I am a Kentucky based USDA Mortgage Lender that has originated over 200 KY Rural Housing Mortgage Loans in Kentucky, Put my expert advice to use. Kentucky Rural Development RHS loans give KY Rural Homebuyers a zero down mortgage loan with a low 30 year fixed rate loan. A Local Kentucky Rural Housing Mortgage Lender offering same day free approvals and credit report. This website is not affiliated with USDA or any other government agency. NMLS#57916 Equal Housing Lender Text or call today 502-905-3708 with your mortgage questions about USDA Rural Housing Loans in Kentucky. Free Pre-Approvals on most applications within the same day. Kentuckyloan@gmail.com NMLS# 57916 Joel Lobb Loan Originator, American Mortgage Solutions NMLS ID. 1364 Equal Housing Lender

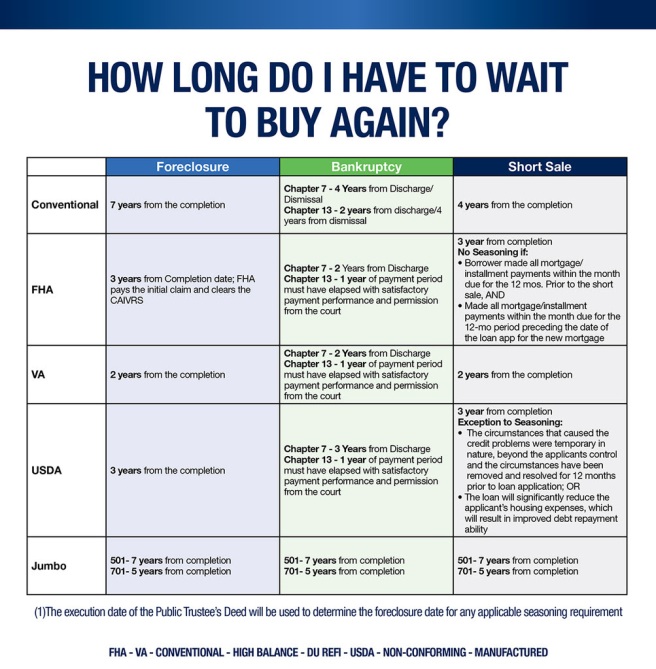

Kentucky Mortgage After a Bankruptcy in 2024 – Chapter 7 or 13

Kentucky Mortgage After a Bankruptcy in 2024 – Chapter 7 or 13

How Long After Bankruptcy Can I Buy a House?

You can buy a house approximately one or two years after filing for bankruptcy, only if you restore your credit and avoid new debt. Filing a Chapter 7 or Chapter 13 bankruptcy will impact your credit report and put a negative score on your credit. But it does not mean that you cannot buy your own house.

Chapter 7 Bankruptcy

The standard type of bankruptcy is Chapter 7, in which the court wipes down your qualifying debts. In this case, your credit score is affected. If you file Chapter 7 bankruptcy, you have to wait for about four years after the court dismisses your bankruptcy to make you eligible for a conventional loan.

However, government-backed mortgage loans are more complex. You have to wait for about three years after your bankruptcies’ dismissal to qualify for a USDA loan. At the same time, you have to wait for about two years in order to qualify for a VA or FHA loan.

Chapter 13 Bankruptcy

Chapter 13 bankruptcy involves the restructuring of your debts. That means you have to make scheduled payments to your creditors. It does not have a substantial effect on your credit score. Moreover, you can keep your assets as well. While regulations for chapter 13 are less severe than Chapter 7, these loans also have a waiting period.

Conventional loans after chapter 13 bankruptcy usually require a waiting period depending on the court’s choice to handle your bankruptcy. Generally, the waiting period is about four years from the date you file bankruptcy and two years from your dismissal date.

While chapter 7 bankruptcy standards are relaxed for government-backed loans, USDA loans have a 1-year waiting period after filing for Chapter 13 bankruptcy. FHA and VA loans need a court to dismiss or discharge approval of your loan before your apply. However, the waiting period remains the same in both cases, whether dismissal or discharge.

There are two types of Kentucky USDA Rural Housing Home loans available to rural Kentucky Home buyers through Rural Development:

Direct homeownership loans and guaranteed home ownership loans.

Let’s first look at the 502 Direct USDA Loan in Kentucky

502 Direct USDA Loan in Kentucky:

With a Kentucky Direct Loan 502, the applicant applies directly to the USDA office serving their location in Kentucky. There are about 13 different locations . They lend the money direct from USDA , 100 percent financing, for the low rate currently at 3 percent on a 33 year term.

For a direct home loan, the purchase, construction, repair and rehabilitation of a single family home in rural areas must be used for the applicant’s permanent residence. “For manufactured housing, only new construction can be funded,” he explained.

Credit scores of 640 or greater are typically acceptable with a minimum number of trade lines (2 usually for 12 months can be opened or closed) that have been open and active.

No down payment typically is required- Loans may be up to 100 percent of the appraised value. Homebuyer education is required prior to closing for the Direct USDA Loan 502 program

Mortgage payments are based on what the applicant can afford to pay. USDA offers payment assistance/subsidies to make it affordable. When you go to payoff the USDA Direct loan, you may incur a subsidy recapture fee.

Paragraph

There are two types of Kentucky USDA Rural Housing Home loans available to rural Kentucky Home buyers through Rural Development:

Direct homeownership loans and guaranteed home ownership loans.

Let’s first look at the 502 Direct USDA Loan in Kentucky

502 Direct USDA Loan in Kentucky:

Rural Home Loans (Direct Program) What does this program do? Also known as the Section 502 Direct Loan Program, this program assists low- and very-low-income applicants obtain decent, safe, and sanitary housing in eligible rural areas by providing payment assistance to increase an applicant’s repayment ability. Payment assistance is a type of subsidy that reduces the mortgage payment for a short time. The amount of assistance is determined by the adjusted family income. Who may apply for this program? A number of factors are considered when determining an applicant’s eligibility for Single Family Direct Home Loans. At a minimum, applicants interested in obtaining a direct loan must have an adjusted income that is at or below the applicable low-income limit for the area where they wish to buy a house and they must demonstrate a willingness and ability to repay debt. Applicants must: • Be without decent, safe, and sanitary housing • Be unable to obtain a loan from other resources on terms and conditions that can reasonably be expected to meet • Agree to occupy the property as your primary residence • Have the legal capacity to incur a loan obligation • Meet citizenship or eligible noncitizen requirements • Not be suspended or debarred from participation in federal programs Properties financed with direct loan funds must: • Be modest in size for the area • Not have market value in excess of the applicable area loan limit • Not have in-ground swimming pools • Not be designed for income producing activities Borrowers are required to repay all or a portion of the payment subsidy received over the life of the loan when the title to the property transfers or the borrower is no longer living in the dwelling. Applicants must meet income eligibility for a direct loan. Please contact your local RD office to ask for additional details about eligibility requirements. What is an eligible area? Generally, rural areas with a population less than 35,000 are eligible. Visit the USDA Income and Property eligibility website for complete details. How may funds be used? Loan funds may be used to help low-income individuals or households purchase homes in rural areas. Funds can be used to build, repair, renovate, or relocate a home, or to purchase and prepare sites, including providing water and sewage facilities. How much may I borrow? The maximum loan amount an applicant may qualify for will depend on the applicant’s repayment ability. The applicant’s ability to repay a loan considers various factors such as income, debts, assets, and the amount of payment assistance applicants may be eligible to receive. Regardless of repayment ability, applicants may never borrow more than the area loan limit (plus certain costs allowed to be financed) for the county in which the property is located. Rural Home Loans (Direct Program) What is the interest rate and payback period? • Fixed interest rate based on current market rates at loan approval or loan closing, whichever is lower. • The monthly mortgage payment, when modified by payment assistance, may be reduced to as little as an effective 1% interest rate. • Up to 33 year payback period – 38 year payback period for very low income applicants who can’t afford the 33 year loan term. How much down payment is required? No down payment is typically required. Applicants with assets higher than the asset limits may be required to use a portion of those assets. Is there a deadline to apply? Applications for this program are accepted through your local RD office year round. How long does an application take? Processing times vary depending on funding availability and program demand in the area in which an applicant is interested in buying and completeness of the application package. What governs this program? • The Housing Act of 1949 as amended, 7 CFR, Part 3550 • HB-1-3550 – Direct Single Family

Sites must be modest and developed in accordance with any standards imposed by a State or local government. Therefore, the lender must verify that the following requirements are met at the time of application.

Site size The site size must be typical for the area. (Some acreage is fine as long as it is normal and the appraisal has comparable sales with similar acreage)

Income-Producing Buildings. The property must not include buildings designed and to be used principally for income-producing purposes. For example barns, silos, greenhouses, or livestock facilities used primarily for income producing agricultural, farming or commercial enterprise are ineligible. However, barn, silos, livestock facilities or greenhouses no longer in use for a commercial operation, used for storage, and outbuildings such as storage sheds are permitted if they are not used primarily for income producing agricultural, farming or commercial enterprise. A minimal income-producing activity, such as maintaining a garden that generates a small amount of additional income, does not violate this requirement. Home-based operations such as childcare, product sales, or craft production that do not require specific features are not restricted. A qualified property must be predominantly residential in use, character and appearance.

Income-Producing Land. The site must not have income-producing land that will be used principally for income producing purposes. Vacant land or properties used primarily for agricultural, farming or commercial enterprise are ineligible. Sites that have income-producing characteristics (e.g. large tracts of arable land ready for planting) are considered income-producing property. However maintaining a garden for personal use is not in violation of this requirement. A minimal income-producing activity, such as a garden that could generate a small amount of additional income does not violate this requirement. A qualified property must be predominantly residential in use, character and appearance.

Site Specifications. The site must be contiguous to and have direct access from a street, road, or driveway. Streets and roads must be hard surfaced or all weather surfaced and legally enforceable arrangements must be in place to ensure that needed maintenance will be provided.

Utilities. The site must be supported by adequate utilities and water and wastewater disposal systems.

Kentucky USDA/Rural Development Changes for Student Loans in 2016

Student Loans and their Impact in the Total Debt Ratio for a USDA Home Mortgage in Kentucky

Recent updates to the 3555 Handbook intended to simplify guidance for the delivery of the guaranteed loan program have caused some misperception in regards to total debt ratio calculations, specifically in the subject of student loans. The Agency is working on revisions to Chapter 11: Ratio Analysis; however, we want to further clarify the subject at this time.

Total debt includes monthly housing expenses plus any other credit obligations incurred by the applicant. Student loan payments must be included in the calculation of the total debt-to-income ratio and captured under liabilities on the application. Student loan payments should be treated as described below:

Fixed payment loans: A fixed payment may be used in the debt ratio when the lender retains documentation to verify the payment is fixed, the interest rate is fixed, and the repayment term is fixed. There must be no future adjustments to the terms of the student loan payments.

Non-Fixed payment loans: Payments for deferred loans, Income Based Repayment (IBR), Graduated, Adjustable, and other types of repayment agreements which are not fixed cannot be used in the total debt ratio calculation. One percent of the loan balance reflected on the credit report must be used as the monthly payment. No additional documentation is required.

Effective immediately, an applicant’s credit score may be validated with at least two eligible trade lines instead of three trade lines as previously required. Such trade lines consist of credit accounts (revolving, installment, etc.) with at least twelve months of repayment history reported on the credit report. Corresponding revisions to the 3555 Handbook will be posted on the USDA Rural Development’s Regulation and Guidance website on March 9, 2016.

At least one applicant whose income or assets are used for qualification must have a valid credit report score or have at least two historical trade line references that have existed for at least 12 months to establish a credit reputation.

For applicants without an established credit history and unable to establish the required number of eligible trade lines to validate the credit score, alternative methods may be used to evidence an applicant’s willingness to pay, such as a non-traditional mortgage credit report or multiple independent verifications of trade references per 7 CFR 3555, Section 3555.151 (i)(6).

Non-traditional credit may not be used to enhance poor payment records or low credit scores. GUS applications receiving an “Accept” underwriting recommendation, but which fail to meet the credit score validation test using a traditional credit report, must be downgraded to a “Refer” by the lender. In these instances the use of a non-traditional credit history will be required in order to proceed.

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

, NMLS ID# 57916, (www.nmlsconsumeraccess.org). I lend in the following states: Kentucky