lender overlays

Programs like FHA, VA, USDA, Fannie Mae, and KHC publish baseline guidelines. Lenders often add overlays (stricter rules) due to risk and secondary market requirements. This is why “on paper” minimums may not match what lenders actually approve.

How lenders calculate your qualifying credit score

Mortgage lenders pull a tri-merge credit report showing three scores from Equifax, Experian, and TransUnion. The lender discards the highest and lowest score and uses the middle score.

Example:

Equifax: 610

Experian: 629

TransUnion: 614

Your qualifying score would be 614 (the middle score).

Most lenders require at least two usable scores. Also, the score you see on consumer apps is often not the same score model used for mortgage underwriting.

What credit score typically gets the best interest rate?

Rate pricing improves as scores rise. While exact pricing varies by day, lender, and loan type, these tiers are common:

620–639: higher rates and limited pricing

640–679: improved options

680–719: strong approval tier

720–759: excellent pricing

760+: top tier pricing

If you are within 10–20 points of a better tier, improving your score before you lock can materially reduce your payment and long-term interest cost.

If your credit score is low: what to do next

Do not guess. Do not apply randomly. Also, do not dispute accounts without a plan (disputes can delay underwriting). The most effective approach is a structured credit review focused on:

reducing revolving utilization

verifying tradeline reporting accuracy

strategic payoff sequencing if needed

avoiding new inquiries and new debt

In many cases, meaningful improvement can happen in 30–60 days with the right steps.

Images from the original post

Replace the image URLs below with your WordPress Media Library URLs (or paste your existing image blocks here).

Credit score tiers for Kentucky mortgage approvalsTri-merge credit report: how the middle score is usedHow credit score ranges can affect mortgage pricing

Frequently asked questions

What is the minimum credit score to buy a home in Kentucky?

Many lenders will consider FHA/VA at 580+ and Conventional/KHC at 620+. USDA is commonly easiest at 640+ for automated approval, though exceptions may exist depending on the full file.

Does VA have a minimum credit score requirement?

VA does not publish a minimum credit score. However, most lenders use overlays and commonly require 580–620.

Why is my Credit Karma score different than my mortgage score?

Mortgage lending uses specific FICO score models. Many consumer apps show different scoring models intended for education and monitoring, not mortgage underwriting.

How do lenders pick which credit score they use?

With three bureau scores, lenders typically use the middle score (not the highest or the lowest). Most lenders also require at least two usable scores.

What score gets the best mortgage rate?

Top pricing is commonly seen at 760+ and often strong pricing begins around 740+. Exact pricing depends on the loan type, down payment, DTI, reserves, and market conditions.

The views and opinions stated on this website belong solely to the author and are intended for informational purposes only.

Posted information does not guarantee approval and does not represent full underwriting guidelines.

This does not represent being part of a government agency.

The views expressed do not necessarily reflect the view of my employer.

Not all products or services mentioned may fit all borrowers.

NMLS ID #57916 (www.nmlsconsumeraccess.org). USDA mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender.

Products and interest rates are subject to change without notice.

{

“@context”: “https://schema.org”,

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “What is the minimum credit score to buy a home in Kentucky?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Many lenders will consider FHA/VA at 580+ and Conventional/KHC at 620+. USDA is commonly easiest at 640+ for automated approval, though exceptions may exist depending on the full file.”

}

},

{

“@type”: “Question”,

“name”: “Does VA have a minimum credit score requirement?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “VA does not publish a minimum credit score. However, most lenders use overlays and commonly require 580–620.”

}

},

{

“@type”: “Question”,

“name”: “Why is my Credit Karma score different than my mortgage score?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Mortgage lending uses specific FICO score models. Many consumer apps show different scoring models intended for education and monitoring, not mortgage underwriting.”

}

},

{

“@type”: “Question”,

“name”: “How do lenders pick which credit score they use?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “With three bureau scores, lenders typically use the middle score (not the highest or the lowest). Most lenders also require at least two usable scores.”

}

},

{

“@type”: “Question”,

“name”: “What score gets the best mortgage rate?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Top pricing is commonly seen at 760+ and often strong pricing begins around 740+. Exact pricing depends on the loan type, down payment, DTI, reserves, and market conditions.”

}

}

]

}

{

“@context”: “https://schema.org”,

“@type”: “MortgageLoan”,

“name”: “Kentucky Mortgage Loan Options: FHA, VA, USDA, Conventional, KHC”,

“description”: “Educational overview of credit score requirements and typical lender overlays for Kentucky mortgage loans, including FHA, VA, USDA, Conventional (Fannie Mae), and KHC down payment assistance options.”,

“loanType”: [“FHA”, “VA”, “USDA”, “Conventional”, “KHC”],

“areaServed”: {

“@type”: “State”,

“name”: “Kentucky”

},

“provider”: {

“@type”: “MortgageBroker”,

“name”: “Joel Lobb, Mortgage Broker FHA, VA, KHC, USDA”,

“telephone”: “+1-502-905-3708”,

“email”: “kentuckyloan@gmail.com”,

“url”: “http://mylouisvillekentuckymortgage.com/”,

“identifier”: {

“@type”: “PropertyValue”,

“name”: “NMLS”,

“value”: “57916”

}

},

“isBasedOn”: “Credit score guidance varies by program and lender overlays. Final approval depends on full underwriting including income, assets, DTI, and appraisal.”,

“disclaimer”: “Informational only. Not a commitment to lend. All loans subject to credit approval, verification, and collateral evaluation. Rates and programs subject to change.”

}

GUS Approved: Each credit report must contain 2 acceptable tradelines with at least 12 month history and last active within the last 24 months (see below regarding acceptable tradelines).

Manual Underwrite: As determined acceptable by the underwriter.

· Court-ordered payments should be documented by a copy of the court order.

· Borrower(s) must have an acceptable existing repayment plan for any arrearages and proof of 12 months on time payments, and/or be required to pay account in full prior to, or at closing.

· If the borrower is a co-signer on an account paid by a 3rd party, the liability may only be excluded from the borrower debt ratios if evidence the primary obligor has been making the payments on time on the debt for a minimum of 12 months can be obtained.

· Court-ordered assignment of debt should be documented by a copy of the court order. Must have 12 months cancelled checks from the payer of the court ordered debt in order to exclude from the debt ratio.

PREVIOUS MORTGAGE:

· Section 1980.345(c)(1)(ii) requires all previous mortgage liabilities disposed of through a sale, trade, or transfer without a release of liability, to be included in the debt ratio calculation unless evidence can be obtained to confirm the remaining party has made payments over the last 12 months.

· In divorce settlements when one person retains ownership of a residence as a result of the proceedings, it does not imply that the person relinquishing ownership is automatically released of the financial liability associated with an existing mortgage debt. The divorce decree along with a release of liability from the mortgage creditor must be presented as evidence that an applicant is no longer legally responsible for the mortgage payment. If no release of liability is granted by the creditor then the applicant remains legally obligated for the debt. Quit claim deeds do not remove liability for mortgage debts.

DEFERRED INSTALLMENT DEBT

May not be omitted from debt ratio. If the credit report does not reflect a monthly payment due at the end of the deferment period, the lender may request a copy of the applicant’s payment letter, or utilize the industry standard of estimating student loan payments as 1% of the loan balance.

NON-REIMBURSED EMPLOYEE EXPENSES

If the borrower claims any non-reimbursed employee expenses (IRS Form 2106 or 1040 Schedule A), the borrowers monthly income should be reduced by the annualized monthly average.

BUSINESS DEBT IN BORROWER’S NAME

When the account in question does not have a history of delinquency, the debt may be excluded with satisfactory evidence the obligation was paid out of company funds (such as 12 months cancelled company checks). If the account in question has a history of delinquency, the full debt obligation must be included in the borrower’s debt ratio.

FINANCED PROPERTIES

Additional financed properties are generally not permitted as borrower may not own any other suitable housing at time of closing.

DEBTS WITH <6 REMAINING PAYMENTS

The total debt ratio should include revolving debt regardless of when the debt will be retired. Installment loans will only be considered if the debt will be retired in more than six months. However, if the monthly payment on the debt is substantial, the payment will also be included in long term debt. The GUS system will automatically exclude debt that is eligible to be excluded. If not excluded by GUS the debt must be included in the debt ratio.

“PAYING DOWN” ACCOUNTS

Not permitted. Settlement offers will not be considered as proof of balance

SETTLEMENT OFFERS

Are acceptable on accounts that will be paid in full at closing as long as the offer is in writing from the creditor reporting on the credit report.

PAST DUE ACCOUNTS (NOT A COLLECTION OR CHARGE OFF)

Recent derogatory credit >1×30 within the previous 12 months is not permitted unless approved by GUS. All past due accounts must be current at time of closing.

COLLECTIONS/ CHARGE OFFS

· No accounts converted to Collection/Charge off in previous 12 months allowed, unless approved by GUS.

GUS Approved:

· Medical Collections/Charge offs are not required to be paid.

· Other Collections/Charge offs, if >24 months, not required to be paid, otherwise accounts must be paid in full prior to, or at, closing.

Manual Underwrite:

· Medical Collections/Charge offs are not required to be paid.

· Other Collections/Charge offs must be paid in full prior to, or at closing.

Any unpaid Collections/Charge offs will require a satisfactory letter of explanation from the borrower.

OUTSTANDING FEDERALLY INSURED OR GUARANTEED DEBT

Borrower(s) must have an acceptable existing repayment plan (minimum of 12 months), and/or be required to pay account in full prior to, or at closing. Borrower must also be cleared through CAIVRS.

JUDGMENTS/LIENS

· Must be paid at, or prior to, closing.

· Borrower(s) may not have any new Judgments/Liens within the previous 12 months, unless approved by GUS.

BANKRUPTCY (ALL)

3 years seasoning required from Discharge or Dismissal date.

FORECLOSURE

3 years seasoning required.

DEED-IN-LIEU OF FORECLOSURE

3 years seasoning required.

SHORT SALES

3 years seasoning required.

COMPENSATING FACTORS

Some compensating factors include:

· Conservative use of credit

· Minimal increase in borrower’s housing expense

· Substantial cash reserves after closing

· Credit score >660

· Low total debt ratio (does not compensate for high housing ratio)

MULTIPLE RISK LAYERING

Multiple risk layering is not allowed on manually underwritten loans:

· Payment Shock (>100%)

· Ratio Waiver

· Credit Waiver

· Credit Score <660

· Short Duration of Employment (less than 12 months employment with current employer)

Joel Lobb (NMLS#57916) Senior Loan Officer

502-905-3708 cell

502-813-2795 fax jlobb@keyfinllc.comKey Financial Mortgage Co. (NMLS #1800)*

107 South Hurstbourne Parkway*

Louisville, KY 40222*