Key reminders for income calculations:

• Look at the date of employment, date the recent pay stub pays through, and the VOE.

• Look for overtime, bonus, commission, or any additional income that should be counted and count it.

• Make sure you are calculating your days correctly when averaging the income.

• If there has been a recent increase in salary or hourly rate, use the higher salary or hourly rate when calculating the Annual Household Income.

• #1 Reminder: Document your process. USDA reviewers look for Underwriter notes and any sort of explanation. It helps them to review a file faster if they don’t have to recreate what has already been done.

Q. The applicant has a history of overtime, with a substantial amount received year to date; however, the VOE states the overtime is unlikely to continue. Do I need to include overtime in the annual income calculation?

A. Annual income is calculated based on what is expected to be received in the ensuing 12 months. If there is a history of overtime, it would need to be considered by the underwriter when calculating annual

income. Ultimately it is the approved lender’s responsibility to review the complete income history to determine what is expected to be received in the ensuing 12 months and to document the permanent loan file

to support their lending decisions.

Q. Does the IRS child tax credit need to be included in the annual income calculation?

A. No, tax credits, including the Child Tax Credit are not included in the Annual income calculation.

Q. Is per diem considered in annual income calculations?

A. If the per diem is taxable income, then it must be included in annual income. If the per diem is non-taxable income, it is considered reimbursement and therefore not included in annual income.

Q. The VOE states the applicant is expected to receive a 3% pay raise within the next 3 months. Do we have to count this expected increase in annual income?

A. Annual income is calculated based on what is expected to be received in the ensuing 12 months, including bonus income, projected pay raises, etc. If a pay raise is expected within the next 12 months, it would need to be included in the annual income calculation.

Q. We have a borrower that is divorced and has joint custody of a child that is only claimed on the tax returns as a dependent every other tax year. Can we consider this child a household member for the calculation of family size and income eligibility?

A. Applicants with shared custody may include their children as household members and receive the $480 per

child deduction.

Annual household income for Kentucky USDA Loans

All files must include an income calculation worksheet. Lenders may document their income calculations on their own in-house income worksheet

Defines Annual Income as: Income from all household members who live or propose to live in the dwelling as their primary residence for all or part of the ensuing 12 months. Adjusted annual income is used to determine whether an applicant is income-eligible for a guaranteed loan, or interest assistance, if applicable.

Adjusted annual income provides for deductions to account for varying household circumstances and expenses.

Kentucky USDA loans are loans offered by the United States Department of Agriculture to those looking to buy homes in rural areas of Kentucky.

There are a few requirements and restrictions associated with this type of loan however, if you are afirst time home buyer in Kentucky with a limited income, no down payment and are looking to live in a rural part of Kentucky, this may be a good option for you to purchase a home going no money down and getting a 30 year fixed rate loan.

Income Requirements for USDA Loans in Kentucky

The Rural Housing USDA website provides an income eligibility calculatordepending on where you are looking for housing in the state of Kentucky. Because it is a nationally funded loan by the United States Government, the income restrictions will vary county-by-county but the loan recipient cannot make more than 115% of the median income for the area in which they are applying. There is also a chart you can consult that provides Kentucky USDA county income limits depending on the number of people in your home. Most Kentucky Counties will allow up to $90,200 for a household family of four or less, and up to $119,350 for a household of five. The Northern Kentucky Counties of Kenton, Bracken, Boone, Gallatin, Campbell allow for more. See Chart below

Households with 1-4 members have different limits as households with 5-8. Similarly, applicants living in high-cost counties will have a higher income limit than those living in counties with a more average cost of living.

Kentucky Score Requirements for a USDA Loan in Kentucky

Borrowers in Kentucky are required to have a FICO minimum credit score of 581 or higher. However, most USDA lenders will create a credit overlay where they will want a minimum credit score of 640 in order to get a GUS approval.

If the potential borrower has declared bankruptcy or foreclosure within the last 36 months, they would be ineligible for this type of loan.

If the mortgage was included in the Bankruptcy, sometimes the 36 month hold is ignored and you just have to make sure the property is out of your name before applying for a USDA loan

Can you get a USDA loan in Kentucky with a Previous Bankruptcy?

Chapter 7 bankruptcy, the bankruptcy must have been discharged at least 3 years prior to becoming eligible for a Kentucky USDA home loan.

Borrowers must be in a Chapter 13 bankruptcy for a minimum of 12 months, with documentation of 12 months of on time payments and a letter of authorization from the bankruptcy trustee authorizing you to enter into new debt.

In order to qualify for a USDA home loan after filing a Chapter 13 bankruptcy, additional documentation may be requested/required stating that the reason for the Chapter 13 filing was due to extenuating circumstances beyond the borrower’s control, temporary in nature and not likely to re-occur.

Home must be primary Residence.

Recipients must be U.S. Citizens, U.S. non-citizen nationals or Qualified Aliens to apply for this program. They must also agree to use the home as their primary residence and not as a rental property.

The property must be for a family including townhouses, single family homes, condominiums (FHA Approved), new construction or new mobile homes.

What areas of Kentucky Qualify for the USDA Loan Program?

The USDA provides a map of the where you can apply a USDA loans are eligible in Kentucky. The major metro areas of Jefferson County and Fayette County Kentucky are not eligible for Rural Housing Loans in Kentucky, along with some parts of Northern Kentucky next to Cincinnati; parts of Owensboro, Paducah, Bowling Green, Richmond, Frankfort, Winchester, Radcliff, Hopkinsville and Henderson Kentucky are not eligible.

If you have a property in mind, you can head over to the eligibility map to see if the home you are considering qualifies.

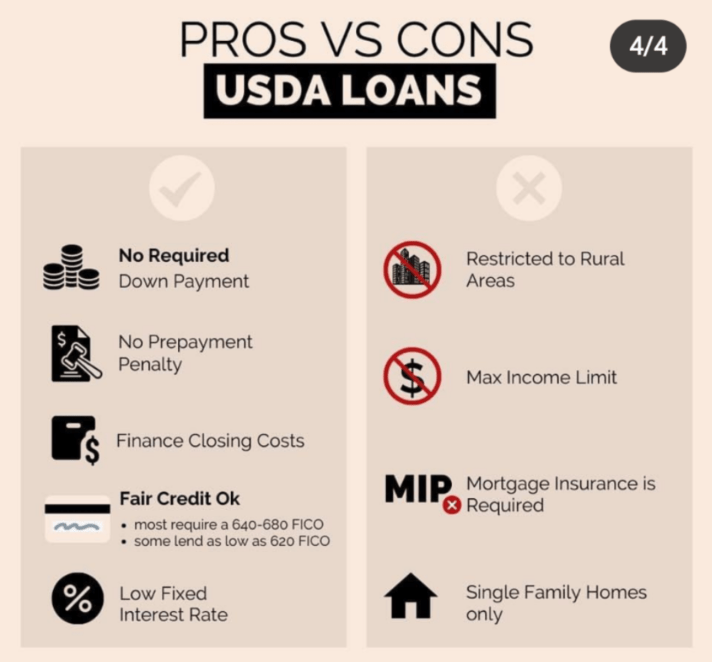

What are the advantages of USDA loans in Kentucky?

For many people in a low to middle-income bracket, saving for a down payment can be difficult. A USDA loan does not require the purchaser to put any money down toward the purchase price of a home. The government insures the loan in this case, should the borrower default, therefore the borrower is required to carry mortgage insurance during the life of the loan. The mortgage insurance for the USDA loan is provided at a more discounted rate than that required by traditional loans.

On USDA loans the mortgage insurance is 1% upfront, called a guarantee fee, and .35% monthly called an annual mortgage insurance fee to USDA. The beauty of USDA, is that it does not matter if you have a credit score of 640, or a credit score of 740, everyone pays the same premiums, unlike conventional loans.

They only offer 30 year fixed rates with no prepayment penalty, and usually the rates are very low and compare to FHA rates and much lower than conventional loans.

USDA loans take on average about 30 days to close, and the appraisal must meet FHA requirements. Home inspections are not required, and only new mobile homes are allowed on this home loan program.

If you are an individual with disabilities who needs accommodation, or you are having difficulty using our website to apply for a loan, please contact us at 502-905-3708.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916 http://www.nmlsconsumeraccess.org/

— Some products and services may not be available in all states. Credit and collateral are subject to approval. Terms and conditions apply. This is not a commitment to lend. Programs, rates, terms and conditions are subject to change without notice. The content in this marketing advertisement has not been approved, reviewed, sponsored or endorsed by any department or government agency. Rates are subject to change and are subject to borrower(s) qualification.

Beginning on September 23rd, 2019, the way USDA calculates student loans in regards to Student Loans and they effect loan approvals.

Kentucky Rural Housing loan Changes for Student Loans

Effective immediately for all Kentucky Rural Development loans, student loan calculations will be changed to the following

Fixed Payment Loans:A permanent amortized, fixed payment may be used when it can be documented that the payment is fixed, the interest rate is fixed, and the repayment term is fixed.

Non-Fixed Payment Loans (i.e. deferred, income based, graduated, adjustable, etc.): The payment should be calculated as the greater of 0.5% of the loan balance or the actual payment reflected on the credit report. No additional documentation is required.

RHS temporarily modified the calculation of non-fixed student loan payments for purposes of determining debt-to-income ratios. Per the modified requirements, lenders must now use the higher of .50% of the loan balance or the actual payment reflected on the credit report as the monthly payment (rather than 1% of the loan balance). The modified requirements went into effect September 23, 2019 and will be permanently incorporated into Chapter 11 of the Single Family Housing Loan Program Technical Handbook (HB-1-3555) in the near future.

BIG change announced for Kentucky Rural Housing USDA loans today regarding how minimum payments on your Student Loans are calculated. Reach out to see if you qualify for this awesome loan!

Have you or someone you know been turned down for a USDA loan recently because of student loans?

New guidelines effective today may allow you to qualify (or qualify for a little higher loan amount)

**This is not an offer for extension of credit or a commitment to lend. All loans must satisfy company underwriting guidelines. Information and pricing are subject to change at any time and without notice. Not all applicants will qualify for all loan products offered. This is not an offer to enter into a rate lock agreement under any applicable law. Not endorsed or part of USDA Federal Government Agency.

A borrower who has no verifiable employment for 6 months or longer is deemed to have a gap in employment.

Any gaps in employment must be analyzed in order to make a final determination of stable and dependable income. An employment gap does not automatically render an applicant ineligible. Applicants with job gaps due to maternity leave, medical leave, relocation, etc. are considered to have employment continuity. Applicants returning to the workforce after leaving a previous job to care for a child/family member, complete education, etc. will require a 12 month employment history.

A Kentucky USDA home loan is a zero-dollar-down mortgage option provided by USDA’s Department of Rural Development.

This government-backed loan program comes in two types: direct loan, which is reserved for lower-income households and issued by USDA, and the guaranteed loan, which is reserved for low- to moderate-income families. The guaranteed loan is funded by private lenders, and USDA guarantees a portion of the loan against default.

The KY USDA home loan program is generally more beneficial to rural families than a conventional lending program, particularly for first-time homebuyers with lower- to median-level incomes.

Some of the benefits of Kentucky Rural Housing USDA loans include: • zero down payment • competitive interest rates • lower-than-average monthly mortgage insurance • relaxed credit requirements versus conventional loans

• no loan limits

How do I determine eligibility for a Kentucky Rural Housing USDA loan? To be eligible for a USDA home loan, borrowers must meet the program’s basic eligibility requirements. These requirements are relaxed compared to other mortgage options and are in place to ensure borrowers can make their monthly mortgage payments.

Here are a few of the basic Kentucky RHS USDA eligibility requirements:

• Income. Applicants must not have annual adjusted income greater than 115% of the median household income for the area. Check your county’s USDA income limit. This called compliance income.

• Credit. USDA’s guaranteed underwriting credit requirements. However, most lenders will want a 620 or preferably to get an Automated Approval 640 is the magic number in most cases. With regards to bankruptcy, 3 years is usually the date needed to lapse since your discharge. They actually require no minimum score but no lenders that I know of will do a no score loan.

• Employment. Applicants must have proof of two years of stable income and employment.

: Income: They will take your gross monthly income and develop two ratios for you: The front end ratio, which is called your housing ratio, and then the back-end ratio or total debt ratio is the house payment plus the total monthly payments listed on the credit report. If you pay child support, this is included in the qualifying ratios but utility bills, car insurance, cell phone bills, water bills etc, is not included. Typically 28% is used for the housing ratio, and

Student Loans: They are pretty tough on student loans and qualifying with your current student loan debts. They will make us use 1% of your outstanding balance on student loans, so sometimes this will cause the loan to get denied because your debt to income ratio is too high. If they are in an Income-Based repayment plan they will still make us use the .5% balance so keep this in mind. For example, let’s say you owe $50k in outstanding student loans, and your IBR plan calls for a $50 monthly payment. RHS will make us use $250, not the $50 IBR payment so you can see where this will cause issue on higher debt to income ratios on some loans.**********

If you are a Kentucky USDA Mortgage applicant who has student loan calculations will be changed to the following Fixed Payment Loans:

A permanent amortized, fixed payment may be used when it can be documented that the payment is fixed, the interest rate is fixed, and the repayment term is fixed.

Non-Fixed Payment Loans (i.e. deferred, income based, graduated, adjustable, etc.): The payment should be calculated as the greater of 0.5% of the loan balance or the actual payment reflected on the credit report. No additional documentation is required.

• Property location. Homes must be located within a rural area, as defined by USDA. Rural areas are any that have a population less than 35,000 depending on the area’s designation. Use this tool from USDA to determine if a specific address is eligible.

• Physical property. Homes must be the borrower’s primary residence, have direct access to a street, and have adequate utilities and water and wastewater disposal, among other things No working fams allowed or properties that income producing livestock or crops.

For those with lower incomes, a USDA direct loan provides greater opportunities for lending, as its credit and income requirements are more lax than the guaranteed loan option.

Disclaimer: No statement on this site is a commitment to make a loan. Loans are subject to borrower qualifications, including income, property evaluation, sufficient equity in the home to meet Loan-to-Value requirements, and final credit approval. Approvals are subject to underwriting guidelines, interest rates, and program guidelines and are subject to change without notice based on applicant’s eligibility and market conditions. Refinancing an existing loan may result in total finance charges being higher over the life of a loan. Reduction in payments may reflect a longer loan term. Terms of any loan may be subject to payment of points and fees by the applicant Equal Opportunity Lender. NMLS#57916http://www.nmlsconsumeraccess.org/